Wand_Prapan

Overview of structural treatments

Therapeutic Infrastructure Company (Nasdaq: GBCR) was in the news yesterday after a phase 2a obesity study (randomized, placebo-controlled) of “an orally available small molecule agonist of the glucagon-like peptide-1 (GLP-1) receptor,” GSBR-1290, caused dramatic weight loss. Statistically significant using placebo After 12 weeks. The company targets the obesity treatment market is expected To reach $130 billion in 2030. Current leaders, Novo Nordisk (NVO) And Eli Lilly (LLY), delivering subcutaneous GLP-1 agonists, Wegovy and Zepbound (GLP-1 and GIP), respectively.

In March, I provided an overview of the clinical landscape for obesity, which focused on several companies targeting MOA and different administration routes (subcutaneous and oral). While I’ve covered most of the companies vying for the obesity connection, Structure was one I didn’t touch upon. So, let’s take a closer look at the data for the GSBR-1290.

the main points:

- The mean placebo-corrected weight loss was 6.2% (P<0.0001) after 12 weeks.

- 33% of patients achieved at least 10% weight loss, compared to 0% for placebo.

- The AE-related study discontinuation rate was 5.4% for drug and 0% for placebo.

- Side effects included nausea (89.2%), vomiting (62.2%), and constipation (43.2%).

For reference, the comparison is likely to be close with an oral GLP-1 agonist Viking Remedies (vctx) VK2735. Below is a table comparing oral GLP-1 agonists.

| Factor | Viking VK2735 | Chassis GSBR-1290 |

| Type of study | Phase 1 (28 days), n = 47 | Phase 2a (12 weeks), n=64 |

| Dosages | Oral, daily, MAD (2.5 mg, 5 mg, 10 mg, 20 mg, 40 mg) | Oral, daily, 120 mg |

| Placebo-adjusted average weight loss | Up to 3.3% (at 28 days), 5.3% for 40 mg group (n = 7) | 6.2% (in 12 weeks) |

| ≥5% weight loss | Up to 57% of subjects | 67% of subjects achieved ≥6% weight loss |

| Common adverse events | Mild nausea (14%), no vomiting, mild diarrhea (3%) | Mild to moderate nausea (89.2%), vomiting (62.2%) |

| Future plans | The phase 2 obesity trial is scheduled for the second half of 2024 | The Phase 2b obesity study is expected to begin in the fourth quarter of 2024 |

Obviously there are many drawbacks when comparing two experiences. In the previous example, the Hulk determined the ideal dosage, while Viking was still experimenting. As a result, tolerability data favor Viking, as lower doses such as 2.5 mg and 5 mg are not expected to be the preferred maintenance dose.

Even more surprising is the amount of nausea and vomiting caused by 120 mg of GSBR-1290. Dose titration may help alleviate this (as described for Zepbound). Also worth noting is VK2735’s extraordinarily fast and powerful weight loss results in just four weeks. In the 40 mg group (n=7), patients lost an average of 4.9 kg (about 11 lbs) from baseline after just 28 days of daily dosing. The number of participants in both trials remains small, so caution should be exercised when drawing conclusions from either.

Whether it’s luck, experience design, or something else, one thing is clear when comparing the two experiences: Viking’s drug It seems To be superior. And remember, Viking is one of many competitors that Structure will face.

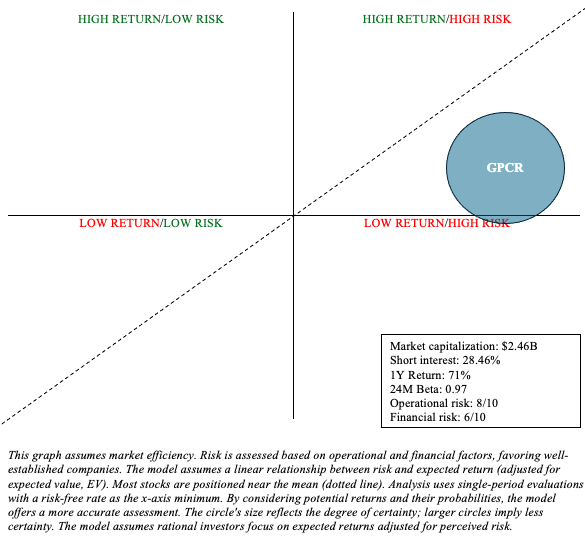

GPCR Stock Financial Health

Following the Phase 2A data, Structure announced its intention to offer 8 million shares. This should raise about $400 million, assuming the price is closer to $50 per share. Therefore, this will boost their cash and short-term investments, which totaled $97.8 million and $338.6 million, respectively, as of March 31. The structure includes only $27.4 million in total liabilities.

Research and development, general and administrative expenses for the first quarter were $20,679 million and $11,336 million, respectively. Since Structure is not yet profitable, I will estimate its cash runway based on its historical cash burn. If we divide their most liquid assets ($436.4 million) by quarter Burn cash ($32.015 million), which refers to more than three years Cash runway. This is expected to extend significantly if the public offering is completed.

Risk/reward analysis and investment recommendations

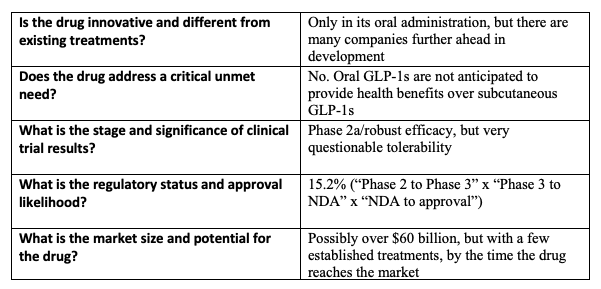

When I evaluate biotech stocks, I ask myself: Five key questions To guide the decision-making process.

author

However, while the structure has many hurdles to overcome, it is difficult to bet against any oral or subcutaneous GLP-1 candidate. This landscape is likely to strengthen, and I expect mergers and acquisitions to continue in the coming years. Furthermore, Structure has other obesity candidates in its pipeline (in the “discovery” phase) that target other incretins, such as amylin. This diversity of objectives reduces operational risks. So, although I’m not as bullish on the structure, compared to, say, Viking, it can still be part of a barbell portfolio, where the majority of the money is allocated to lower-risk assets, like Treasuries and broad market ETFs, with The remaining part is up to speculation.

As for financial risk, an opportunistic capital increase will significantly increase its cash runway. This is important, because advancing GSBR-1290 to late-stage trials would be very expensive. However, as with any clinical-stage biotechnology, Structure’s long-term financial outlook is quite ambiguous.

author

All things considered, the structure is Catch And it certainly deserves close monitoring moving forward.