We/DigitalVision via Getty Images

introduction

Prospective investors interested in value-oriented ETFs are spoiled for choice these days, with so many options now on offer; And in this vast universe, we have the S&P 500 Value ETF (NYSEARCA:SPYV), which focuses on stocks from the major index that display the strongest value characteristics.

SPYV vs VTV

To better understand SPYV’s qualities, we felt it would be appropriate to measure it against the largest value ETF on the market – the Vanguard Value ETF (VTV).

Note that even though SPYV has been around for almost 4 years longer than VTV, investors seem to have taken a strong liking to the latter; This can be seen in the explosion in assets under management, which currently stands at nearly $165 billion in AUM, more than 7.5 times larger than SPYV’s corresponding AUM. Even as a commercial medium, VTV tends to gain traction More attention, and this is reflected in the daily volumes shown in dollars, where we have a difference of more than 3x between these two products in question.

So, what could explain the greater popularity of VTV compared to SPYV? Well, the oft-cited theory regarding Vanguard-based products is that they are typically the cheapest within the ETF segment, but that logic isn’t necessarily a major differentiator in this case, as SPYV offers an identical expense ratio of just 0.04%. .

Perhaps investors also appreciate VTV’s relative stability? Last year, it produced only 10% of its total holdings, and the year before it was even lower at 5%. On the other hand, SPYV is more likely to deliver its portfolio at 27% which is somewhat in line with the sector average.

Investors may also be attracted to VTV’s better income profile. For context, over the past three years, it has been growing its dividend at a greater pace of about 9%, compared to a low-single-digit pace for the SPYV. This also means that VTV currently offers a yield approximately 60 basis points better than our Focus product. Its current yield is also not significantly lower than its 4-year average, while the covariance of SPYV with its historical average is quite wide.

YCharts

Most of all, we believe VTV’s popularity can be explained by its more rigorous screening methodology, which ends up following a smaller group of stocks (345 vs. 442 for SPYV).

While both products focus mostly on large-cap stocks (70% of SPYV’s portfolio and 73% of VTV’s portfolio), VTV uses a five-factor methodology to pick its stocks, while SPYV sticks to just 3. SPYV focuses on stocks that have high earnings yield, sales yield, and book value to price basis. VTV also uses these three metrics, but also complements them by incorporating the forward dividend yield, as well as the dividend yield. Crucially, while determining the composite value score, VTV leans more towards book value to price ratios, as well as historical and forward returns (dividend yield and sales yield only account for a third of the total score).

Find Alpha Bullets, ETF

Does VTV’s greatest factor approach make a big difference? Well, the results are mixed. Note that since its listing date in 2004, VTV has managed to outperform SPYV by 1.11x, but if you plug the degree of risk involved into the equation, and look at it from different time periods, the end result is less clear.

YCharts

The Sharpe ratio takes into account how well these two products achieve returns above the risk-free rate after considering the total risks taken. While VTV has performed very well over a 15-year time frame, SPYV has come out on top in the past five years.

YCharts YCharts

A similar result can be seen when you look at these products through the lens of the Sortino ratio, which measures potential excess return in the face of adverse volatility alone. SPYV has a better short-term track record, but VTV has performed better over the past 15 years. Given these mixed results, it is fair to ask whether some additional screening agents for VTV are unnecessary.

Concluding Thoughts – Should You Buy SPYV Now?

While SPYV stacks up well against its larger counterpart (excluding the income angle), we remain conflicted on whether a long position now would be very beneficial. this is the reason.

SPYV is dominated by financial sector stocks, and here there are good and bad things to consider. Given the Fed’s desire to maintain this elevated position for longer, many people have written off the banks’ ability to see broad loan appetite and the associated National Insurance gains. While there may be pressure on the National Insurance front, the other side of business income has proven to be a positive surprise, and this has played a major role in seeing the financial sector perform very well in the recently concluded earnings season.

To expand on this, note that since the end of March, no other sector has managed to deliver more positive revenue growth surprises than the financials sector.

Looking ahead, two-thirds of economists surveyed by Reuters expect the Fed to cut interest rates in September, and that could be music to banks’ ears, given challenging loan growth momentum. Also keep in mind that for the fiscal year, the financials are poised for a sufficiently strong earnings growth of 13%, with only the high-growth technology and communications services sectors offering a better earnings outlook.

FactSet

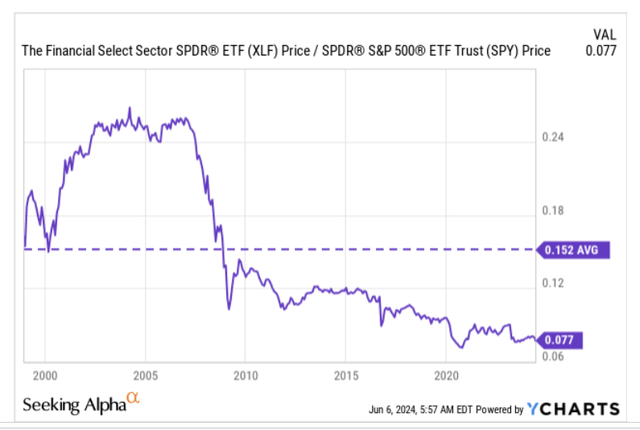

The chart below also indicates that within the universe of the S&P 500, the financial sector looks like quite a worn-out space, with its current relative strength versus the index being only half of its long-term average. As a result, financials would not be a bad bet for some mean bounce.

YCharts

However, despite all this, investors may also want to note that the possibility of increased capital requirements for large banks may prevent them from realizing their true potential. The final Basel III proposals are likely to lead large banks to set aside more capital and push them to withdraw from lending avenues such as mortgages, corporate loans, etc. This situation is still evolving and banks will still have a three-year grace period for repayment. July 2025 to comply with the new framework, but it still seems like a disruptive development.

foot

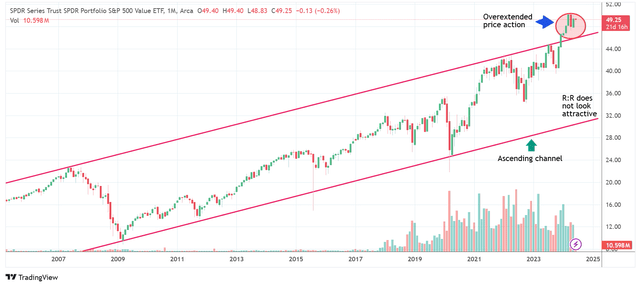

Finally, if we look at the longer-term chart of SPYV, it is difficult to be too excited about starting a long position now, given where the price is currently. Note that for more than two decades, SPYV has trended higher within the confines of an ascending channel; However, since the beginning of the year, we have seen ETFs break through this range, and it is now a long way from the all-time highs. We believe investors should wait for a pullback to their old channel, before considering a buy trade. At these high levels, SPYV is suspended.

Trading offer