By Martin Nanskivel

thesis

Black Swan events are rare, and usually describe highly unusual excesses that lead to significant market disruptions:

The black swan theory or black swan events theory is a metaphor Describes an event that comes as a surprise, has a major impact, and is often inappropriately rationalized after the fact with the benefit of hindsight. This term is based on a Latin expression that posits the absence of black swans. This expression was used until about 1697 when Dutch sailors saw them in Australia. Subsequently, the term was reinterpreted to mean an unexpected and consequential event.

Amplify Black Swan Growth and Treasury Core Fund (NYSEARCA: SWAN) is an exchange-traded fund from Amplify that aims to hedge investors’ returns in cases of sudden and unexpected market disruptions. We’ve got you covered This name is from before, nearly two years ago, when we highlighted why the fund’s duration component would be a negative driver of total return in a rising interest rate environment.

With interest rates peaking, questions in the market revolve around the timing of the first rate cut, rather than whether the next step will be a hike or a cut. In this macro context, we will reconsider SWAN and ascertain whether it is a good fund to own given the massive run in stocks in the past year.

Fund Composition – Long S&P 500 and Treasuries

The fund has a very straightforward structure – it contains long-term S&P 500 options and a ladder of Treasuries. S&P 500 options are:

Leap options (Fund website)

Don’t be intimidated by the nomenclature here, “LEAP” simply stands for Long Term Expected Equity Securities, and refers to options that have maturity dates longer than one year. The fund uses this type of option in order to gain long-term exposure to a stock index without the full impact on the balance sheet of owning the entire index.

The second holding in the ETF is represented by a ladder of Treasuries:

Bond Holding (Fund website)

The portfolio contains Treasury bonds with average maturities of 5, 6 and 7 years. Given its holdings, it’s not surprising that the fund has a 30-day stock yield of 3.18%.

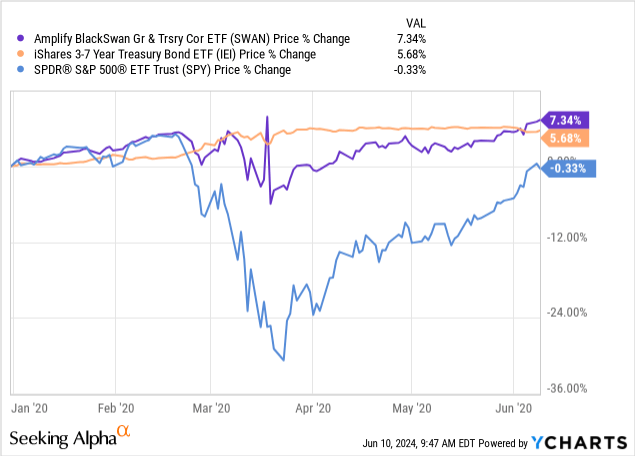

In a normal economic environment, bonds provide a hedge to stocks through their negative correlation. In the event of a crisis or unexpected event, stocks lose their value while bonds are offered as a safety valve. We saw this during the Covid crisis, when stocks saw a huge decline while bonds got a very strong showing:

While the S&P 500 saw a decline close to -30%, SWAN had a very modest -5% decline, with performance tempered by bond bids. We can see how the iShares 3-7 Year Treasure Bond ETF (IEI) got a big exposure as Covid developed.

The chart above is a perfect picture of what SWAN actually does – when external events occur, the ETF protects investors from very large drawdowns with its bond wrapper. External shocks to the economy are always dealt with through monetary and fiscal stimulus. Thus, the economy gets lower interest rates and investors get higher bond prices.

Drivers return

The fund’s primary return drivers are average rates and stock returns as included in the S&P 500. If the return component of the S&P 500 is fairly straightforward, the bond segment has dragged down the fund’s returns in past years.

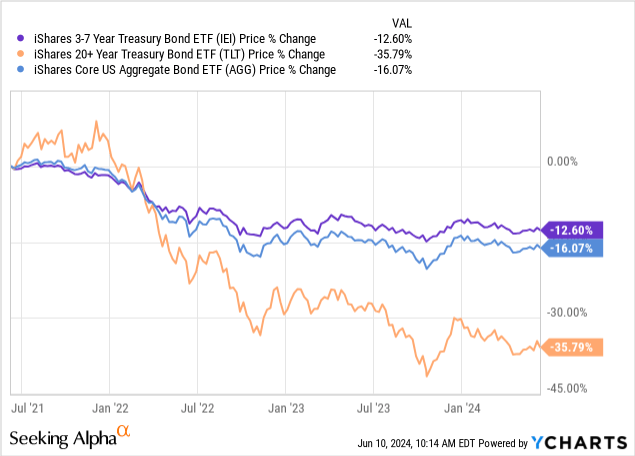

What we have witnessed in the past two years has been an unprecedented bear market in bonds. As the Fed aggressively raises interest rates, bonds of all kinds suffer incredible losses:

Long-term Treasuries suffered the highest losses, with medium-term funds down “only” -12% to -16%. When we come out of peak rates, we will see the opposite happen. When prices fall, the likes of IEI, AGG and TLT will benefit greatly.

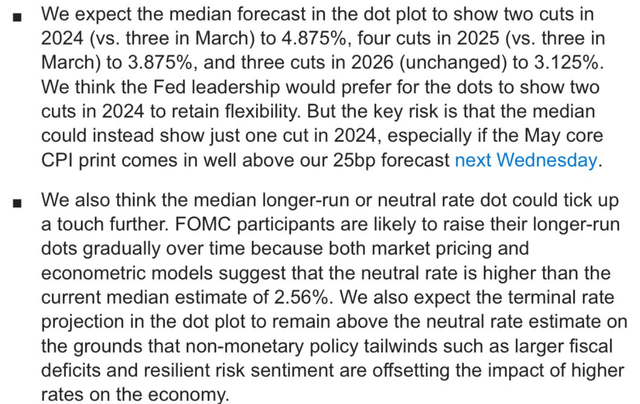

In the external case of a black swan event, we will see another strong showing for Treasuries. Think of a major global conflict or other unexpected event. While we do not rule out black swans, our base case calls for a moderate recession that would lead to the Fed cutting interest rates. Goldman calls for two cuts in 2024 and four cuts in 2025:

Fed cuts GS (Goldman)

First, it should be noted the higher neutral rate that Goldman Sachs is assuming going forward, but more importantly the reader should focus on the number of cuts expected for the next 12 months. Interest rate cuts equal higher bond prices, which is beneficial for SWAN even if no external event occurs. The trend this year has been to postpone interest rate cuts by the Fed, so in our view we will only get a cut at the end of the year.

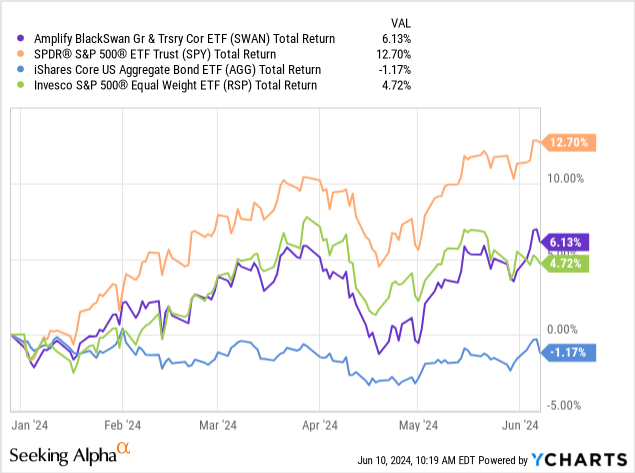

Performance was strong in 2024

While the iShares Core US Aggregate Bond ETF (AGG) has posted negative performance in 2024, SWAN is up significantly:

It is interesting to note that on a total return basis, SWAN is higher than the Invesco S&P 500 Equal Weight ETF (RSP). SWAN posted a total return of 6.13% this year, versus just 4.72% for RSP. We expect this trend to continue, with large caps benefiting from the rise, while the middle part of the yield curve does not drag yields lower, all while providing a built-in hedge.

Conclusion

SWAN is an exchange-traded fund. The vehicle has S&P 500 LEAP options and an intermediate duration bond cover. The fund performed admirably during the Covid black swan event, but was impacted by a spike in interest rates starting in 2022. With peak rates behind us, the fund is once again an attractive option for investors interested in external black swan events. In a normal economic environment, the fund would perform well, and testimony is its 6.13% performance in 2024, outperforming the equal-weight RSP Full Equity Fund. As the Fed lowers interest rates, SWAN’s bond wrap will yield positive results, while LEAP options will follow the broader stock market. We like SWAN’s makeup of today’s macro environment and are a ‘buy’ of the name at current levels.