PM/DigitalVision images via Getty Images

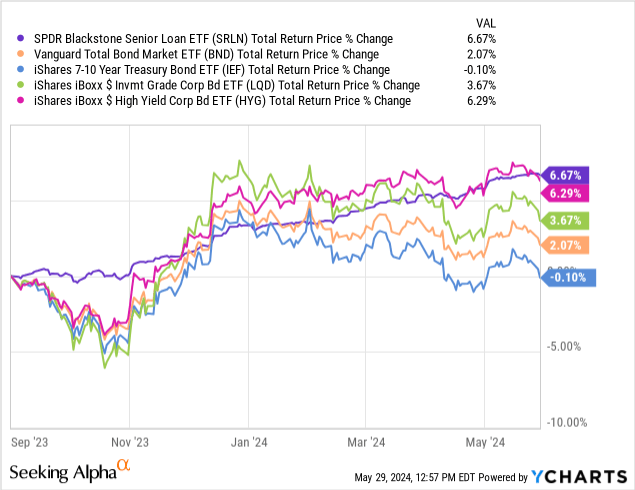

I last covered the SPDR Blackstone Senior Loan ETF (SRLN), an actively managed senior loan ETF, in late 2023. In that article, I argued that SRLN’s strong, rising yield and low price risk made the fund a buy. SRLN It has posted reasonably good returns since then, outperforming most bonds and bond sub-asset classes, and seeing dividend growth. Performance has been very good, generally in line with expectations.

SRLN continues to offer investors a strong dividend yield with low price risk, so the fund remains a buy. However, it remains a somewhat risky option, with high credit risks.

SRLN – The Basics

- Investment Manager: State Street

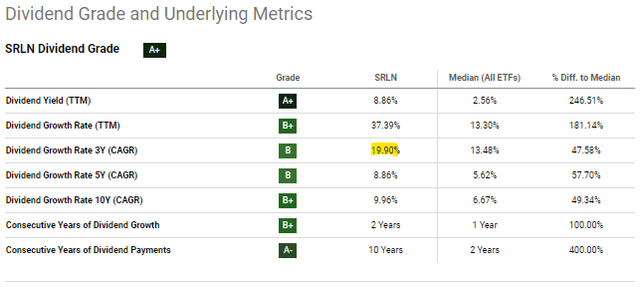

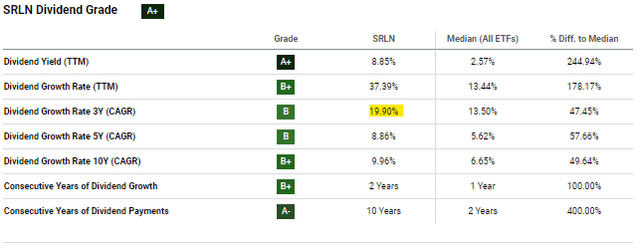

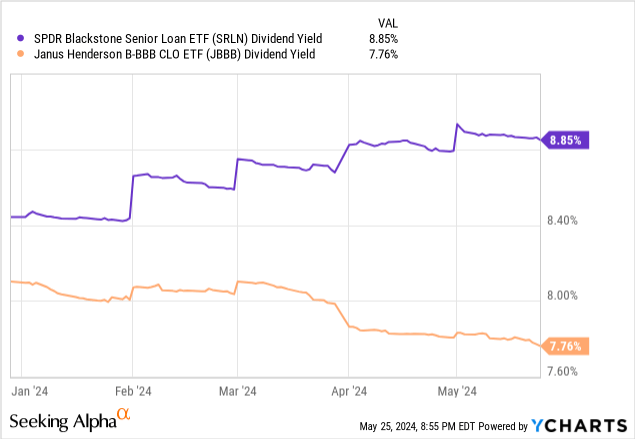

- Dividend yield: 8.85%

- Expense ratio: 0.70%

- Total returns at 10-year CAGR: 3.43%

SRLN – Overview and Analysis

Strategy and portfolio

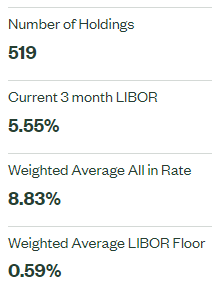

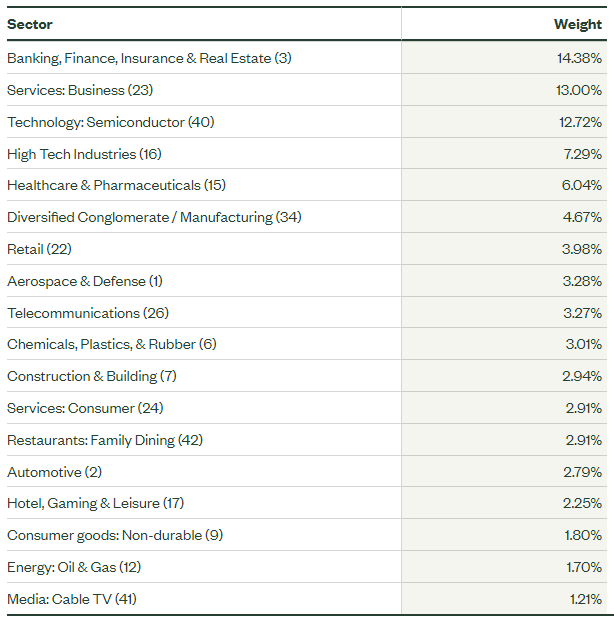

SRLN is an actively managed ETF focused on Senior loans, which are variable interest loans secured by non-investment grade companies. SRLN provides investors with diversified exposure to these securities, with investments in over 500 loans from several sectors.

SRLN SRLN

That said, SRLN is much less diversified than many of the largest bond ETFs on the market, including the Vanguard Total Bond Market Index Fund ETF (NASDAQ:BND) and the iShares Core US Aggregate Bond ETF (NYSEARCA:AGG), where That these exposure to several Sub-asset classes of bonds.

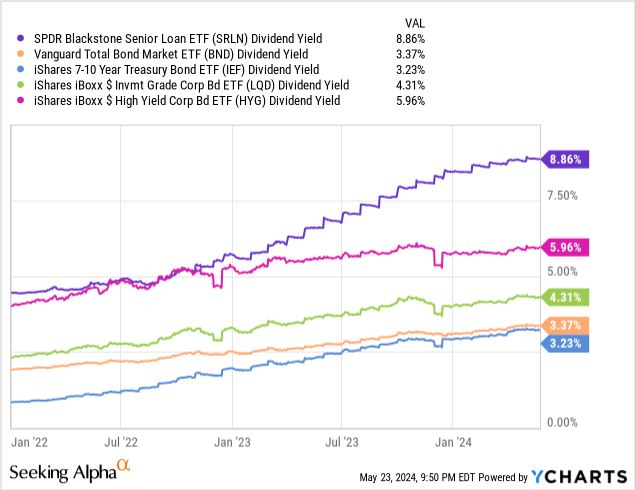

Strong dividend yield of 8.9%

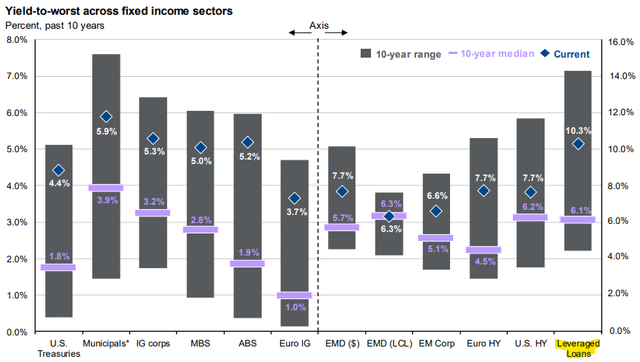

The Fed hike has led to higher interest rates across the board. Senior loans were one of the biggest beneficiaries of these loans Factor Interest rates on loans. Interest rates on senior loans have risen about 4.2% over the past few years, which is well above average.

JP Morgan Guide to the Markets

SRLN’s earnings have also seen tremendous growth over the past few years, in line with the above.

SRLN

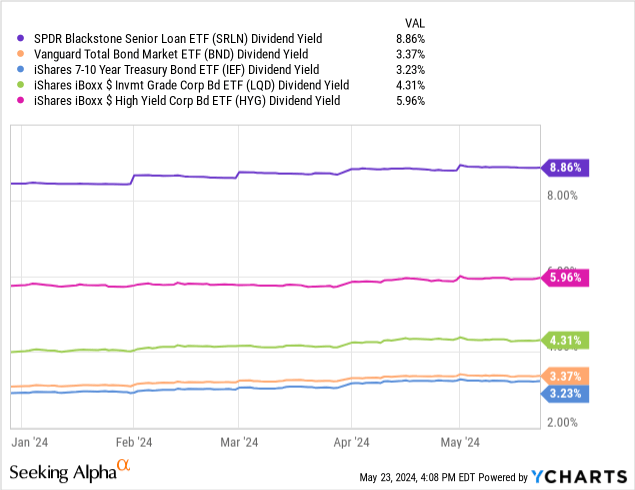

Currently, the fund has a dividend yield of 8.9%, which is very strong on an absolute basis, and higher than most bonds and bond sub-asset classes.

Data by YCharts

SRLN’s strong 8.9% dividend yield is a significant benefit to shareholders, and the fund’s main advantage over its peers.

As is the case with most bond or loan funds, dividends should fall as the Fed cuts interest rates later in the year. Dividend cuts should be rapid, and of a similar size to interest rate cuts: if the Fed cuts 1.0%, dividends should fall by 1.0%. Investors should be able to stabilize interest rates by focusing on long-term bond funds, but they will no Do this by investing in SRLN.

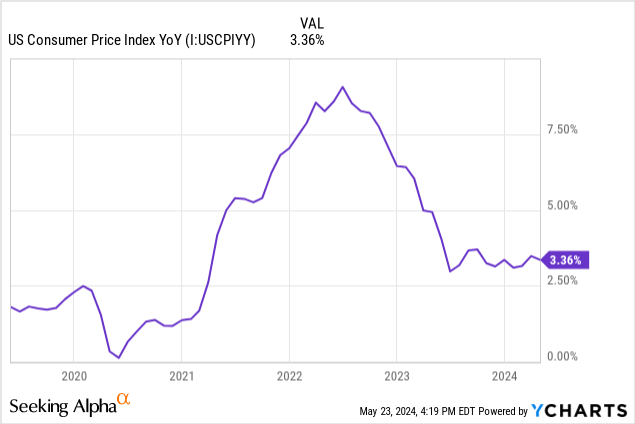

In my opinion, lower interest rates are almost certain to happen at some point in the future, but I do not expect large, rapid interest rate cuts. Inflation remains consistently above target and has remained steady for about a year. Under these circumstances, interest rate cuts seem unlikely in the near term. Powell seems to agree, arguing much the same after the April CPI report.

Data by YCharts

Since SRLN trades with a healthy spread compared to its peers, interest rate cuts would have to be very large for the fund to start earning a lower return than its peers. Under current circumstances, this does not seem likely at all in the next two years or so, to say the least. However, much will depend on the Fed’s policy going forward.

Credit risk

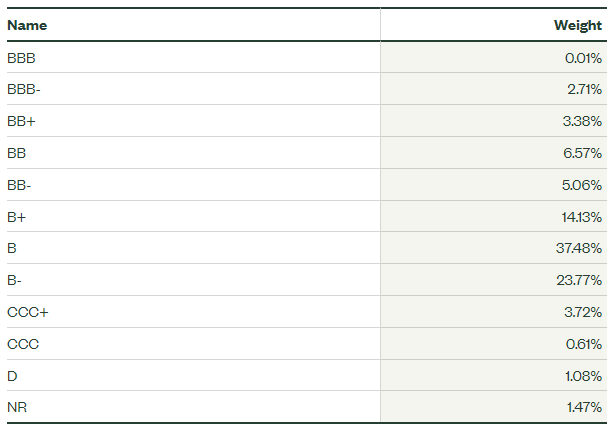

Senior loans almost always come from non-investment grade companies. These are relatively weak companies, with poor credit ratings. SRLN itself focuses on B-rated loans, a relatively weak rating, even for high-yield ETFs. From previous coverage, most of SRLN’s peers focus on BB-rated bonds/loans.

SRLN

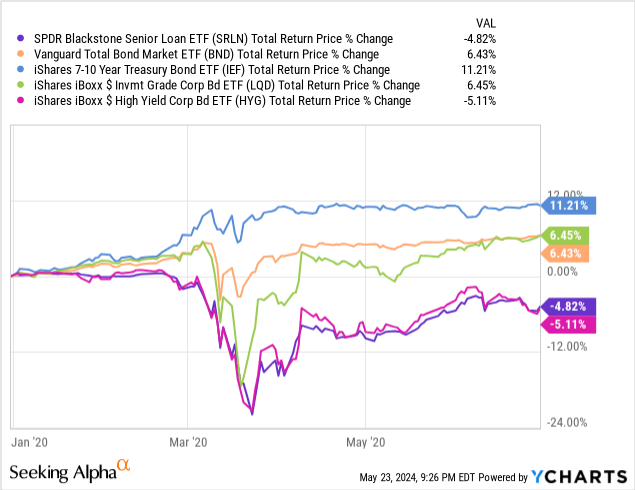

SRLN issuers are generally able to meet their financial obligations without any problems nowBut most of these countries may start to face trouble if economic conditions deteriorate, and default rates rise. As such, expect significant above-average losses for SRLN during downturns and downturns, as was the case during early 2020. The losses were not materially different from high-yield corporate bond losses, and even somewhat exceeded expectations.

Data by YCharts

SRLN’s higher-than-average credit risk is a significant negative for the fund and may be a deal-breaker for more risk-averse investors.

Interest rate risk

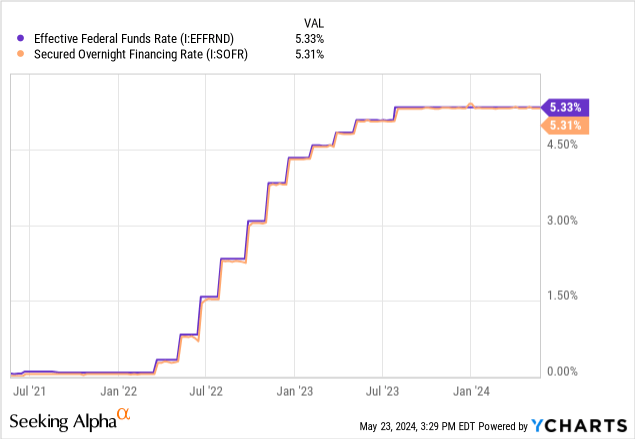

Senior loans are almost always available Variable rate Loans, are indexed at specific rates, so we see higher coupon rates when those rates rise. Prices generally reset every three months. Most of them are indexed to the SOFR, which, for our purposes, is functionally identical to the Federal Reserve funds rate.

Data by YCharts

Therefore, premium loan coupon rates fluctuate along with federal interest rates every quarter. Remember that most bonds have fixed interest rates from issuance to maturity, unlike senior loans.

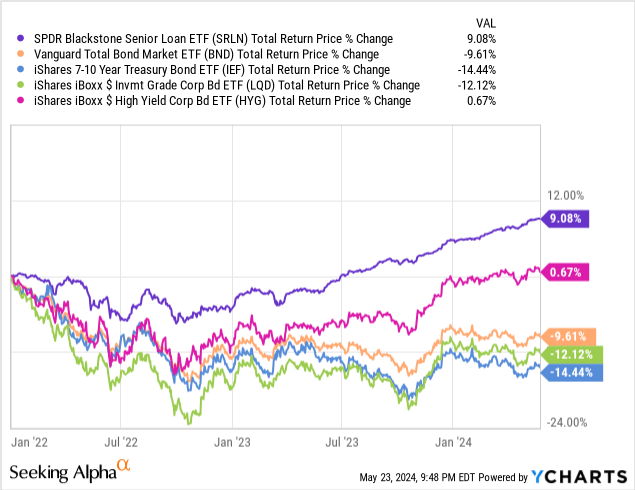

SRLN focuses on senior loans, so interest rate and duration risks are negligible, like these securities. Expect below-average losses and outperformance when interest rates rise, as has been the case since early 2022.

Data by YCharts

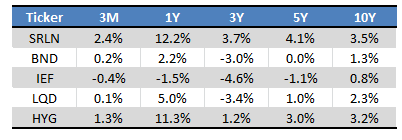

At the same time, the fund’s earnings should increase much more quickly than those of its peers when interest rates rise. For example, SRLN has seen four times earnings growth compared to the $iShares iBoxx High Yield Corporate Bond Fund (HYG), the largest high-yield corporate bond ETF, over the past three years.

SRLN Growth:

Seeking alpha

HYG Growth:

Seeking alpha

This is also quite evident when comparing SRLN’s return to the returns of its peers since early 2022. SRLN’s return has increased by more than average, and this is especially easy to see when comparing the fund to HYG.

Data by YCharts

On the more downside, as mentioned earlier, SRLN earnings should decline when the Fed starts cutting interest rates. Dividend cuts should be rapid, and of a similar size to interest rate cuts. Since SRLN trades with a healthy spread to its peers, see above, interest rates would have to fall much lower for the fund’s earnings to become uncompetitive. In my opinion, this is unlikely to happen in the short term.

Performance scorecard

SRLN’s track record is reasonably good, with the fund consistently outperforming its peers.

Searching for Alpha – table by author

Some other comments on the above.

SRLN’s long-term returns are very low, as have been the rates a lot less in the past. Recent defaults and price losses were also partly responsible.

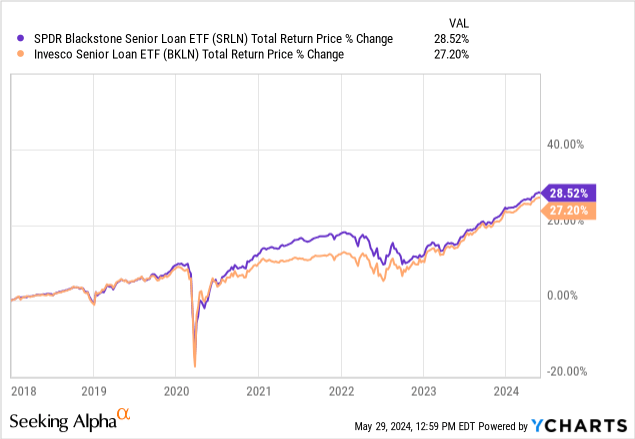

SRLN’s medium-term returns are slightly weaker than expected. 3Y returns He should be higher, as rates have been reasonably high over the past three years. I’m not entirely sure why this happened, but I think a combination of timing and changes in credit spreads played a role. When I compare SRLN to the Invesco Senior Loan ETF (NYSEARCA:BKLN), I see relatively strong returns through 2021, weaker returns through 2022, and similar long-term returns. This pattern is consistent with/explains SRLN’s relatively weak 3-year returns.

Short-term SRLN returns are very strong, due to a combination of higher interest rates and tighter credit spreads. As long as interest rates remain high, returns should remain reasonably good in the future. It is unlikely to achieve double-digit annual returns, at least over the long term, as credit spreads cannot be tightened continuously, and the fund does not have a double-digit return.

Overall, SRLN’s track record is reasonably good, although a little weaker than I would expect for a variable rate fund.

SRLN vs JBBB – quick comparison

Longtime readers know I’ve been bullish on CLO debt ETFs for years, due to their high returns and low overall risk. These are very similar to the SRLN, so consider doing a quick comparison. I’ll focus on SRLN and the Janus Henderson B-BBB CLO ETF (BATS:JBBB), which focuses on BBB-rated CLOs below.

Both SRLN and JBBB focus on variable rate investments. Interest rate and duration risks are negligible for both.

Both are fairly expensive funds, SRLN a bit more. SRLN has an expense ratio of 0.70%, compared to JBBB’s 0.49%.

SRLN’s credit risk is much higher, as the fund focuses on non-investment grade loans, compared to JBBB’s investment grade holdings. Default rates for collateralized loan obligations are also incredibly low, reducing the fund’s credit risk.

Both funds have strong above-average dividend yields. However, the SRLN yield is higher at over 1.0%. More on this later.

Data by YCharts

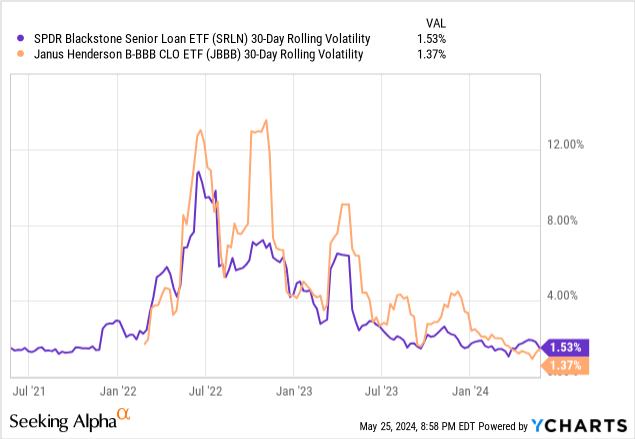

Overall, the SRLN is a broadly volatile and risky option, given the focus on non-investment grade loans. GBPP He should It is a safer and more stable option, taking into account the characteristics of the underlying CLOs. In practice, the volatility is similar to that of the SRLN. In my opinion, this is because collateralized loan obligations are fairly illiquid investments and are viewed as very risky.

Data by YCharts

Notwithstanding the foregoing, the actual credit risk of most investment grade collateralized loan obligations is very low, which should reflect favorably on JBBB stock prices and returns over the long term.

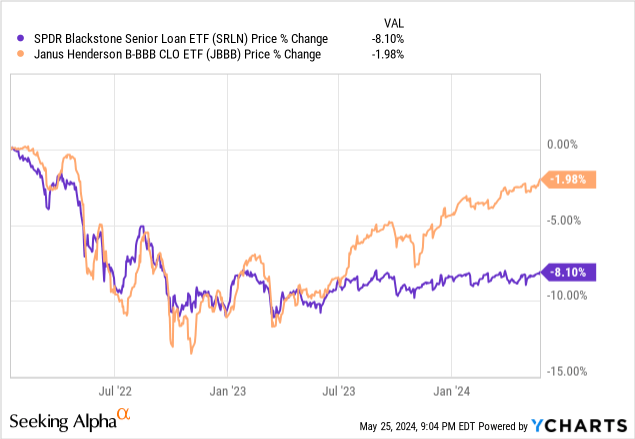

For example, both SRLN and JBBB saw some capital losses/stock price declines in 2022, due to higher default rates (to some extent) and bearish market sentiment. JBBB’s share price has rebounded steadily since mid-2023, while SRLN has not. Given the fundamentals, JBBB’s stock price should be as well no It is down, but the short-term decline is not also Far from expectations.

Data by YCharts

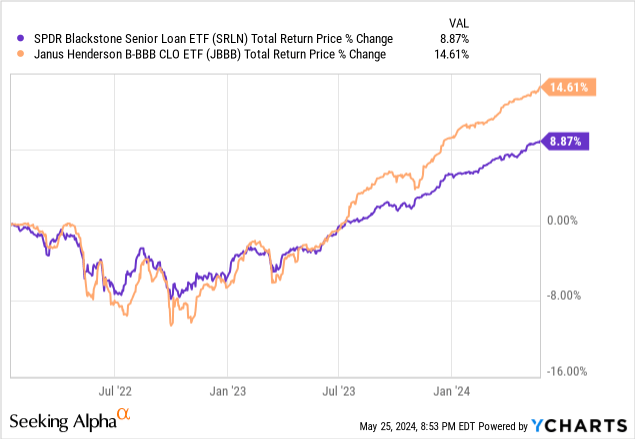

In my opinion, given current market and industry conditions, JBBB should deliver higher long-term returns than SRLN. This has been the case from the beginning, as expected.

Data by YCharts

Overall, JBBB looks a little better than SRLN. I maintain a Buy rating on SRLN as is strong Investment opportunity as a whole, but it looks JBBB more powerful.

Conclusion

SRLN’s high 8.9% dividend yield, low rate risk, and recent strong performance make the fund a buy.