tum3123

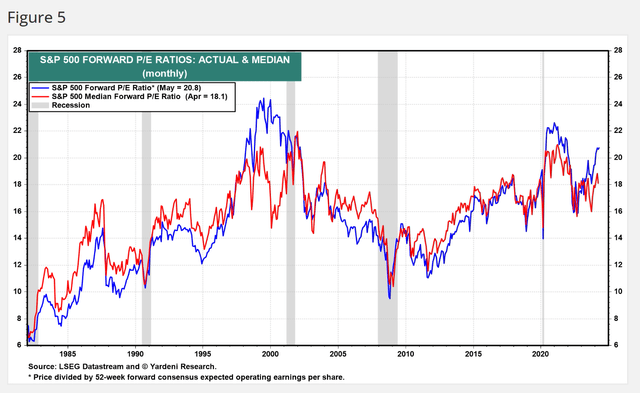

I’ve written a lot recently about extended valuations in US stock markets and how investors can protect their portfolios against potential drawdowns. For example, based on consensus estimates, the S&P 500’s P/E multiple of 21 times is among the highest in its history. History excluding the dot-com bubble and early 2021 (Figure 1).

Figure 1 – US stock valuations extended (Yardeni.com)

These strategies include something as simple as taking profits from big winners to reallocate funds to hedging products like the JPMorgan Hedged Equity Laddered Overlay ETF (HELO) or the First Trust Long/Short Equity ETF (FTLS) that can reduce a portfolio’s downside.

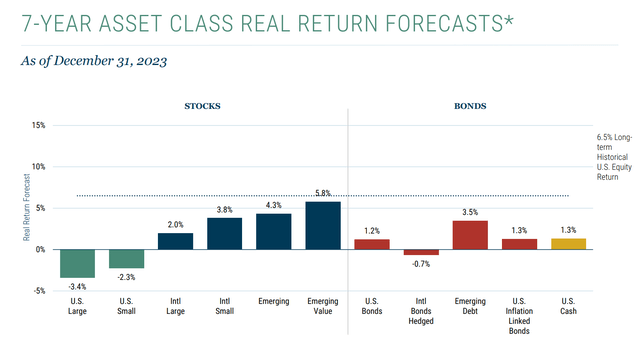

Alternatively, investors can look for markets or niches where valuations are not stretched. According to the cyclical analysis conducted by institutional manager GMO, while US stocks are expected to achieve negative returns over 7 years due to rising interest rates. With valuations, other markets such as emerging markets remain attractive to investors with a long investment horizon (Figure 2).

Figure 2 – Emerging markets remain attractively valued (GMO)

However, with over 100 emerging market ETFs listed on the market, which emerging market funds should investors consider? I think the SPDR Emerging Markets ETF (NYSEARCA:SPEM) is a fund that compares well with its peers.

SPEM ETF charges one of the lowest management fees while consistently delivering second quarter performance or better. Although there is a large allocation to underperforming Chinese stocks, the SPEM ETF has roughly kept pace with an ETF that excludes Chinese stocks.

For investors looking to diversify globally, I recommend taking a look at SPEM.

Fund overview

The SPDR Portfolio Emerging Markets ETF is a low-cost index fund that tracks the S&P Emerging BMI Index (the “Index”). With over 6,000 voters, RThe index is a float-adjusted market capitalization-weighted index designed to capture investables A world of publicly traded companies headquartered in emerging markets.

However, the SPEM ETF does not seek to completely replicate its underlying index. Instead, SPEM uses a sampling methodA strategy that buys a subset of thee securities in the index to create a portfolio with Generally the same risk and return characteristics as the index.

SPEM vs. other emerging market ETFs

Comparing the SPEM ETF to its largest peers, the Vanguard FTSE Emerging Markets ETF (VWO), iShares Core MSCI Emerging Markets ETF (IEMG), iShares MSCI Emerging Markets ETF (EEM), and iShares MSCI Emerging Markets ex China ETF (EMXC), we can see that SPEM is a relatively small company with assets of just $9 billion (Figure 3). However, its costs are the lowest among the peer group, at just 0.07%.

Figure 3 – SPEM vs. Peers, Fund Structure (Searching for Alpha)

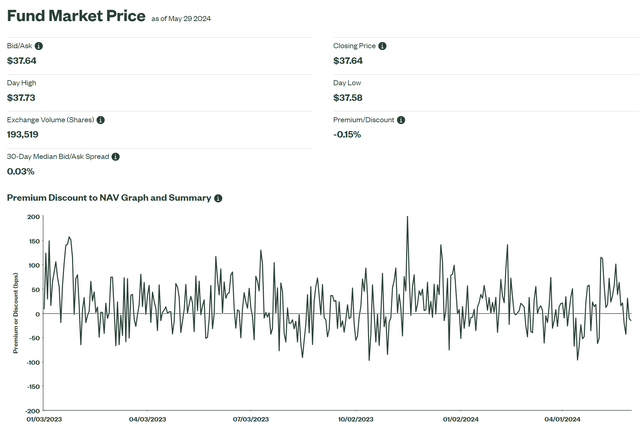

The SPEM ETF is large enough that most investors do not have liquidity constraints, with a bid/ask spread of 0.03% (Figure 4).

Figure 4 – SPEM has a narrow spread between bid and ask (ssga.com)

Meanwhile, the SPEM fund is smart enough to buy companies with a market capitalization of $100 million without affecting stock prices, according to its mandate.

Portfolio overview

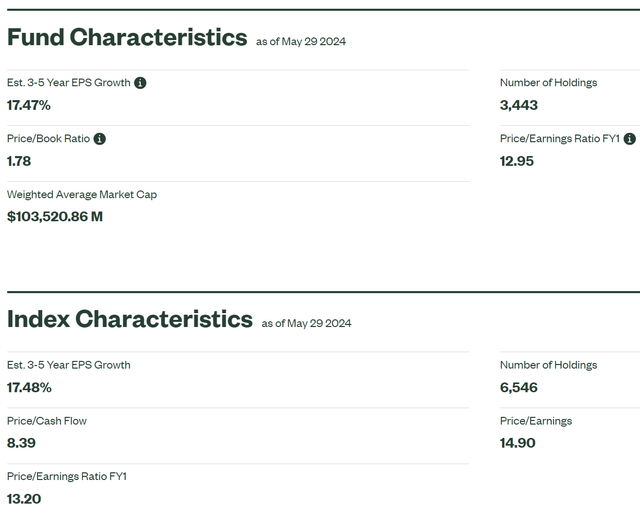

As mentioned above, the SPEM ETF does not fully replicate its underlying index. Instead, it has a basket of more than 3,400 stocks that are expected to have similar characteristics to the index. As of May 29, 2024, the SPEM ETF portfolio has a 3-5 year EPS growth rate of 17.5% and a 13.0x P/E ratio compared to a 17.5% EPS growth rate and 13.2x P/E for the index (Figure 5) .

Figure 5 – SPEM properties versus index (ssga.com)

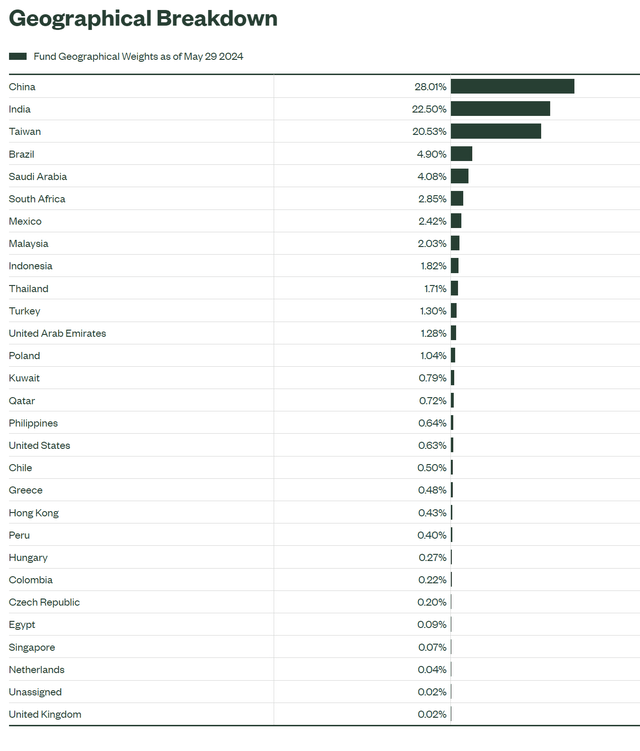

Geographically, the SPEM ETF’s largest allocations are China at 28.0%, India at 22.5%, Taiwan at 20.5%, Brazil at 4.9%, and Saudi Arabia at 4.9% (Figure 6).

Figure 6 – Geographic assignments of SPEM (ssga.com)

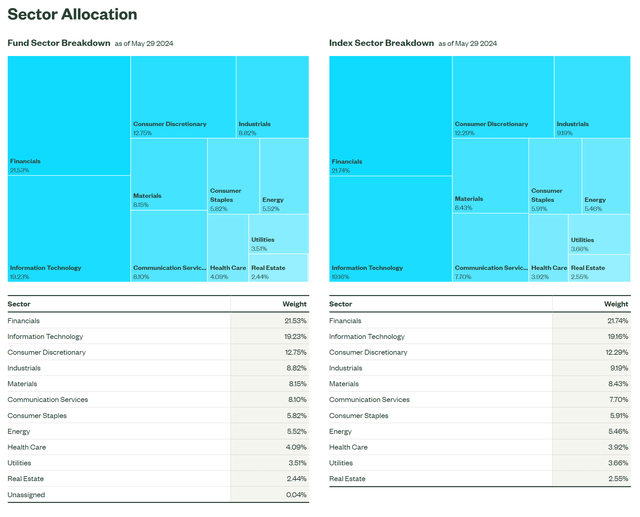

The SPEM ETF is widely diversified in terms of sector allocation, with a 21.5% weight in Financials, a 19.2% weight in Information Technology, a 12.8% weight in Consumer Discretionary, an 8.8% weight in Industrials, and an 8.2% weight in Materials (Figure 7).

Figure 7 – SPEM sector allocations (ssga.com)

Historical returns

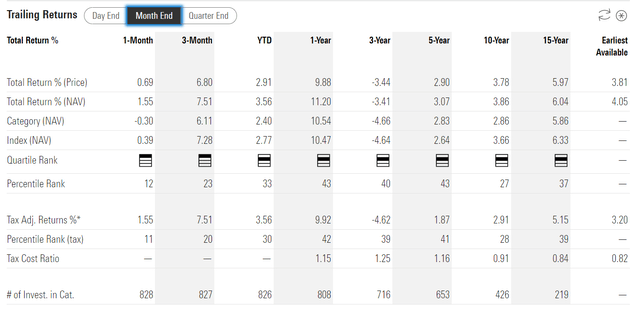

Historically, the SPEM ETF has generated only modest returns, with 3/5/10/15-year average annual returns of -3.4%/3.1%/3.9%/6.0% respectively through April 30, 2024 (Figure 8).

Figure 8 – Historical SPEM Returns (morningstar.com)

However, the problem is mostly due to the relatively poor performance of the emerging market asset class in the past few years due to weak stocks in China, as the SPEM ETF consistently ranks in the second quartile compared to Morningstar. Diversified emerging markets Peers.

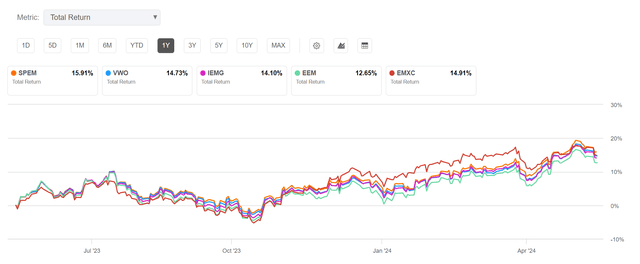

In fact, compared to the larger AUM peers I mentioned earlier, the SPEM ETF performed well, with its one-year total returns of 15.9% compared to 14.7% for VWO, 14.1% for IEMG, and 12.7% for EEM, and 14.9%. For EMXC (Figure 9)

Figure 9 – SPEM versus peers, one-year returns (Searching for Alpha)

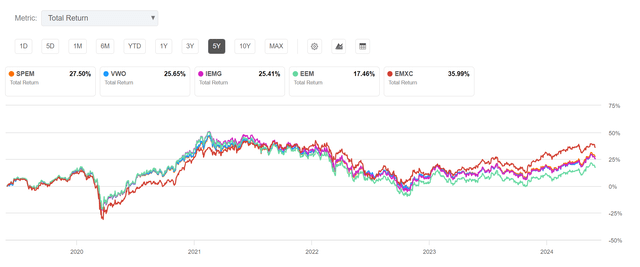

SPEM remains the second best performer on a 3- and 5-year basis, with 5-year returns of 27.5% compared to 25.7% for VWO, 25.4% for IEMG, 17.5% for EEM, and 36.0% for EMXC (Figure 10).

Figure 10 – SPEM versus peers, 5-year returns (Searching for Alpha)

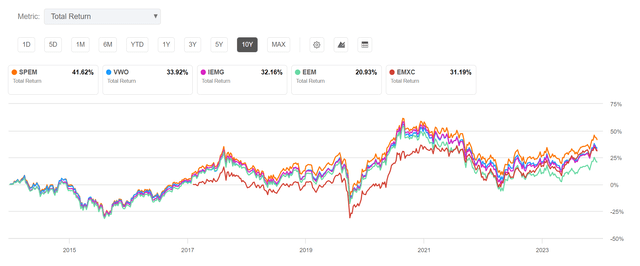

On a 10-year basis, SPEM was the best performer, with 10-year average annual returns of 41.6% versus 33.9% for VWO, 32.2% for IEMG, 20.9% for EEM, and 31.2% for EMXC ( Figure 11).

Figure 11 – SPEM versus peers, 10-year returns (Searching for Alpha)

With or without China?

Keen-eyed readers will note that the best-performing short-term emerging market ETFs mentioned above are EMXC. The iShares MSCI Emerging Markets ex China ETF, as its name suggests, is designed to provide exposure to emerging markets excluding stocks from China.

China has been a hot topic in geopolitical circles, as the Chinese government is a direct competitor of the United States, and several leading Chinese companies such as Huawei and ZTE have been subject to sanctions by the US and European governments.

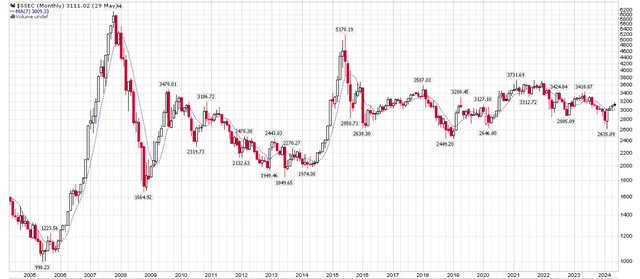

Combined with the fact that Chinese stocks, as modeled by the Shanghai Composite Index, have done nothing over the past few years, it is not surprising that an index fund excluding Chinese stocks outperforms (Figure 12).

Figure 12 – Performance of the Shanghai Composite Index (stockcharts.com)

The big question is whether it is wise to exclude Chinese stocks from the investable universe on a going forward basis. For those who fear escalating geopolitical tensions between the US and China, they should choose EMXC for their exposure to emerging markets.

However, for me, I think the valuations available in the Chinese markets may be worth the risk. For example, the MSCI China P/E is currently just 9.7x versus 12.2x for Emerging Markets and 17.1x for MSCI ACWI (i.e. World) (Figure 13).

Figure 13 – Chinese stocks are cheap (msci.com)

While the geopolitical risks are high, so are the potential rewards.

Furthermore, it is important to note that the SPEM ETF was able to keep pace with the EMXC ETF over one year despite the poor performance in Chinese stocks, which represent about 28% of SPEM’s portfolio. This is like a boxer fighting with one hand tied behind his back.

I believe SPEM’s relatively strong performance is because the fund’s mandate of investing in companies with market capitalizations above $100 million allows it to buy many small-cap capitalizations that other emerging market funds cannot buy with their focused large- and mid-cap mandates. These smaller companies may have better growth prospects and are less closely monitored, allowing investors to outperform.

SPEM risks

The biggest risk to the SPEM ETF is the global economy. While the US economy remains strong, many economists expect the global economy to weaken in 2024. If the global economy weakens, emerging markets will not be immune.

Another risk is geopolitical tensions between the United States and China. Both major US presidential candidates appear to have a tough stance on China, and whoever wins the presidency in November is likely to raise tariffs and new trade restrictions. This could negatively impact Chinese holdings in the SPEM ETF.

Conclusion

With US stock valuations trading near multi-year highs, I think investors should consider diversifying into other markets. Emerging markets, with their cheap valuations, appear to be a good place to allocate long-term capital.

The SPDR Portfolio Emerging Markets ETF is a low-cost emerging markets ETF that compares well with its peers. Her mandate and fund size allow her to buy smaller-capitalization stocks that may have higher growth potential. I rate the SPEM ETF a Buy.