Peshkov

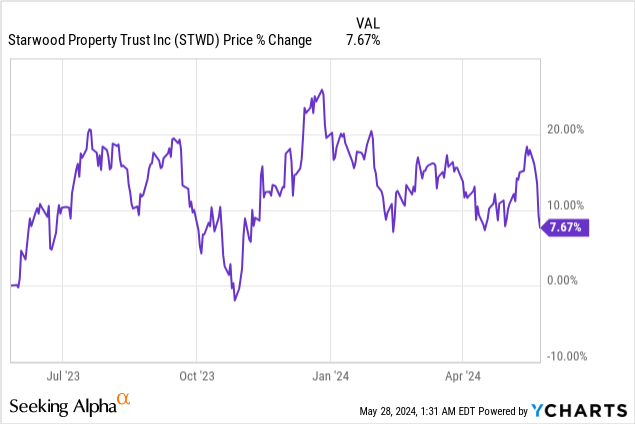

Starwood Property Trust (New York Stock Exchange: STUD) is a solid choice for dividend investors in the commercial real estate market: Starwood Property supported its dividend with distributable profits in the first fiscal quarter and the company has significant access to liquidity that… It could make the REIT a net buyer of commercial mortgage assets in the future. Starwood Property suffered a drop in valuation last week as redemption issues affecting the non-traded Starwood Real Estate Income Trust were reported last week, reintroducing worries and concerns about the state of commercial properties into the market. I believe the redemption limitations are an isolated issue that does not affect publicly traded Starwood Property shares. The REIT also has relatively little exposure to distressed US office loans, making Starwood Properties one of the safest options in the commercial real estate market, in my opinion.

Previous evaluation

I rated Starwood Property stock a Strong Buy in early March given its well-performing REIT loan portfolio and high dividend yield: Earn a 9.4% yield on autopilot. Additionally, Starwood Property shares are priced below book value, which again I think is unfair considering the REIT has no distribution coverage issues and a well-structured portfolio. I think the risk profile is still broadly skewed to the upside here, especially now that investors are overreacting to the SREIT issue.

Diversified portfolio, access to liquidity and SREIT problems

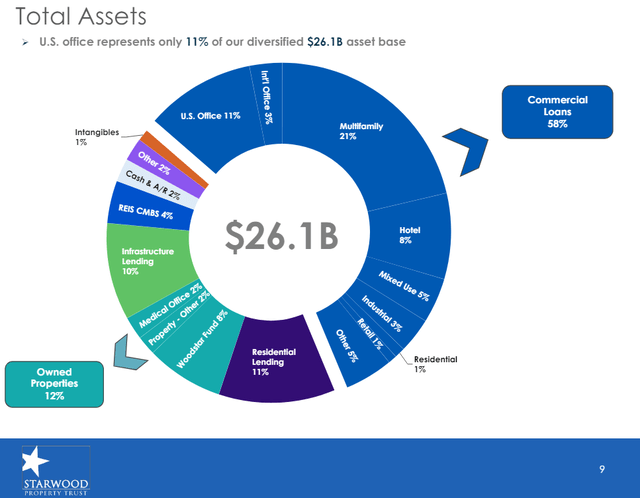

Starwood Property is a well-managed, highly diversified REIT with a relatively low amount of investments in the challenging US office market. US offices represented only about 11% of all investment assets on Starwood Property’s balance sheet at the end of the March quarter, and REITs remained generally well diversified with investments in commercial and residential lending (the largest sector, responsible for 69% of assets). Infrastructure lending, owned real estate, real estate investment and services.

Starwood property

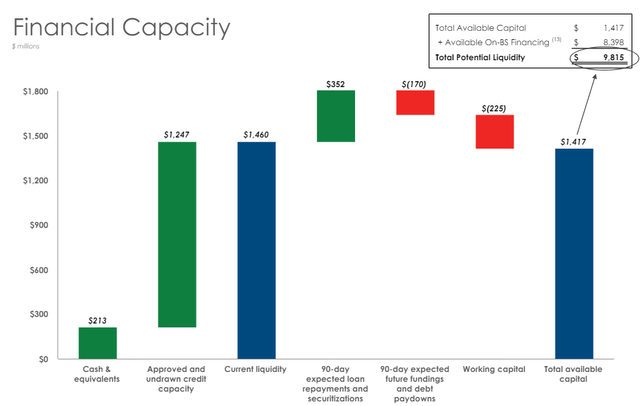

Starwood Property’s primary strength is that it is the largest commercial real estate investment trust in the United States and therefore has access to a significant amount of liquidity that the company can deploy to grow its distributable earnings, especially in times of stress. Starwood Property had $9.8 billion in potential liquidity available as of the end of the first quarter of 2024, which would make STWD a significant force on the acquisition front.

Starwood property

Starwood Property has, over time, proven to be quite opportunistic and specifically seeks market positions that other investors avoid. With a commercial REIT having significant firepower, I believe this money could be used to buy cheap distressed real estate assets in the future. One area I see Starwood Property becoming more active in is the office market, which is currently experiencing declining occupancy rates in office buildings due to remote work trends.

I said in the introduction that Starwood Property is a promising investment candidate now that shares have fallen below $19, which means a 10% dividend yield. Shares of Starwood Property fell from about $21 to $19 last week due to liquidity issues at one of Starwood Property’s non-traded private REIT vehicles, Starwood Real Estate Income Trust (SREIT)…which manages nearly $10 billion for investors .

The REIT has limited the ability of investors to redeem their investments in non-traded REITs (reducing redemptions to 0.33% of net assets per month), causing widespread concerns about potential cheap sales. According to news reports, Starwood Real Estate Investment Trust had to tap a $1.3 billion credit facility in the first quarter of 2024 to meet redemption requests, and just last week it tightened redemption requirements in an effort to preserve liquidity and avoid forced asset sales.

Last week, concerns about losses at Starwood Real Estate Income Trust began to impact Starwood Property prices. However, these problems should not affect Starwood Property, whose shares are traded on the public markets. Looking at the following distribution coverage analysis, I don’t think investors need to be concerned here.

Distribution coverage analysis

Starwood Property’s distribution coverage looked as good as ever in the fiscal first quarter, mainly due to strong performance in the real estate investment trust’s core commercial and residential lending segment. The segment generated distributable earnings of $0.59 per share in Q1 2024 which was more than enough to support the current dividend of $0.48 per share. The resulting distribution coverage ratio was 1.23x in the first quarter of 2024, meaning Starwood Property generated 23% more distributable earnings than it needed to cover its quarterly dividend. The distribution coverage trend is also positive and actually shows signs of improvement compared to previous quarters.

| Distributable earnings, per share | S2’23 | S3’23 | S 4’23 | S1’24 | middle |

| Commercial and residential | $0.56 | $0.64 | $0.63 | $0.63 | $0.62 |

| infrastructure | $0.06 | $0.03 | $0.07 | $0.06 | $0.06 |

| Property | $0.07 | $0.07 | $0.07 | $0.18 | $0.10 |

| Reese | $0.07 | $0.05 | $0.10 | – | $0.07 |

| Big company | ($0.27) | ($0.30) | ($0.29) | ($0.28) | ($0.29) |

| Total de | $0.49 | $0.49 | $0.58 | $0.59 | $0.54 |

| distribution | $0.48 | $0.48 | $0.48 | $0.48 | $0.48 |

| coverage | 102% | 102% | 121% | 123% | $1.12 |

(Source: Author)

Cheap evaluation

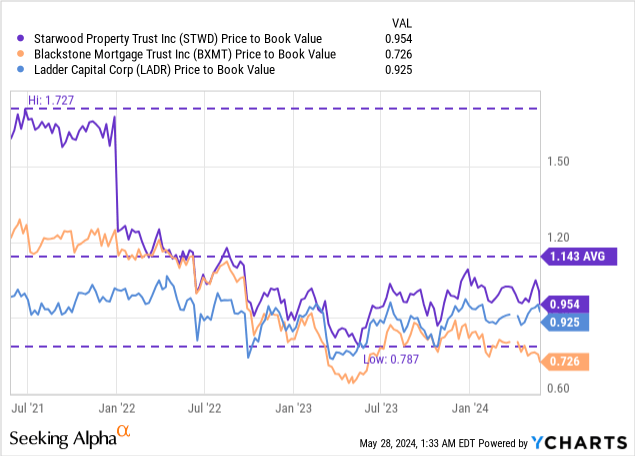

Last week’s sell-off has made Starwood Property cheaper, and shares can now be bought at a solid 5% discount to book value. The 5% discount is still the lowest in an industry group that includes Blackstone Mortgage Trust (BXMT) and Ladder Capital (LADR). The decline in valuation, in my opinion, is temporary and can be reversed once investors calm down about the liquidity demands made by the SREIT. Starwood Property shares are also now trading at 17% below the long-term (3-year) average P/B ratio. My fair value estimate for STWD is $19.85 per share (equivalent to the REIT’s GAAP book value), so the stock has a 5% upside to book value and a 19% upside to the long-term average valuation of 1.14XP/B.

Risks Related to Starwood’s Ownership

As I said above, the SREIT’s liquidity crunch shouldn’t have had any impact on publicly traded Starwood Property. The SREIT’s problems relate to redemptions, which is not an issue for Starwood Property. Quite the opposite: Redemptions are never a problem for publicly traded REITs, as the market provides enough liquidity for investors to sell their shares if they choose to do so. What might change my opinion about Starwood Property is if the REIT saw a sharp deterioration in its distribution coverage ratio, or if it saw a sudden decline in balance sheet quality.

Final thoughts

Every now and then a buying opportunity arises out of nowhere, and I believe that is the case here today with Starwood Property. The REIT’s stock price recently fell below $19, pushing Starwood Property’s dividend yield to over 10% due to the SREIT’s change in redemption rules. I believe that the SREIT’s issues should not have impacted Starwood Property’s valuation and that the risk profile is more skewed to the upside considering that the REIT has only recently reported very strong distribution coverage, primarily due to outstanding commercial and residential lending performance. I am a buyer here!