Robert Y

Sea Limited (New York Stock Exchange: SE) reported recently 1Q24 is strongrter, which further supports the transformation thesis.

Specifically, we could be at the beginning of Free Fire’s return to growth, helping drive Sea Limited’s profitable growth.

The competitive dynamics of Shopee are It is also stabilizing, with the company’s revenue growing strongly and potentially reaching breakeven earlier than expected.

I have written extensively about Sea Limited on Seeking Alpha, which can be found here. In my previous article, I argued that an inflection point had been reached, and since then, we’ve seen financials support that thesis and the stock outperforms the S&P 500 by 30 percentage points. I remain more bullish on Sea Limited than before because I believe we are only at the beginning of the company’s recovery story.

Review 1Q24

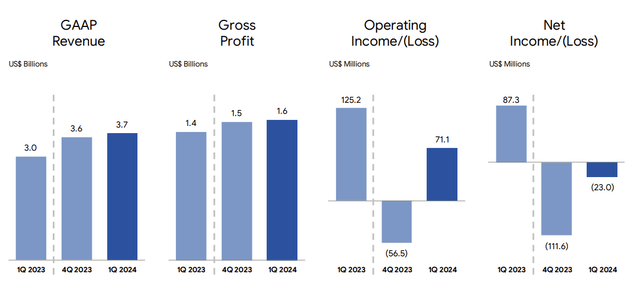

1Q24 results came out on top From consensus expectations.

Total revenue for the first quarter of 2024 was $3.7 billion, up 23% from the previous year. This beats consensus expectations by 3%.

1Q24 Highlights (sea ltd)

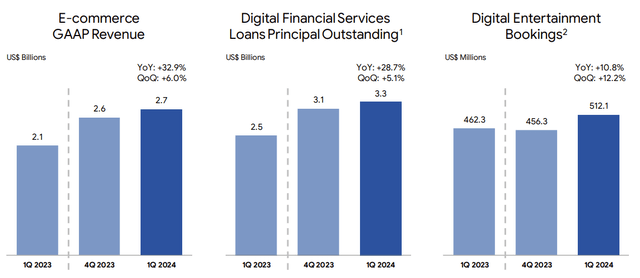

The strength in total revenue was driven by strong GVA growth in the e-commerce business coupled with strong growth in the credit business.

E-commerce revenue for the first quarter of 2024 reached $2.7 billion, an increase of 33% from the previous year, and exceeding expectations by 11%.

Additionally, total e-commerce value grew 36% from the previous year to $23.6 billion, beating expectations by 8%.

Digital entertainment revenue was $458 million, 13% below expectations, but bookings for the first quarter of 2024 were strong.

Digital entertainment bookings rose 11% from a year earlier to $512 million, beating expectations by 7%.

Strong growth in all three sectors (sea ltd)

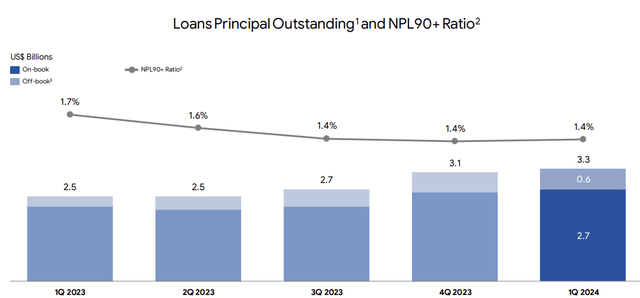

Digital financial services revenues increased 21% from the previous year. In particular, the loan book reached US$3.3 billion, an increase of 29% over the previous year. The number of active users of consumer and SMB loans rose 42% from a year earlier to more than 18 million this quarter.

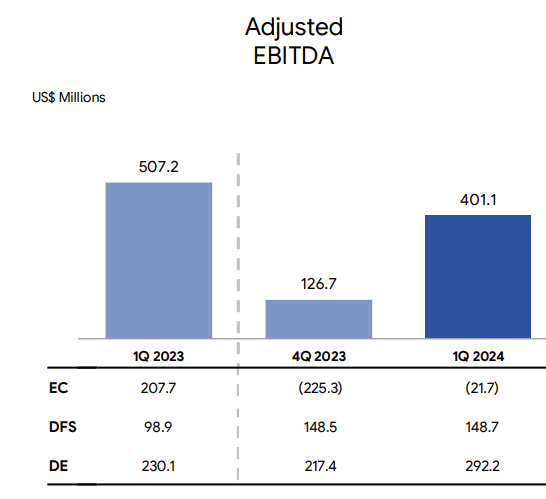

Adjusted EBITDA for the first quarter of 2024 totaled $401 million, beating expectations by 85%, largely due to outperformance in the e-commerce segment.

Adjusted EBITDA (sea ltd)

Digital entertainment adjusted EBITDA rose 27% from a year earlier to $292 million, beating expectations by 35%.

E-commerce adjusted EBITDA was $22 million, significantly beating expectations of $156 million. This also represents a significant improvement over the prior quarter’s e-commerce adjusted EBITDA of -$225 million, indicating significant improvements in cost structure and efficiencies.

In Asian markets, adjusted EBITDA was $11 million.

In its other markets, Adjusted EBITDA was $33 million, significantly narrowing losses from the previous year when Adjusted EBITDA was $68 million. Specifically, contribution margin loss per order improved 88% from the prior year to $0.94.

Digital Financial Services Adjusted EBITDA was $149 million, representing 50% growth from the prior year, and broadly in line with expectations.

Net profit for the first quarter of 2024 was $157 million, beating consensus expectations by 69%.

Overall, we saw Sea Limited perform well in Q1 2024, with the e-commerce segment making faster-than-expected progress towards breakeven while continuing to report strong growth.

This is important because part of the market’s fear was that focusing on profitability would sacrifice growth, and Sea Limited has shown it can balance the two priorities.

guidance

The 2024 guidance was repeated, but I have some feeling that the market was expecting the guidance to be lifted.

I think it’s worth noting that management has seen relatively stable market competition.

The management team is encouraged by the numbers they are seeing in the first quarter of 2024 and are confident of achieving full-year 2024 guidance.

Building on the strength of the first quarter of 2024, particularly in the e-commerce sector, part of that was due to seasonality (Lebaran moved earlier), but the bulk of it was due to the company’s continued investments in three key areas.

This includes reducing the cost of service, providing competitive prices for products, and enhancing the user experience, including with regard to logistics services.

With what Sea Limited reported in 1Q24 and what the management team saw about a month and a half into 2Q24, there is an opportunity for 2024 guidance to be revised upwards after 1H24 was reported.

Operational improvements and focus

Shoppe

Shopee’s focus remains on improving service quality, enhancing price competitiveness and strengthening its content ecosystem.

To enhance price competitiveness, Shopee continues to help sellers with access to the upstream supply chain sell more easily on Shopee.

To improve its content ecosystem, Shopee has focused on live streaming as a new format for engagement and conversion within e-commerce.

In fact, Shopee is now the largest live streaming e-commerce platform in Indonesia based on average daily live streaming orders as of Q1 2024.

As Shopee ramps up its live streaming volume, its e-commerce live streaming unit economics have sequentially improved.

One of Shopee’s key investment areas is SPX Express, which provides integrated logistics capability for Shopee.

Shopee has grown SPX Express into one of the fastest and largest logistics players in its markets.

The goal of SPX Express is to improve customer experience while lowering the cost of service.

In Q1 2024, 70% of SPX Express orders in Asia were delivered within three days of placing the order.

With the expansion of Shopee’s business, SPX Express was also able to reduce its order cost by 15% for Asia and 23% for Brazil year-on-year.

SPX Express has also enabled Shopee to introduce new features such as the Just-in-Time Guarantee program launched in Southeast Asia. By having SPX Express, Shopee is now able to guarantee order delivery time to further improve customer experience.

Another new effort from Shopee to improve user experience is managing the returns and refund process directly.

As a result, resolution times improved by 30%, and in the first quarter of 2024, 45% of cases were resolved within one day.

Overall, I expect Shopee’s investments to not only lower cost of service and improve efficiency as it scales, but also improve its customer experience and deliver a superior e-commerce experience to its users.

Digital entertainment sector

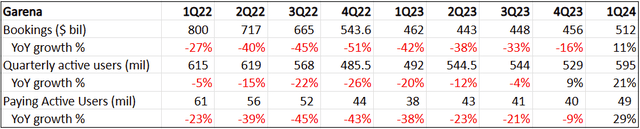

The digital entertainment sector returned to positive growth in the first quarter of 2024.

This is a big deal because Garena has seen bookings decline for 8 straight quarters.

Garena metrics (author created)

As mentioned above, bookings were up 11% year-on-year, and this was driven by Free Fire’s strong performance across all markets.

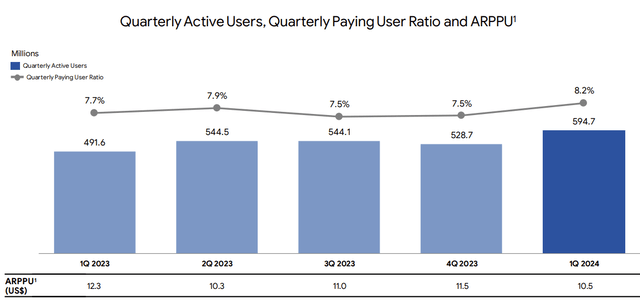

The number of quarterly active users rose by a staggering 21% this quarter, while the percentage of paying users quarterly rose from 7.7% to 8.2%. Quarterly active users returned to positive growth last quarter, while paying active users returned to positive growth this quarter.

In addition, the number of monthly active users also increased by 24% in the first quarter, which is also very strong.

All of these positive metrics indicate two things.

First, efforts to improve employee engagement and retention are certainly paying off.

Second, with a greater number of active users and paying users, there is room for average bookings per paying user (“ARPPU”) in subsequent quarters.

Digital entertainment sector (sea ltd)

Other positive news is that the management is working with various stakeholders in India such as regulators and local partners to relaunch Free Fire in India.

If the relaunch is successful, the management expects there to be a significant rise in bookings given the large market size in India.

As for the current expectations of double-digit growth in Free Fire, the management has not taken into account the relaunch in India.

Free Fire is now in its seventh year and remains one of the largest mobile games in the world in terms of number of users.

It’s still very effective at attracting new users, says Sensor Tower, as Free Fire was the most downloaded mobile game globally in Q1 2024.

Management’s priority continues to be improving user acquisition, engagement and retention, with the ultimate goal being to turn Free Fire into an ever-growing franchise.

Digital financial services

For the digital financial services sector, the credit sector continues to be the largest driver of revenue and profit growth.

One thing to note is that the vast majority of the loan book consists of off-book loans. They are essentially routing arrangements, where lending is done by other financial institutions on the company’s platform.

Another thing to note is the prudent approach to risk management for the credit business taken by Sea Limited. The company first starts by offering low credit limit and short-term loans to users to build their credit history with the company before gradually increasing the credit limit and loan term.

Thanks to this prudent risk control and more data to fine-tune the risk model for each market, we have seen non-performing loans over 90 days as a percentage of total consumer and SME loans stabilize at 1.4%.

Non-performing loan ratio (sea ltd)

I expect that Sea Limited is still at a very early stage in the digital financial services sector as it is still growing its user base in a sustainable way, while poised for future growth as it is able to offer a wider range of financial services to these users.

evaluation

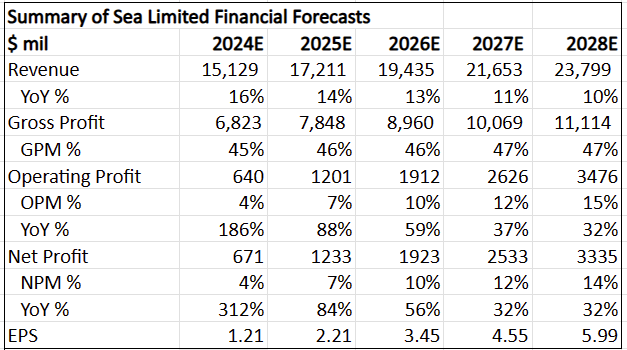

Given the strong first quarter 2024 results across all three segments, I have revised my financial outlook for Sea Limited accordingly.

A summary of my 5-year financial projections (author created)

My intrinsic value rises to $78, largely due to a review of the financial outlook and an increase in the final multiple to 25x, from the previous 20x. This reflects the increased differentiation and improved execution and profitability of the company.

My one-year and three-year price targets are $87 and $121 respectively. The 1-year price target is based on a discounted 2025×45 P/E, and the 3-year price target is based on a 2026×35 P/E. Both assumptions are in accordance with the previous article.

Conclusion

I believe we are only at the beginning of Sea Limited’s recovery story.

In the first quarter of 2024, Sea Limited performed well as its e-commerce segment made faster-than-expected progress towards breakeven while continuing to report strong growth.

Free Fire reported its first-ever positive bookings growth quarter, highlighting that the business is not only stabilizing, but growing.

Considering that this is already Free Fire’s seventh year, and that it remains one of the largest mobile games in the world in terms of number of users, this is a testament to its strong franchise value.

The management’s work with various stakeholders in India such as regulators and local partners to relaunch Free Fire in India is positive news for Free Fire.

Finally, in terms of the digital financial services sector, Sea Limited is still very early stage and is focused on growing its user base in a sustainable way, positioning itself for future growth as it is able to offer a wider range of financial services to these users.