Service characteristics: Low hotel occupancy rates, which renews concerns about dividends

Liz Leyden/iStock Unreleased via Getty Images

Service characteristics trust (Nasdaq: SVC) is a real estate investment trust consisting of hotels and rental retail properties with no employees and outside management that controls its operations. Last year I wrote about income opportunities through high-yield corporate debt. Earlier this week, it participated in a tender offer for Dionne’s property. With several high-yield options remaining, I reviewed the company’s financials and decided not to put new money into Service Properties’ debt.

FINRA

Service Characteristics Trust Financial Results

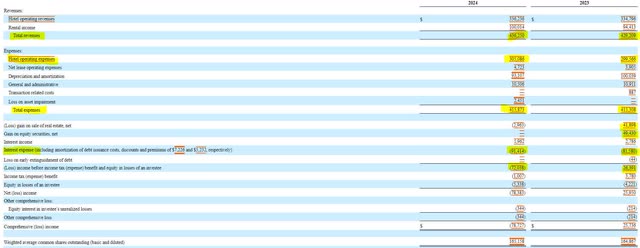

Service Properties Trust’s first-quarter financial results showed a slight increase in revenue, led by the performance of net leased properties. While overall expenditures remained under control, this was mainly due to lower consumption. Operating expenses rose and interest expenses jumped by $10 million, resulting in a loss of $72 million before taxes.

10-h seconds

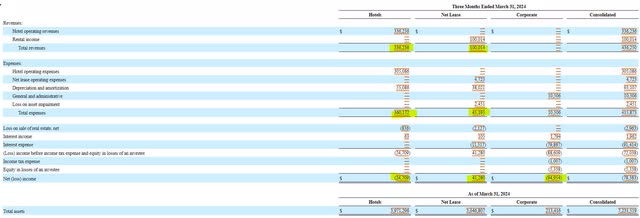

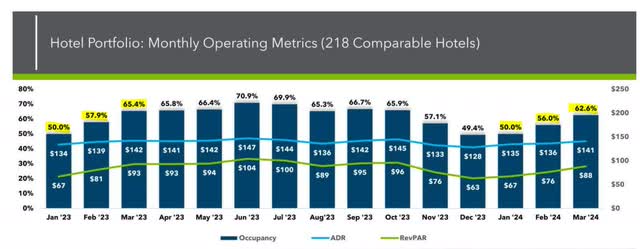

The net lease portion of the Service Properties business is performing well, but is not large enough to support the company’s costs (which are mostly interest expense). The hotel sector is much larger, but not profitable. The main reason for Service Properties’ problems is hotel occupancy, which continues to decline with the last two months seeing a year-over-year decline in occupancy. Even though their net rental occupancy is over 97%, they cannot generate more revenue/profitability from existing assets in this segment.

10-h seconds Investor presentation 10-h seconds

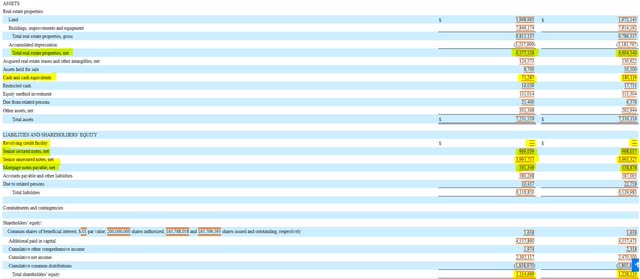

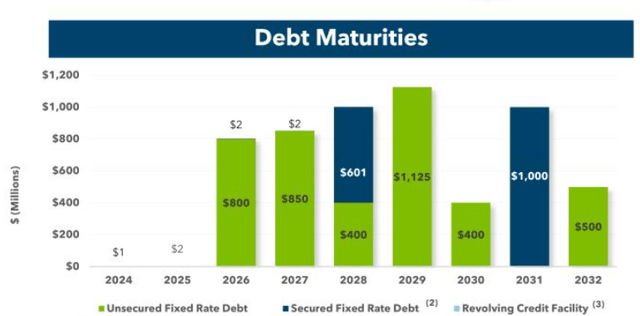

Although there are no changes, investors can get a good idea of the capital structure by examining the company’s balance sheet. Not much changed in the first quarter, except that the company reduced its cash position by about $110 million. Service Properties Trust has net real estate assets of $6.58 billion against approximately $5.5 billion of secured, unsecured and mortgage debt. Shareholders’ equity fell by $100 million to $1.1 billion during the first quarter.

10-h seconds

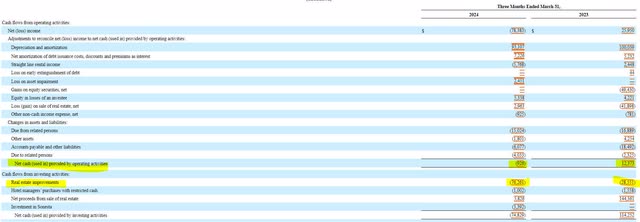

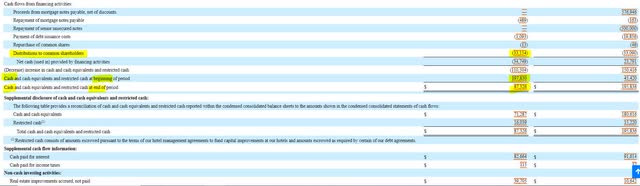

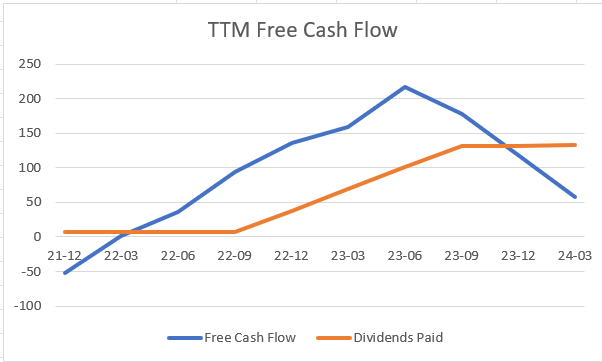

The cash flow statement demonstrates my primary interest in Service Properties Trust, and its ability to generate cash flow and maintain its dividend. Operating cash flow fell below zero in the first quarter. Add $76 million in capital expenditures, and the company had free cash flow of $77 million. The company is unable to support a dividend at this level in my view, and the $33 million dividend only adds to the quarter’s cash flow burn of $110 million. Additionally, the trend in trailing-twelve-month free cash flow has been disappointing since I last wrote about the company. Cash flow burn also highlights the inability to service debt without taking on more debt. Service Properties Trust has an untapped $650 million credit revolver it can fall back on, but that also comes at the cost of additional interest liabilities.

10-h seconds 10-h seconds Taker 10-h seconds

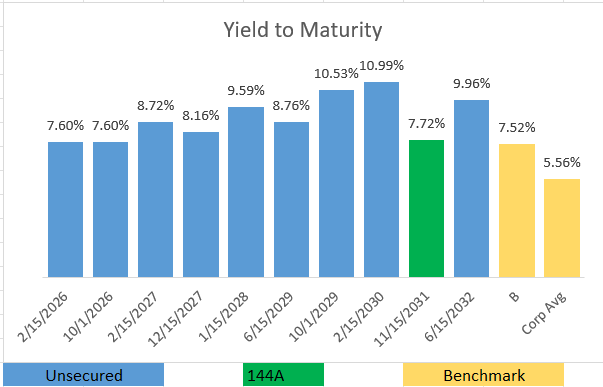

Changes in debt

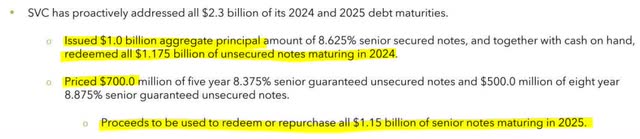

Service Properties Trust has undergone some recent changes to some of its $5.5 billion debt. Last fall, the company issued $1 billion in 8.625% senior secured notes due 2031. The company used those proceeds to repay $1.2 billion of notes due 2024. Recently, Service Properties priced $1.2 billion of notes Unsecured at 8.375% and $8.875. % with maturity dates in 2029 and 2032 respectively. These bonds will be used to repay the company’s 2025 maturities and extend the next maturity date to 2026.

Investor presentation Investor presentation

Although the ability to refinance has been good, and the ability not to increase the secured class of creditors beyond what was created last fall is better, investors need to keep in mind the cost of this refinancing. Service Properties Trust is refinancing debt that previously carried interest of $75.75 million annually with debt that will bear interest of $103 million, adding to cash flow generation pressures.

10-h seconds

Conclusion

The decline in Service Properties Trust’s hotel business raises serious concerns about the viability of the company’s earnings. Add to that the higher cost of financing its debt load, and investors will almost certainly expect a decline in free cash flow in future quarters. With the company burning cash, I will take the money earned from my tender offer and look for another opportunity.