Emanuel M. Schwermer

Over the past few months, things have gone well for shareholders Standex International (New York Stock Exchange:SXI). For those who are not familiar with the company, it operates as a diversified player in the industrial manufacturing space. It produces a wide range of Products, including sensing and switching technologies such as magnetic energy conversion components and similar offerings that can be used in security products, devices, medical products and more. They also provide custom materials and surface finishes that are used in tools, as well as produce specialized temperature control equipment for the medical industry, industrial companies, and more. In addition, it also sells products that go into building fuel tanks, rocket engine components, spacecraft structures, power production turbines, and more. The list of examples goes on from here, but you get an idea of how versatile this project is.

When I say things have gone well, this is in reference to the time window from the last time I wrote about the company in November of last year to the present day. At the time, I rated the company a “Buy” to reflect my view that shares should outperform the broader market for the foreseeable future. This was based on the growth expectations for the company as set forth by management, as well as how the shares were priced. However, the ‘Buy’ rating was a weak ‘Buy’, which reflects my belief that the outperformance will not be astronomical. And that’s exactly what we saw. Since this article was published, shares have risen 27.2%. This is comfortably higher than the 18% increase the S&P 500 saw over the same time period.

Given this upside, as well as the fact that fundamentals have continued to change since that article was published, I thought it would be wise to reconsider the action at this time. What I found is that although I still believe in the long-term outlook for the company, the shares appear to be at least fairly valued and perhaps a bit overpriced. For this reason, I have decided to downgrade the work to “Hold” for the time being.

It’s time to downgrade

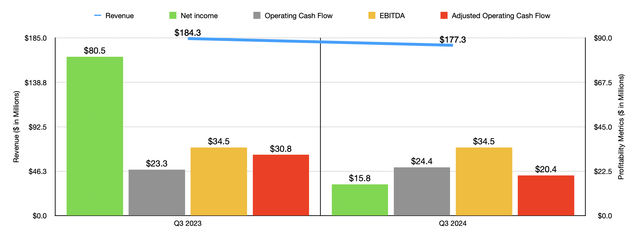

Fundamentally, Standex International remains an interesting and profitable company. However, I would be lying if I said that everything since I last wrote about the company has been great. The fact of the matter is that some financial performance has been on the weak side of things. For example, we only need to look at revenue covering the third quarter of fiscal 2024. During that period, sales totaled $177.3 million. This is 3.8% less than the $184.3 million generated one year ago. Interestingly, the picture would have been worse had it not been for some of the company’s acquisitions.

Author – SEC EDGAR data

Organic sales, for example, followed at $10.5 million year over year. This 5.7% decline was due to headwinds in the company’s end markets, which management described as “temporary.” In particular, demand was lower in the electronics and scientific sectors. On the other hand, acquisitions impacted the company positively, reaching $10.6 million. However, the business liquidations amounted to $5.5 million. In addition, the Company received approximately $1.6 million as a result of foreign currency fluctuations.

With revenues down, it should not be surprising that profitability has suffered. Income decreased from $80.5 million to $15.8 million. However, this requires a little clarification. The fact of the matter is that in the third quarter of 2023, Standex International made a profit of $62.1 million from the sale of business operations. But even without that, the company’s profitability would have fallen slightly, with pre-tax income excluding that gain falling from $24.3 million to $15.9 million. Other profitability metrics were much more stable. For example, operating cash flow increased from $23.3 million to $24.4 million. But if we adjust for changes in working capital, we get a decrease from $30.8 million to $20.4 million. Meanwhile, EBITDA remained flat year over year at $34.5 million.

Author – SEC EDGAR data

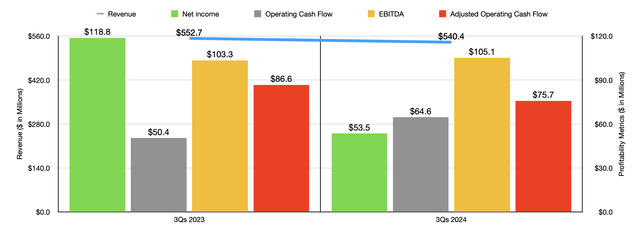

The third quarter wasn’t the only period when the business saw some weakness. For the first nine months of 2024 as a whole, revenues totaled $540.4 million. This represents a 2.2% decline from the $552.7 million the company generated one year ago. This was despite the fact that the company benefited from acquisitions worth $28.8 million. Organic sales revenue decreased by $20.1 million, while divestitures amounted to $21.3 million. Obviously, these more than offset the benefit of the above acquisitions. Other profitability metrics were mixed. For example, net income fell by more than half from $118.8 million to $53.5 million. As you can see in the chart above, one of the company’s three cash flow metrics has worsened year over year.

Author – SEC EDGAR data

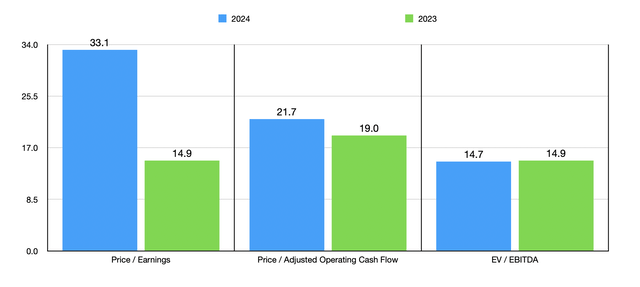

Unfortunately, management has not provided any detailed guidance for the rest of fiscal 2024. But if we analyze the year-to-date results, we expect net income of about $62.6 million, adjusted operating cash flow of about $95.3 million, and total EBITDA $141.9 million. With these results, plus the historical numbers for 2023, I was able to value the company as shown in the chart above. These multiples indicate to me that the stock is at least fairly valued. In the same chart, you can see how the stock was priced when I last wrote about the company. On an absolute basis, there’s no denying that the stock has become more expensive. But shares are also more expensive compared to similar companies. In the table below, I’ve compared them to five such companies. When it comes to both the price-to-earnings approach and the price-to-operating cash flow approach, three of the five companies were cheaper than Standex International. This number increased to four of the five companies when using the EV to EBITDA approach.

| a company | Price/earnings | Price/operating cash flow | Value added/EBITDA |

| Standex International | 33.1 | 21.7 | 14.7 |

| Tennant Corporation (TNC) | 17.3 | 12.3 | 11.0 |

| Enerpack Kit (EPAC) | 30.3 | 28.9 | 16.8 |

| Kennametal (KMT) | 19.5 | 7.2 | 8.8 |

| Barnes Group (B) | 455.2 | 26.9 | 14.4 |

| Hillman Solutions (HLMN) | 721.0 | 8.5 | 13.6 |

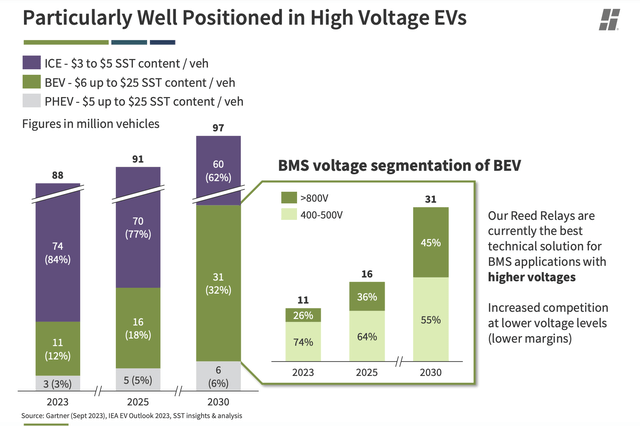

With numbers like these, I cannot in good faith rate the business higher than “hold” at this time. But that doesn’t mean I’m pessimistic about the business in the long term. The fact of the matter is that the company has a lot to do. One of the things management has tried to convey to investors is that the company should benefit, for example, from continued growth in electric vehicle adoption. As you can see in the image below, the number of vehicles produced annually is expected to grow from 88 million on a global scale in 2023 to 97 million by 2030. The share of electric vehicles, especially BEVs (battery electric vehicles) is expected to grow from 12 % only to 32% during this time window. As the image shows, the amount of content the company produces per vehicle is likely to be much greater than it was for internal combustion engines. This can open up significant revenue opportunities for the company.

Standex International

Of course, this is not just an electric car toy. A diverse company like this can only be multiple plays. The fact of the matter is that management believes in the company’s growth potential across multiple different markets. For example, they believe the electronics sector has industry-wide potential of $5 billion or more on an annual basis. In 2023 alone, the company generated $306 million just from this part of the project. Other market opportunities are much smaller. But they are nothing to scoff at. For example, the engraving segment operates in a market worth more than $500 million, with the company generating sales of just $152 million from this space last year. The scientific sector is much smaller, generating just $75 million in revenue in 2023. But the market potential, at more than $700 million, is very large. The same can be said for the engineering technology sector, which was responsible for just $81 million last year but operates an industry worth more than $700 million annually. Finally, the Specialized Solutions segment was responsible for $127 million in adjusted revenue. It operates in an industry worth more than a billion dollars. It appears that about 60% of this opportunity is in custom cranes.

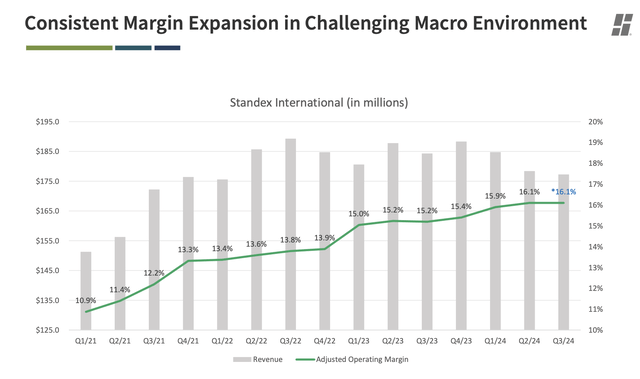

In fact, management asserts that there is a real opportunity for the company to grow its revenues to $1 billion annually or more by 2028. And if the past is any indication of the future, profit margins should expand during this time. Going back to the first quarter of 2021, for example, Standex International showed an adjusted operating profit margin of 10.9%. That number rose to 16.1% as of the third quarter of fiscal 2024. But if all goes according to plan, by the time the company’s sales reach $1 billion, its adjusted operating profit margin is expected to expand to 19% or more.

Standex International

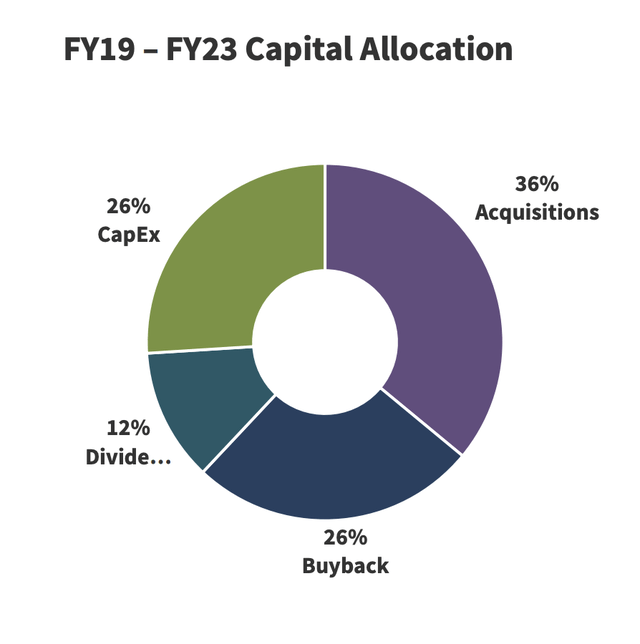

Naturally, this will not be an easy task for the company to achieve. Significant investments will be required in order to gain this kind of upside. However, the administration is no stranger to this. From 2019 through 2023, Standex International allocated about 36% of its cash flow to acquisitions. This is in addition to 20% allocated to capital expenditures. 26% of the cash flow was used to buy back shares during this period, while the remaining 12% was allocated to dividends. This indicates that management is trying to reward shareholders directly while at the same time focusing on growth. This is usually a positive for most investors.

Standex International

He stays away

Fundamentally, things are good, but not great when it comes to Standex International. The company has seen some weakness recently. Having said that, I think this possibility will yield good results in the long term. But that doesn’t mean it makes sense to hold stocks. The fact of the matter is that the stock has seen some fairly significant upside since I came out with a bullish rating on it late last year. Given how much the stock has rallied, as well as the weaknesses mentioned above, I think it’s time to finally downgrade the stock to ‘hold’.