JHVEphoto

Investment thesis

Last time I covered it On the semiconductor company (NASDAQ: ON) Also known as com. onsemi That’s when the stock soared after fourth-quarter earnings in early February. Despite the big post-earnings rally, I was cautious and called In an overreaction. Thus, my previous thesis appears to have matured well, as the stock price is down about 6% over the past three months, compared to +7% for the S&P 500 (SP500).

There have been many developments since then, including the release of Q1 2024 earnings, and I want to share my insights on onsemi with readers. The company’s financial performance continued to deteriorate in the first quarter as rising interest rates continued to impact end markets. There was a significant decline in consensus estimates for long-term revenue growth, which significantly undermined the company’s fair value.

onsemi has a strong financial position and has sufficient resources to do so Current weather challenges. However, I downgraded ON to ‘Strong Sell’ as the stock is now 24% overvalued and positive catalysts are unlikely to emerge in the foreseeable future.

Recent developments

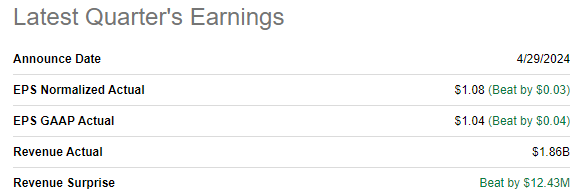

ON released its most recent quarterly earnings on April 29 when the company beat consensus estimates. The company continued to experience weakness in end markets and its revenues declined approximately 5% year over year. The bottom line followed a decline in revenue as adjusted EPS fell from $1.19 to $1.08 year over year.

Seeking alpha

Power Solutions Group (PSG) was the only sector to grow in the first quarter, at a modest 1.6% year-over-year. Both the Analogue and Mixed Group (AMG) and Intelligent Sensor Group (ISG) showed a notable decline year-on-year.

From an end-market perspective, the automotive industry showed 3.2% year-on-year growth, while industrial and other sectors declined by double digits.

ON Latest 10-Q Report

Due to weak revenues, Onsemi’s profitability metrics also suffered. Gross profit margin decreased from 46.82% to 45.83%, and operating margin decreased from 31.45% to 28.27%. Despite a shrinking operating margin, improved working capital management helped improve cash from operations from $409 million to $499 million year over year.

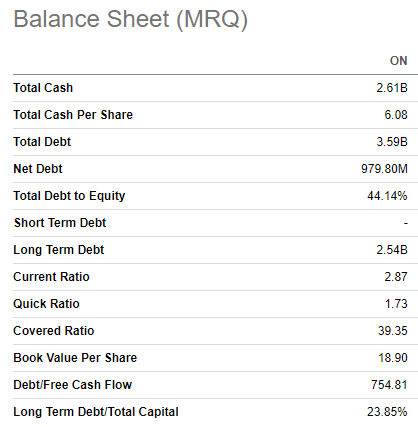

As a result, Onsemi’s balance sheet improved slightly. Total cash grew to US$2.6 billion, and net debt position fell below US$1 billion for the first time since December 2022. The company has a strong financial position with abundant liquidity, meaning onsemi can easily weather the current challenging environment.

Seeking alpha

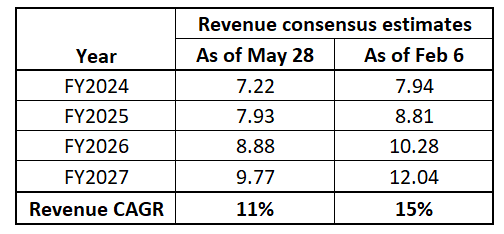

The big red flag for investors is that Wall Street analysts have significantly lowered ON’s long-term revenue growth estimates. In the table below, I compare how projected revenue estimates for FY 2024-2027 looked when I wrote my previous analysis versus the current estimates.

Collected by the author

As of early February 2024, consensus estimates forecast a 15% revenue CAGR between 2024 and 2027. As we can see, currently, the expected CAGR for the same period is now 11%. This is a significant decline that will have a significant impact on my valuation analysis, which I will explain in depth in the next section of my analysis.

According to its latest 10-Q report, onsemi generates about 55% of its total revenue from the automotive end market. The industry is weakening globally following a spending frenzy caused by the pandemic and the highest interest rates across advanced economies over the past 20 years. Although inflation has been slowing steadily, the Fed is likely to keep interest rates higher for longer. It seems to me that all other major central banks are looking at the Fed’s decisions and are unlikely to rush to cut rates before the Fed does. Therefore, expecting weakness in the auto industry for a longer period seems sound.

ON Latest 10-Q Report

Rating update

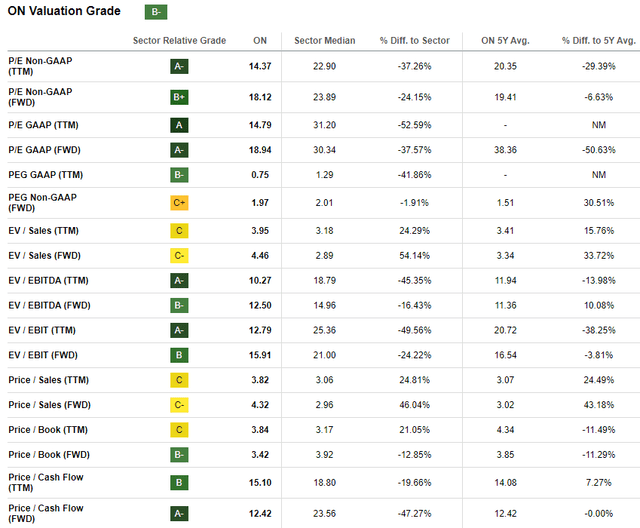

ON’s share price has fallen by about 9% over the past 12 months and has shown a 13% decline since the beginning of the year. The valuation ratios look attractive compared to historical averages and the sector average, making the strong ‘B-‘ seeking Alpha Quant valuation score well deserved.

Seeking alpha

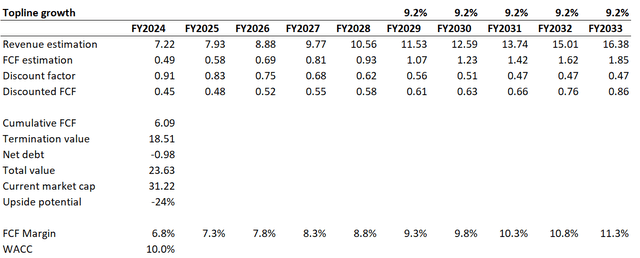

Onsemi, on the other hand, is not a valuable stock to draw conclusions about valuation based on ratios alone. The discounted cash flow (DCF) approach seems to be a suitable option to check from another perspective. I use a WACC of 10%, which is a recommendation from valueinvesting.io. I have consensus revenue estimates available through fiscal year 2028. For the following years, I expect a revenue CAGR of 9.2%. For the base year, I use a 6.8% FCF ex-SBC margin, which is the average for the past decade. Since revenues are expected to grow, I think incorporating FCF margin expansion of 50 basis points annually is fair.

Author’s calculations

The company’s fair value is about $24 billion, 24% less than its current market value. Therefore, ON is significantly overvalued, especially in the context of all the current headwinds the company is facing.

Risks to my bearish thesis

As I wrote in my initial thesis on onsemi, communion is fundamentally powerful from a secular perspective. The company has a strong and diversified revenue mix. The exposure to the automotive industry which is witnessing a secular shift to electric vehicles (EVs) is enormous. Therefore, Onsemi is certain to enjoy strong revenue growth and a rebound in profitability expansion once the monetary environment becomes more positive. The macro environment is evolving rapidly, and the Fed analyzes all changes in key metrics. Therefore, if there is a sudden rise in unemployment rates, it could force the Fed to start cutting interest rates earlier than expected. In this case, Onsemi would likely see an upward consensus revision to its growth prospects, which would boost the company’s fair value.

The company may take cost-effective steps that can be perceived very favorably by the market and result in significant upside. For example, the company has about 30,000 employees. Since the beginning of monetary tightening, the company has laid off nearly 2,000 employees. This is a significant reduction in headcount, but it is still less than 10%, which means there will likely be more potential for layoffs. If the company announces a new round of layoffs that will lead to noticeable improvements in earnings per share, it is very likely that the stock will rise.

minimum

In conclusion, ON is a “strong sell” at current levels. Long-term consensus revenue forecasts have significantly undermined the company’s fair value, and the stock is currently overvalued by approximately 24%. The challenges are likely to continue further as interest rates are expected to rise for a longer period.