Jeremy Poland

Subsea 7 (OTCPK:ACGYF)(OTCPK:SUBCY) is an engineering, procurement and construction (“EPC”) company that builds oil production structures at key locations around the world. They are one of two elite players working in the biggest fields. Our latest coverage focused on… On debt, which made us insecure about the company, as its business is cyclical. However, clearing the backlog from a better pricing environment is boosting EBITDA at the moment and the company is also taking some other constructive steps like increasing outsourcing to reduce capital intensity. EBITDA multiples remain low, but net income is taking a hit due to higher financing costs. The backlog will be cleared, and strong EBITDA growth will be ensured over the next two years, based on typical project cycles. These are not very cash productive, so the debt will be here to stay for a while then They want to continue to grow their business, too.

Dividend distribution

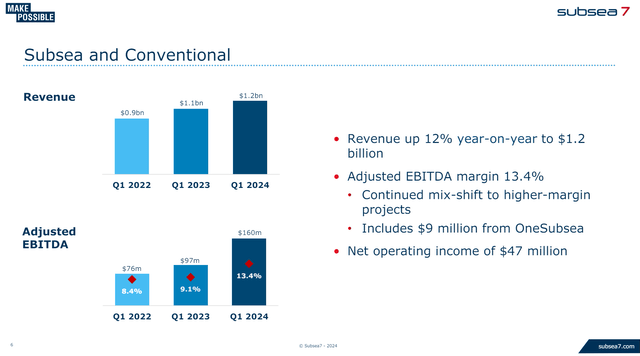

The main effect is that new projects are indexed to higher margins after the initial bout of inflation, where previously inflation indexing was not widely used. The EPC operation in key developments such as Yggdrasil is an example of this, as well as some operations in Brazil, which are lower margin activities but benefit from having better pricing environments after the Ukraine war. These large contracts in Norway and Brazil are described as “very large”, and the general expansion of other contracts reflects the increasing scale of projects and the commitment of exploration and production companies. At the same time, other projects in the pipeline are starting to shift to later, higher-margin stages of their life cycle, a dynamic we’ve focused on in our previous coverage. Backlog development is very good, with a flat backlog year-on-year despite strong delivery and revenue growth from the traditional segment.

Undersea part (View Q1)

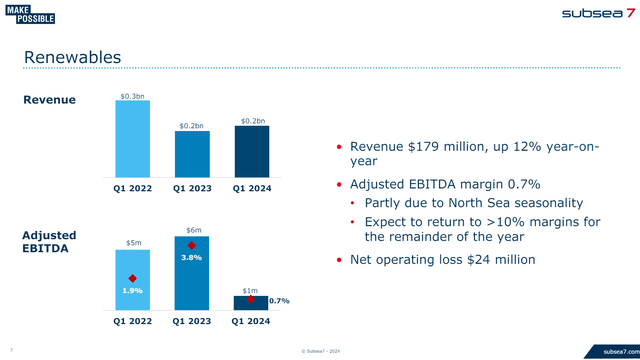

Seaway remains a marginal sector, unable to deliver exceptional margin growth, but revenues are at least rising. This is partly a lack of operational experience, but also due to some seasonal effects from maintenance and lower margin resulting from activities already undertaken in the quarter. The backlog continues to develop well for the renewables business, as you would expect from a major renewables push.

Renewable energy sector (View Q1)

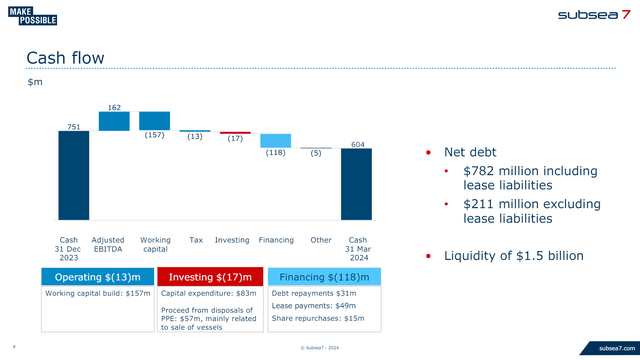

There are two capital allocation points we would like to highlight. In our last article we highlighted debt. It is a big responsibility and depends on income and cash. If the activity stops, Subsea will have a big problem. However, we would like the company to use recycling as an opportunity to address this. They have completed some vessel dispositions equivalent to about 10% of net debt, and are instead leasing vessels to handle less commoditized business. Overall, their approach of outsourcing some work to other ships also reduces the firm’s fixed capital intensity. Working capital intensity remains high due to the significant contract and economics inherent in EPC. However, net financing costs continue to rise.

Group orientation (View Q1)

However, going from having 28 owned vessels to 12 charter vessels is a great start, and the more they can reduce the capital base, taking into account the economics of the industry, the better. It will exit the margin, but high levels of strategic activity and the conditions needed to justify rich pricing given expensive raw materials and inflation help offset that.

Likewise, the company is trying to achieve scale in existing geographies to be able to keep fleet utilization high by avoiding transit. Hence, their focus is on building a big book in Brazil, which is going well so far, and as a seller, Subsea 7 is not exposed to political considerations around Petrobras (PBR). With pipeline construction in Australia, Brazil, and more distant geographies, utilization should continue to rise and this will boost margins as existing projects also continue to expand into later stages, and begin to filter out higher margin projects deeper in the backlog.

minimum

Ultimately, the combination of divesting the backlog created in a better pricing environment, and higher-margin later-stage projects, does a lot to support the company’s EBITDA growth.

Financial flow (View Q1)

But growth is capitally expensive for Subsea 7 and the debt will be there, costing a lot in terms of interest rates as long as there is increased demand to develop oil assets. Without this order, things would be worse for Subsea 7.

We like the company, but we still see risks in this business that is generally cyclical and has below-average economics. Combined with the high cost environment, we are still uncompetitive even with future EV/EBITDA multiples of less than 6x. At least it’s cheaper than its peers at 8.5x EV/EBITDA.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.