Oat_Phawat

introduction

It’s time to head back to 2022.

At that time, I wrote my last article covering the Copper Giant Southern Copper Company (New York Stock Exchange: SCO) In an article entitled “I am the Brass Bull, and this is why I go south Copper can double.”

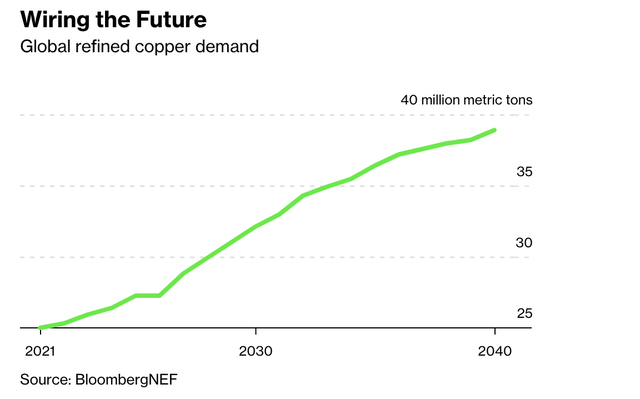

In this article, I discuss the strong tailwinds for copper, especially regarding its role in the energy transition, which could push annual copper demand to nearly 40 million metric tons by 2040.

Bloomberg

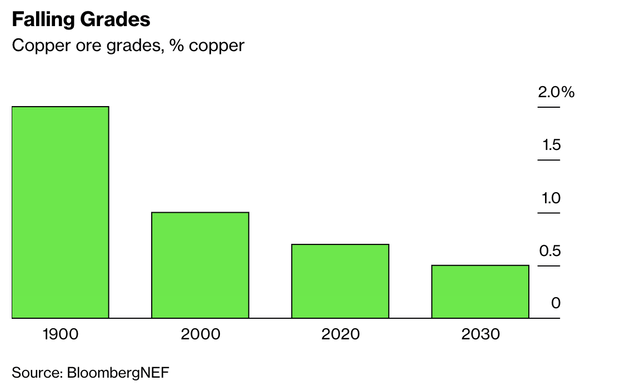

At the same time, global copper supply is weakening, as evidenced by the sharp decline in copper ore grades, which are expected to fall to 0.5% by 2030.

Bloomberg

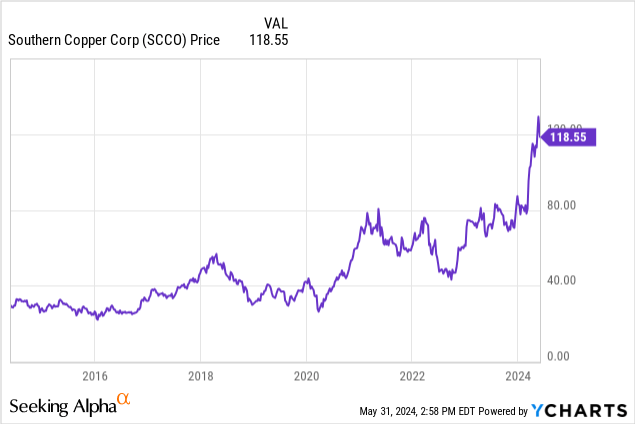

Since then, SCCO shares have risen 162%, outpacing the S&P 500’s (SP500) staggering 37% rise by a wide margin.

Even better, including dividends, the total return for New York-listed SCCO shares is 181%.

In this article, I will update my thesis using new developments, the latest company financials, and my view on overall risk/reward.

So lets get to it!

Copper fly

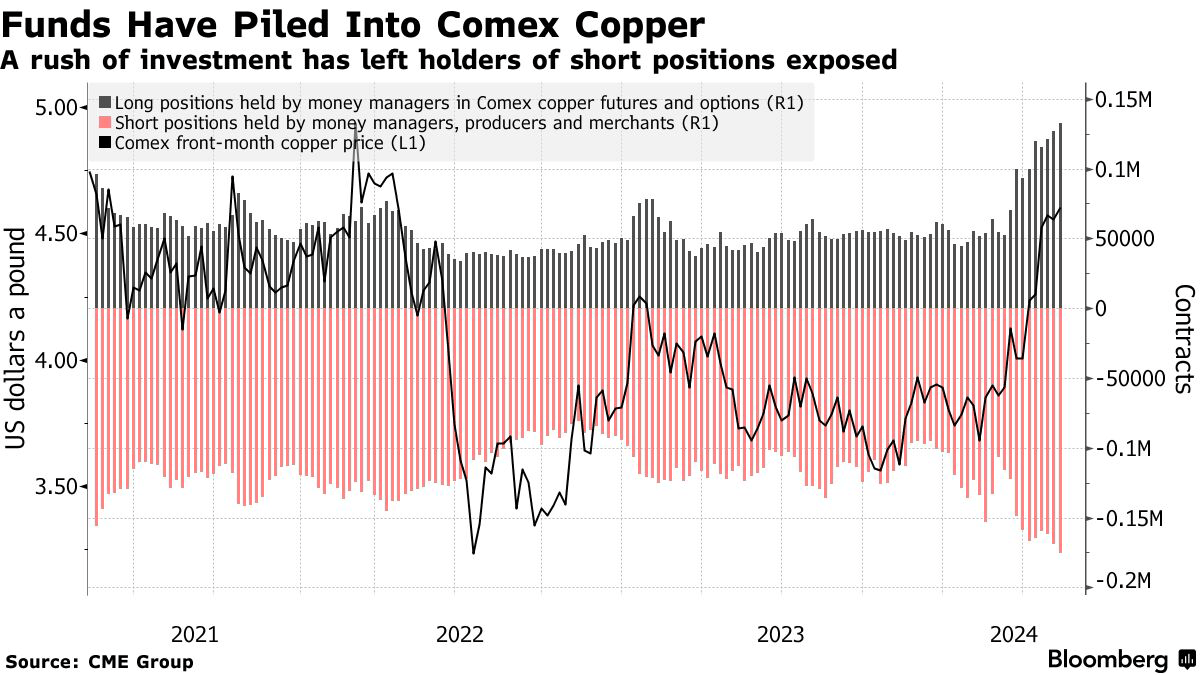

In the second half of May, COMEX copper futures (HG1:COM) rose to $5.10 per pound, the highest copper price ever.

Although prices have fallen slightly since then, they remain at levels seen during the first two years after the pandemic.

TradingView (Comex Cooper)

As the Wall Street Journal reported on May 20, copper is benefiting from a number of trends. I added emphasis to the quote below.

The price of the world’s favorite electrical conductor hit a new record on Monday, hitting its target for the seventh straight day of gains. Obviously, big investors are getting in on the action. The big macro hedge fund, Caxton Associates, pointed this out Three mega trends that could have a lasting impact on demand for the electrical metalIn a recent letter to investors.

The markets are just waking up The long-term impact of artificial intelligence And National industrial policiesincluded Defense spendingCaxton president Andrew Law wrote. This is in addition to what is already well established Green energy investment trend.

“What all three have in common is the need for copper,” he said.

“Building AI by companies and countries will be a modern-day arms race with competing and recurring investments across geographies,” Lu added. -The Wall Street Journal

In other words, in addition to the green shift, the market is now expecting further tailwinds from AI (infrastructure), defense spending, and the return of economic support.

As a result, investors’ total long positions increased by almost 3x, as we can see in the chart below.

Bloomberg

What’s interesting is that Bloomberg commodities expert Javier Blas wrote an in-depth article on copper, including comments from sell-side researchers who see much more upside potential if we compare the May rally to previous highs.

Can copper rise to $12,000 per ton, perhaps $13,000? maybe. In 2008, during the China-led commodities boom, the metal briefly traded above $8,000. In real terms, adjusted for inflation, they would need to rise to nearly $14,000 per ton in today’s currencies to match that peak. -Bloomberg

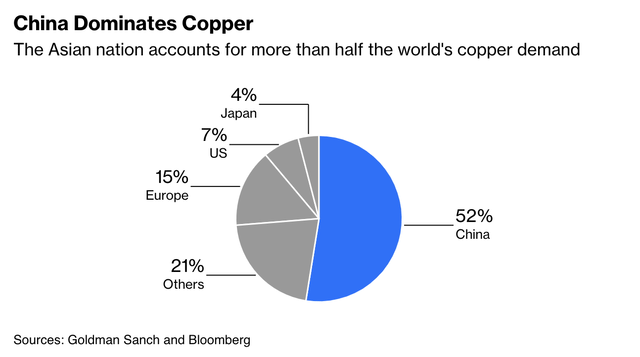

However, he calls for caution, as China accounts for nearly half of the world’s copper consumption.

This nation is currently facing a weak real estate sector, which has been one of the biggest drivers of global commodity demand since the early 2000s.

Bloomberg

Mr. Blass stresses that China’s physical copper market remains weak, which makes it unlikely that manufacturers will be willing to pay premiums for copper.

He even asserts that global copper demand forecasts are useless (I’m paraphrasing here).

Essentially, he asserts that these estimates are based on what the world would look like in a “net zero” environment.

The problem is that based on current trends, we will not see such an environment, which means that the demand outlook for copper is likely to be very high.

The CRU Group expects global demand to reach 35 million tons by 2050, which is significantly lower than current forecasts.

However, the bull’s condition remains intact. Even if demand growth is weaker than expected, it will still face upward supply challenges.

In the words of Mr. Blass:

(…) The easiest copper deposits were exploited. Additional production will come from miners with lower ore grades, located in more difficult geographic areas, and perhaps with ore bodies buried deeper.

However, he still maintains that people who call copper “the new oil” are wrong, because this would require the most optimistic supply and demand forecasts to turn into reality without the support of new resources and technological advantages.

I agree with that.

The odds of that are very low.

Although I remain bullish on copper in the long term, I am not chasing that rally.

So, what does this mean for Southern copper?

A closer look behind the SCCO bar

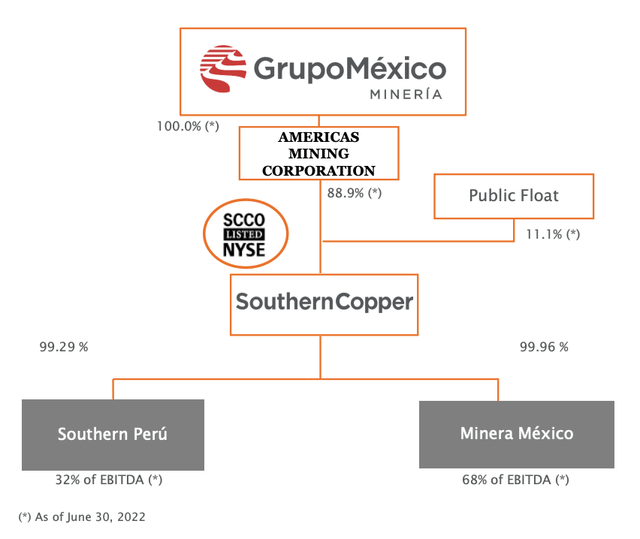

Southern Copper is one of the largest copper miners in the world. It is also majority owned by Mexican company Grupo Mexico (OTCPK:GMBXF).

Mexico group

In addition to taking advantage of strong prices, the company is working to boost production.

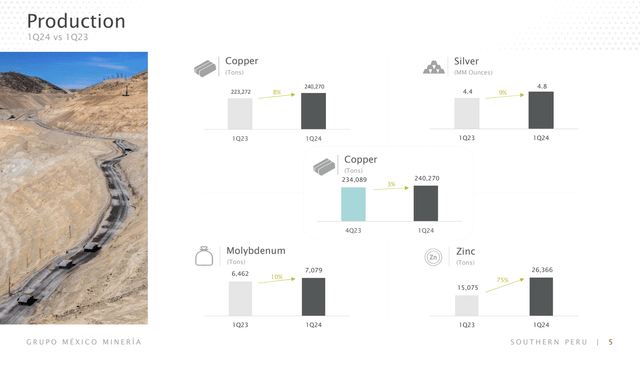

In the first quarter of this year, copper production increased by 7.6% quarter-on-quarter, bringing the total to 240,270 tons.

South Copper

According to the company, this growth was driven by significant improvements in Peru, with production increasing by 19% due to higher ore grades and improved mineral processing and extraction.

Looking ahead, the company’s 2024 forecast sees copper production rising to 948,800 tons, which translates to a 4.1% increase compared to 2023.

Furthermore, the Belares project and Buenavista zinc concentrator are expected to contribute 43,800 tonnes of copper. Last year, the company brought Pilares to full capacity and began ramping up production from the Buenavista Zinc Center.

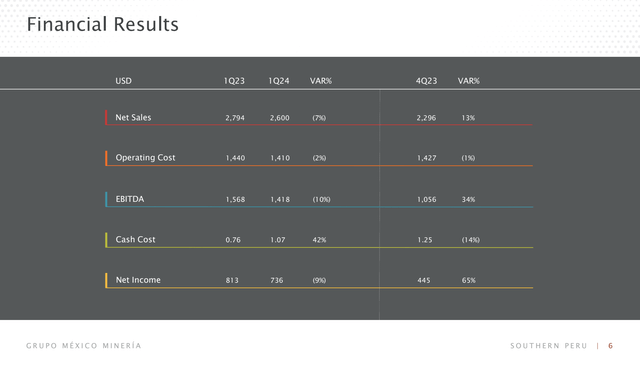

However, the company’s revenues did not increase, on the contrary.

In the first quarter of 2024, the company reported a 7% decline in net sales of $2.6 billion. This is mainly due to the significant rise in copper prices, which started to break their highest levels during the first quarter of 2023 after the end of the first quarter. In other words, the recent rise is not included in these numbers.

South Copper

The good news is that strong margins kept net income below 10%, which also helped the company increase operating cash flow by 22% to about $660 million.

We must also say that Southern Brass brings more to the table than brass.

Besides copper, the company produces large quantities of molybdenum, silver and zinc.

- Molybdenum, which represents 10.5% of sales value in the first quarter of 2024, saw an increase in production of 9.5% compared to the same quarter of the previous year. This metal is used in alloying because it improves strength and electrical conductivity. For example, many engines include molybdenum.

- silver Production also increased by 8.4% in the first quarter of 2024, with expectations for production of 20.5 million ounces in 2024, which represents an increase of 11.4% from 2023.

- Zinc Production saw a 75% increase quarter-on-quarter thanks to the company’s new Buenavista zinc concentrator.

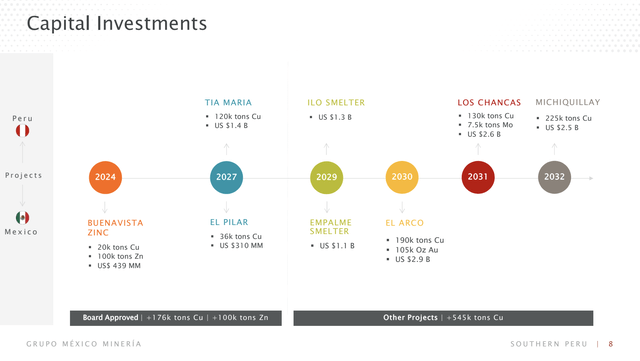

Going forward, the company aims to boost production in both Peru and Mexico.

As we can see below, these projects include the Tia Maria, Los Chancas, Michiquillay, Buenavista Zinc, Pilares, El Pilar and El Arco projects.

South Copper

In the first quarter of 2024 alone, the company invested $214 million in capital expenditures, representing 29% of net income.

As we mentioned previously, we expect to produce 54,500 tons of zinc and 11,900 tons of copper this year, and over the next five years we expect our average production to be 90,200 tons of zinc and 20,000 tons of copper annually coming from this new Buenavista zinc concentrator. – SCCO Q1 2024 earnings call.

evaluation

Setting a fair target price for a copper miner is difficult.

After all, revenues depend heavily on the price of copper.

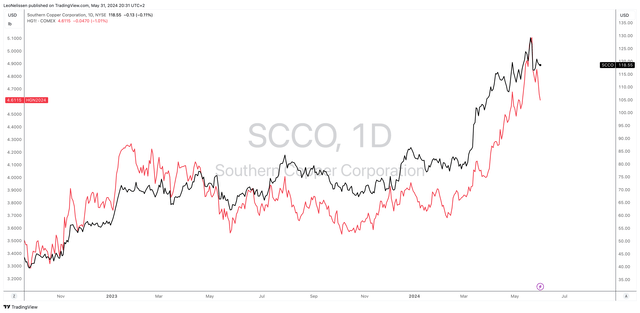

This is what the comparison between SCCO (black line) and COMEX copper looks like:

TradingView (SCCO, COMEX Cooper)

After the recent rally, we need copper prices to remain high.

Why?

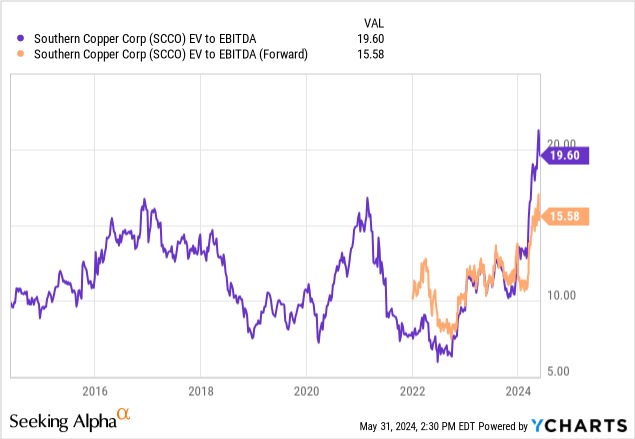

This is because SCCO is now trading at a forward EV/EBITDA multiple of 15.6x, which is near the high end of its 10-year range.

Although I am optimistic about copper’s long-term future, I think the massive rally over the past two years requires some caution.

Copper’s recent rally has been great and will likely be offset by fears of a cyclical slowdown, which is why I’m going for it Catch Classification in this article.

I would like to see SCCO stock drop to $100 before I upgrade it to… He buys once again.

Away

Copper rose on strong demand expectations from green energy investments, AI infrastructure, defense spending, and the restoration of economic support.

These factors have accelerated investor interest, pushing prices to record levels.

However, the rise may be exaggerated. China’s weak real estate sector and lower-than-expected global copper demand could hurt the current recovery

In addition, high copper prices are based on optimistic supply and demand forecasts that may not be fully realized unless the world does its best in the energy transition – and what are the odds of that?

As for SCCO, the company has benefited from these trends, showing strong production growth and impressive revenues.

Despite this, SCCO’s valuation is fairly high.

The recent rise in copper prices indicates a cautious outlook, with the possibility of a cyclical slowdown.

Therefore, I maintain Catch Rating on SCCO, waiting for a more attractive price closer to $100 before considering getting He buys evaluation.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.