Mascot/Digital Vision via Getty Images

In our latest assessment, we decided to downgrade Stefanato Group (New York Stock Exchange: Stephen) classification because of ‘Destruction risk and assessment.‘ As a reminder, after checking the low sales growth estimates of Stefanato’s peers in 2024 and forecasting a decline In EBITDA and net profit due to start-up costs and unfavorable exchange rate impact, the company’s valuation was complete in our view.

no sooner said than done. After analyzing fiscal year 2023, Stefanato’s stock price fell approximately 30%. However, we still view the company positively, due to the following considerations: 1) Secular tailwinds In demand for biological materials, 2) Recent expansion of free float at $26 per share (this will support equity liquidity and the company’s capex plan), and 3) Margin expansion supported by economic moat.

Stefanato Group classification update

First quarter results and routing changes

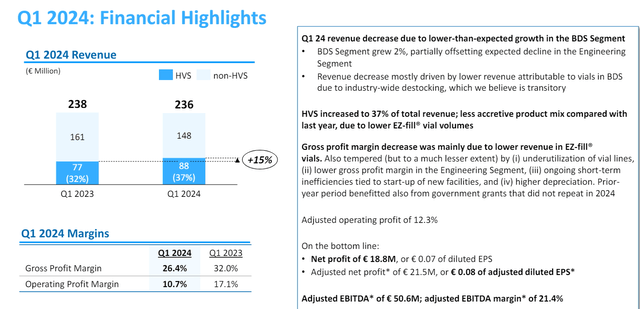

After the first quarter came in below expectations, the company decided to review its estimates. Looking at the numbers, Stefanato recorded a turnover of 236 million, with minus 1% between January and March 2023. Turning to profit and loss, the company’s EBITDA and net income reached EUR 62.2 million and EUR 18.8 million, with minus -18 . % and -33.5%, respectively. This brought first-quarter EPS to 7 cents per share. Lower orders and weaker first-quarter results led the company to adjust its guidance for 2024. In terms of business, sales are down mainly as bottle volumes decline, which the company believes is temporary.

Stefanato Q1 results

Chart 1

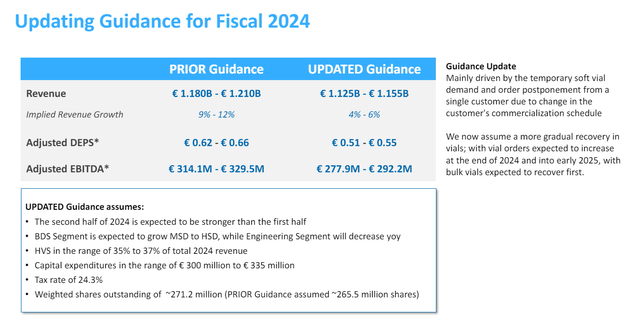

As a reminder, Stefanato was expecting to close “2024 sales between €1.18 and €1.210 billion, with adjusted EBITDA between €314.1 and €329.5 million, and adjusted earnings per share between €0.62 and €0.66.” Currently, sales are expected to be between EUR 1.12 and EUR 1.15 billion, and the EBITDA range has been revised with a new forecast of EUR 278 to EUR 292 million. Finally, the downsizing also includes the company’s earnings per share in a range of €0.51 to €0.55 per share.

New Stefanato Directives 2024

Picture 2

Why are we now positive?

Multiple factors must be taken into account. Starting with the CEO’s words, he said: “The industry-wide disposal of vial inventory has been more pronounced than previously expected, especially in the most heavily backlogged EZ Packaging vials.” There is a gradual recovery expected, with orders building momentum in 2024. In addition, he emphasized how Stefanato was affected by the postponement of a large customer order, causing a more cautious approach to 2024 sales. Stefanato is counting on favorable secular tailwinds with a growing presence in demand for Biological materials. Second-quarter growth is likely to continue to be affected by headwinds. As a result, we here at the Lab are now assuming mid to high single digit growth for the Business Development Services (BDS) sector. Looking at margins and looking at the emptying of EZ-fill bottles, the company will reduce its gross margin mix, and overall, its earnings before interest, taxes, depreciation, and amortization (EBITDA) will be negatively impacted. In the engineering department, longer lead times for electronic components appear to have been resolved; However, margin risks exist. Looking back, the guidance was flat, and now, we assume a moderate decline in sales in the division. We also believe there will be higher start-up costs for new facilities and higher distribution and purchasing costs due to the company’s capital expenditure plan. Regardless of the CEO’s reassuring words and current negative statements, the company is likely to enjoy:

- Higher margin thanks to the High Value Solutions (HVS) division,

- Better EBITDA mix thanks to lower customer offloading activities,

- Better product mix with capacity expansions underway at Fisher and Latina, which is likely to support sales in the long-term trajectory.

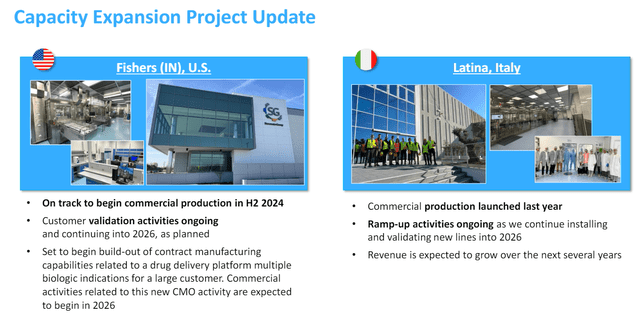

In detail, capacity increase activities continue as Stefanato continues to validate the new lines. Regarding the Italian addition, production of commercial syringes began last quarter. These lines serve as a transition for one customer to sterile cartridges from bulk. Regarding the Indiana facility, the company is well positioned to begin commercial production in the second half of 2024. Capacity will support demand related to biologics and GLP-1. There was no news about Chinese expansion. However, this may be contract manufacturing capabilities for a large customer in 2026.

In addition, Stefanato comes from a capital increase that injected around 170 million euros into the company’s shares, reducing debt that fell to 186.9 million euros from 324 million euros at the end of December.

Expanding Stefanato’s capacity

fig. 3

Earnings and Valuation Changes

Following the first quarter results and Stefanato’s guidance changes, we have updated our EBITDA estimates for 2024 and 2025 to €275 and €310 million, respectively. The single-digit growth rate is impacting the company, and we have reduced our 2024 sales by EUR 1.12 billion, which is in line with Stefanato’s new forecast. Considering the capital injection, we reduced our interest payments to €8 million per year, and with no change in the technical guidance on corporate tax, we reached a net income of €135 million and earnings per share of €0.49 per share.

In terms of valuation, our 12-month price target estimates are derived by applying an EV/EBITDA multiple to the base case TTM EBITDA. Applying a 24x EV/EBITDA multiple, in line with Stevanato’s peers, we lower our price target to $23.75 per share, using expected debt and cash levels. Relative to Stefanato’s peers, the company no longer trades at a premium. We used the average EV/EBITDA valuation of Schott Pharma AG, Gerresheimer AG and West Pharmaceutical Services Inc. On the balance sheet side, considering the equity infusion and the capital expenditure plan, our net debt is €207 million at the end of the year.

Risks

Downside risks to Stefanato’s price target include 1) slowing demand for biologics, 2) increased competition from Chinese players, 3) asset substitution risks, 4) poor execution of significant new capital investments that could impact revenue performance, 5) multiple downstream valuations, 6 ) Regulatory changes and 7) US-China relations regarding drug supply agreements. In addition, the Company is exposed to foreign exchange risk.

Conclusion

Last time, we reported on How Inventory Disposal Activities Should Be Muted Across Space . Although the company’s financial target for 2027 was confirmed, we were more cautious. After the first quarter results and with this reset, we see tailwinds ahead. For this reason, we now recommend Stevanato with a Buy rating and a price target of $23.75 per share.