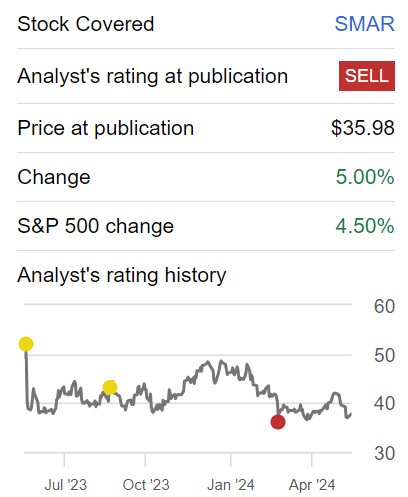

Skynesher/E+ via Getty Images

Investment thesis

Smart sheet (New York Stock Exchange: Smar) gave a generally positive report, and its stock jumped 12% pre-market.

But I find myself less enthusiastic. Here’s the thing, I’ve seen this kind of setup before many times. The company operates small Numbers and having a few good quarters, the stock appears to be off to the races.

Ultimately, I wonder if paying 31 times non-GAAP operating earnings is so tempting. On the other hand, the earnings report was strong enough that it wouldn’t make sense to be bearish on this stock as well.

Quick recap

I said in my previous bearish analysis:

This is how I see SMAR: You have a stock that carries a strong valuation at 34 times non-GAAP forward EPS, is facing decelerating growth rates, and where the company’s underlying profitability relative to… Most of them have reached their limit and gone as far as they can at the moment.

With so many trades in the market right now, I am issuing a sell rating on SMAR.

The author worked on SMAR

With the benefit of hindsight, it wouldn’t have made sense to issue a sell rating on SMAR, and I should have kept it neutral.

But in the market, it’s never what you should have done, it’s what you did.

Smartsheet’s near-term prospects

Smartsheet provides a platform for managing collaborative work, acting as a digital workspace where teams can plan, track, and manage projects together and communicate.

Smartsheet is a bit like Asana (ASAN) but with much better financials. While Asana also focuses on project management and team collaboration, it emphasizes a more user-friendly interface.

Although both systems aim to improve project management, Smartsheet offers more spreadsheet-like features for tracking complex projects, while Asana strives for ease of use for task management.

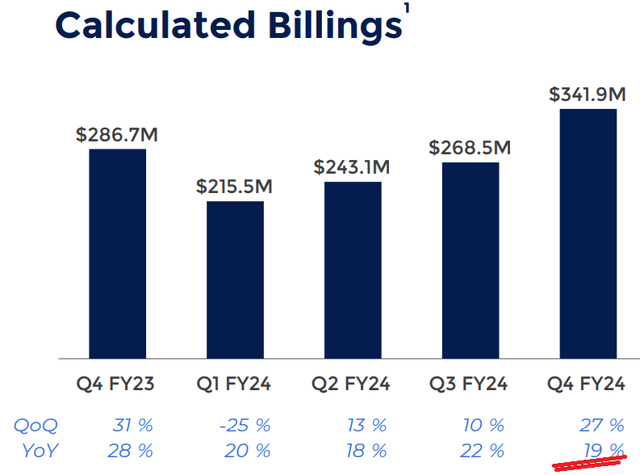

The main problem I had with Smartsheet was that its billing metrics were disappointing.

Smar fourth quarter 2024

As you know, billings are a leading indicator of revenue growth rates.

Above is the last time Smartsheet reported on its billing metrics. Since billings were moving in the wrong direction, management decided to stop reporting their billings and asked investors to instead focus on ARR (Annual Recurring Revenue).

Looking at fiscal 2025, this suggests roughly 15%, which, as you’ll soon see, is below Smartsheet’s revenue growth rate guidance for this fiscal year. This will likely become an issue over time – although everything still seems reasonably solid at the moment. Let’s discuss this further.

Smartsheet’s growth rates could reach 19% this financial year

Smartsheet revenue growth rates

Smartsheet was expected to achieve revenue growth rates of 18% year over year for its fiscal first quarter, but ended up achieving revenue growth rates of 20% year over year.

This has two effects. The first is that it allows management to talk about their growth rates stability. After all, the first quarter of 2025 marks the 11th straight quarter of slowing revenue growth rates. Stabilization in their growth rates is long overdue.

But more importantly, given that Q1 FY 2025 was up against a more challenging “last” quarter, and Smartsheet was able to grow 20% year over year, this means that for Q2 FY and the rest of FY 2025, Smartsheet will Against much easier comparisons.

In practical terms, this will allow Smartsheet to easily beat the maximum guidance for fiscal 2025 revenue growth rates of 17% year-over-year. For my part, I assumed that Smartsheet would grow 19% year over year this fiscal year. However, I think even this number may end up being too conservative. But let’s go with this for now. In light of this context, let us discuss its evaluation.

SMAR Stock Valuation – Non-GAAP Forward Operating Earnings of 31x

I said in my previous analysis, in addition to the financial results for the fourth quarter of 2024:

Smartsheet saw its core earnings rise from negative 5% non-GAAP operating margins in fiscal 2023 to 11% non-GAAP operating margins in fiscal 2024, a 1,600 basis point expansion in profitability in 12 per month, see below.

Given the ease with which Smartsheet improved its underlying profitability, investors were anticipating continued profitability improvement in fiscal 2025.

Now, if we take Smartsheet’s maximum fiscal 2025 non-GAAP operating margins, Investors are looking for a roughly 14% to 15% improvement in underlying profitability. (Emphasis added)

This means that the majority of the low-hanging fruit has been picked, and operating expenses have been reduced to the greatest extent possible.

Accordingly, it said that Smartsheet’s fiscal 2025 non-GAAP operating margins will hover around 15%, and that there won’t be a lot of juice to improve core profit margins this fiscal year.

Furthermore, even if Smartsheet’s earnings eventually reach $180 million, rather than the high end of its current guidance of $167 million, this would still only see its non-GAAP operating profit reach 16%. That’s why I find it difficult to be overly optimistic about this stock.

You’re looking at roughly 19% overall growth, with operating profits pretty much at the ceiling. So, having to pay about 31 times non-GAAP operating earnings seems like fairly valuable indeed.

On the other hand, we should keep in mind that Smartsheet has about $660 million of cash and short-term investments and no debt.

Considering that Smartsheet is expected to generate perhaps another $230 million in free cash flow this year, that means Smartsheet has enough wherewithal to make a major acquisition.

Bottom line

I believe Smartsheet stock is highly valued given its balanced financial outlook and strong recent performance.

Although the stock jumped 12% pre-market after a positive earnings report, I still have concerns about the high valuation of about 31 times non-GAAP forward operating earnings, especially with slowing growth rates and limited potential. For further improvements in profitability.

However, Smartsheet’s strong financials, including $660 million in cash and no debt, coupled with stable revenue growth rates and significant expected free cash flow, make me think its current valuation is reasonable, without being overly bullish.