Boarding1Now/iStock editorial via Getty Images

In February, I downgraded Singapore Airlines shares to ‘hold’ due to a challenging cost profile combined with unit revenue pressure. Additionally, the stock underperformed against the broader market, and despite having a double-digit return, it was not attractive compared to the market. performance. Also, analyzing the stock in my Stock Screener did not provide any compelling reason to put a buy mark on the stock. In this report, I will discuss the latest results and revisit my price target for Singapore Airlines stock.

Singapore Airlines’ financial results show a challenging revenue environment

Singapore Airlines

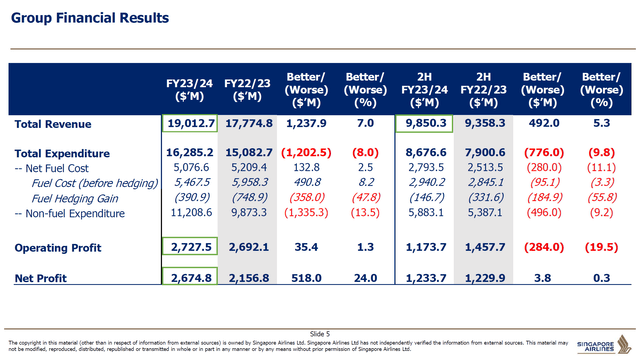

Looking at the results, things don’t look great. When I look at top line growth, I look at top line growth with expanding context capability. Total revenues increased by 7% thanks to a 23% expansion in passenger capacity. This is not entirely favorable. It gets a little better when we think about it Passenger revenues increased by 9.7%. However, it still points to one of the risks I mentioned earlier that is already materializing, which is unit revenue erosion. Shipping revenues decreased by 22.4% as a result of continued weakness in revenue.

When capacity doesn’t translate favorably to the top line, I think for this capacity expansion to be worth it, we should see a significant improvement in unit costs. Total costs increased by 8%, partially offset by a 2.5% decrease in net fuel cost. However, non-fuel costs rose 13.5% driven by higher passenger costs, which rose 43%, while navigation fees, handling fees and staff costs all rose by double digits but with growth below capacity. Therefore, costs increased in absolute terms. However, unit cost development was favourable. Unit costs excluding fuel fell by 3.3% at Singapore Airlines and 4.5% at low-cost carrier Scoot.

Overall, operating profits rose 1.3% with margins falling from 15% to 14.3%. I believe that in the current operating environment, margin pressure and erosion will continue.

Are Singapore Airlines shares a buy?

Aerospace Forum

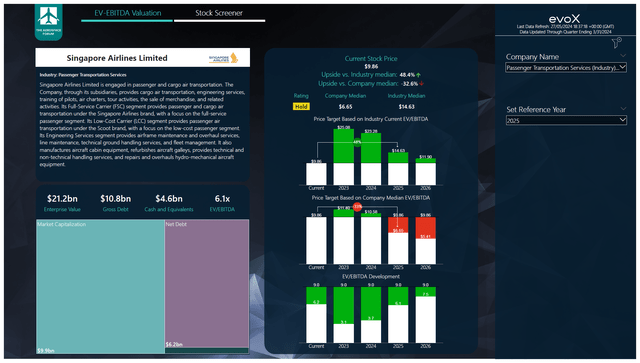

I’ve added Singapore Airlines’ balance sheet to my model as well as the future forecasts, and although EBITDA estimates are high, the investment case is not very compelling with nearly a 50% upside versus an industry benchmark valuation but Downside of 33% when determining valuation. On Singapore Airlines’ average EV/EBITDA multiple. Singapore Airlines’ somewhat stressful investment case is driven by expectations that free cash flow will come under pressure as capital expenditures for fleet development rise. Fleet growth is good, but we also see unit revenues coming under pressure. So the risk is that Singapore Airlines will spend billions of dollars on in-flight equipment while its ability to extract revenue from seats will remain under pressure.

Furthermore, the company has mandatory convertible bonds which are not classified as debt, but rather as equity. Singapore Airlines has redeemed these multilateral loans and the last tranche will be redeemed by June 2024. Since this is not a debt instrument of Singapore Airlines, the cash and equity will decrease after the redemption but the debt will remain the same. Although I consider this part of deleveraging, it does nothing for gross debt while increasing net debt.

Overall, I like the way the company manages its debt but I don’t see a compelling investment case for Singapore Airlines and I reiterate my Hold rating.

Conclusion: Singapore Airlines is a better buy

Although I like how Singapore Airlines, like many airlines, is cleaning up its balance sheet, I think the FY2024 results showed the facts fairly well. Unit revenues and freight revenues remain under pressure, fuel costs are uncontrollable swing cost elements for airlines, and overall the industry continues to experience some cost inflation making cost absorption a challenge. Singapore Airlines has made progress in this regard in FY24, but I believe the investment in the airline is not compelling.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.