Editorial by Alexander Farnsworth/iStock via Getty Images

Dear readers/followers,

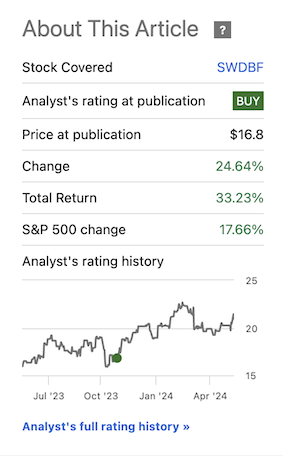

Swedbank ( OTCPK:SWDBY ) has been a very profitable investment for me recently. Since I wrote my last article about the company in November of last year, around that time When the bank “bottomed” the company saw a significant market-beating rate of return. You can see this here, You can find my latest article about the bank here.

Search for Alpha Swedbank RoR (Search for Alpha Swedbank RoR)

My thesis at the time was based on a very strong type of outperformance due to low valuation and a very attractive upcoming yield, derived from interest rate tailwinds. This has been achieved – and not just for Swedbank. I’ve also updated my thesis for other Scandinavian banks, such as Handelsbanken (OTCPK:SVNLF) and Nordea (NRBAY). Swedbank has never been, for In the last few years, it has been basically as good as those two years, but it still represents an attractive opportunity in the medium term.

That’s why I own shares in all three banks at the moment. I have clear goals for selling these shares, which is why I use covered calls over the very long term (1-2 years) to boost the return by 2-3% and possibly sell my shares. The current strike prices for my Swedbank calls are over SEK 240 per original share, and I bought shares for less than SEK 175 per share.

Buying Swedish banks in this way is a very effective way to achieve a very strong return and good upside.

Let’s take a look at the upside and results after the first quarter, going into the second quarter and the rest of the year – and look at what we can expect over the next year or two.

Swedbank – I expect long-term upside, but I would sell at a higher price of SEK 250-260 per share.

It should come as no surprise to anyone that Swedbank has achieved very strong rates of return. The high interest rates we are currently seeing mean that the company has finally seen some impressive ROE, with the KPI well above the target, at 18.3% for 2023, and a similar level expected for this year.

High income also means that cost-to-income ratios have decreased significantly since the end of last year from already low levels of 40% to 33% during 2023.

While credit impairment ratios are not quite at record low levels, at 0.09%, they are still incredibly low and on par with leading banks like Handelsbanken.

The company’s dividend policy was reduced a few years ago and now represents 50% of profits, meaning that for 2023, it paid out more than 15 SEK per share, and the bank is likely to offer a similar dividend for fiscal 2024, given that interest rate cuts. And its decline is slower than one would normally expect.

As of Q1 2024, the company still has more than 80% of its loan book in Sweden – and unlike Handelsbanken and Nordea, it has no operations in other Scandinavian countries. Instead, the company has loans in the Baltics of around 14%, and currently has more than 7 million private clients and more than 550,000 corporate clients. Its gross credit impairment ratio is less than 0.05%, its liquidity is over 180% Liquidity Coverage Ratio (LCR), and it has one of the most comprehensive digital offerings in the market.

Swedbank IR (Swedbank IR)

Swedbank is also a very cheap and efficient bank. It’s not my personal bank – I, as a customer, am willing to pay a little more for a different, more personalized kind of service, which I get from my current bank, which is not publicly listed. However, I maintain an account with Swedbank and use their services.

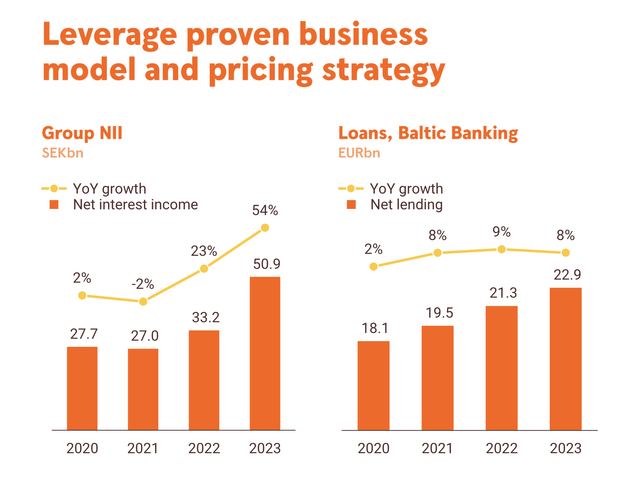

The reversal in interest rates led to the company’s National Insurance doubling its value within a few years, and its loan book, especially in the Baltics, grew by near double-digit increments.

Swedbank IR (Swedbank IR)

The company now has a market share of over 25% in Lithuania, and over 20% in Latvia, and is striving to grow its private banking business further as well.

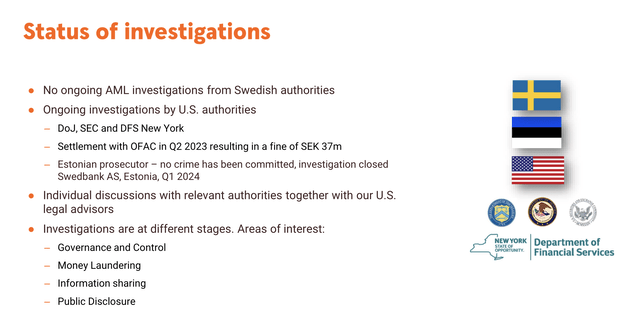

When I started writing about Swedbank on Seeking Alpha in 2019, there was a lot of talk about anti-money laundering and investigations into banking practices, even from US authorities. It expected at the time that these penalties would fall with some fines, but would not have a significant operational impact on the bank. What is the net and final result of these investigations?

Swedbank IR (Swedbank IR)

There are a few still going on with some potential fines, but nothing major – as some analysts have been pointing to the supposed possibility of Swedbank not being allowed to deal in US dollars anymore. I haven’t seen this mentioned in several years. Fines and this type of operation are part of doing business for these banks, and should not be overestimated (nor underestimated either, of course).

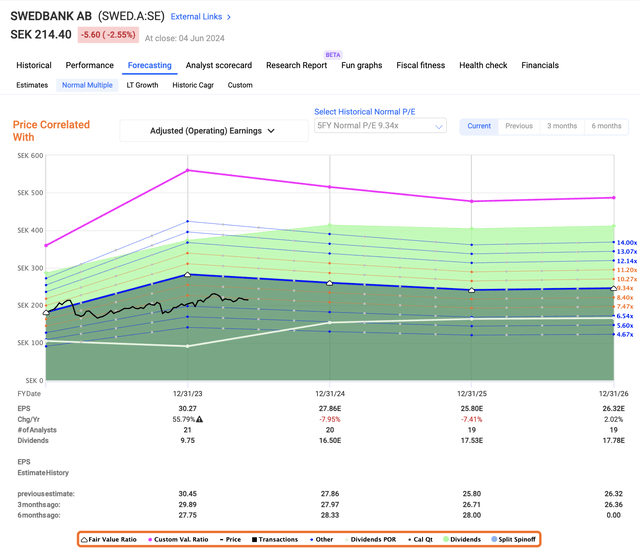

The first quarter saw ROE rise to approximately 17%, impairment ratio by 3 basis points, CET-1 by 19.3% with buffer margin of 420 basis points, and quarterly earnings per share of SEK 7.47 which amounts to Run south of 30 SEK. Based on the company’s dividend policy, this puts the 2024 dividend as of this time at around SEK 14.8 per share, resulting in a current yield at SEK 215, just under 7%. This is a very good return for the bank, but since 2023 has been such a weird year, valuation will become important as we value the bank here. Trading at normal multiples, it may appear that Swedbank is trading at less than 8x P/E, but that is not really the case once you remove 2022-2023 and the decline we are likely to see once interest rates normalize in the next few years.

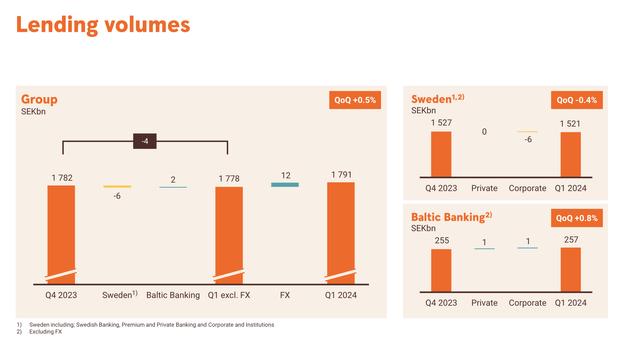

Lending volumes and other fundamental trends do not look worrisome, at least for now.

Swedbank IR (Swedbank IR)

Even deposit sizes are growing or at least not decreasing. But we’re starting to see a little bit lower results in net interest income, which declined during the first quarter by 5.5% due to lower margin and foreign exchange. Net commission income increased by about the same amount (but by a smaller amount). The company took a strong hit on the other income side, down 24.5% due to some revaluations in the Baltics, but at the same time the core income of this sector improved.

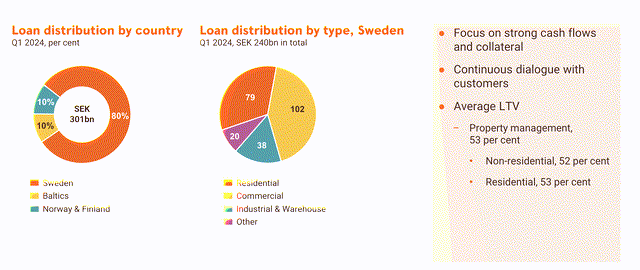

Importantly, asset quality remains strong and the bank’s exposures are conservative. The company’s property management exposures in the 20 largest volumes have been stress-tested, and even at an interest rate charge of 7% of 12-month debt, these 20 largest volumes have an interest coverage ratio, or ICR, of 2x – down from 2.2x based on Annually, but still at a comfortable level. Below is the distribution of the bank’s current loans in the field of property management, which represent 16% of the company’s total loans.

Swedbank IR (Swedbank IR)

As you can see, there is some exposure here in CRE – but the overall LTV is stable, averaging 53%. Loans above 75% are less than 0.5% of the total, and constitute less than SEK 350 million – so although such loans do exist, they are extremely rare, and non-performing loans are low here, with almost none in stage 3.

So the company remains more conservative than critics might imagine, and in fact Handelsbanken has a larger real estate exposure than Swedbank.

When it comes to housing and mortgages, there are also reasons why I shouldn’t worry here. The Swedish market and the Swedish model have full recourse, which means that debt relief is almost zero. There is no conversion into securities, no sub-prime market at all, and no third-party origination practices per se.

Recent years have also brought a very restricted buy-to-let market, meaning there is limited speculation in the existing homeowners’ market, with 65% home ownership in Sweden, and Organize The rental market, even for rent to rent. The bank’s underwriting standards are also very strict, with legal requirements for loan amortization based on LTV and DTI rates – and for apartments or owner-tenant rights, the financial statements of the tenant-owner association are looked at very carefully.

96% of Swedbank’s loan portfolio is below 70% LTV at the moment for private mortgages, which is not the most conservative on the market, but very good, and the percentage of loans past due on a 60 day basis was less than 0.13%. There is a rise in this, but this rise has been almost from zero, and the credit impairment ratio is still very low, with accumulated amounts of SEK 2 billion – but this For the years 1982-2024.

So, overall, very conservative — and the company’s financials and results look good.

Let’s take a look at the positive side of the company and its valuation here.

Swedbank – There is a lot to like, although the rating may be a bit overrated

To call Swedbank overvalued here would be wrong. Also, the last time I covered the business, I gave the bank SEK 185, a goal I’ll meet in a bit here. However, I will be To the fullest extent Swedbank’s accurate forecast for any kind of premium here, though, is over 1.33T at TEV, and an A+ credit rating from S&P Global.

The company is priced for 55% EPS growth for 2023, while 2024 is likely to see a high single-digit decline, and 2025E is likely to bring another decline. This, from my point of view, Completely normal Given interest rate trends here, and where things are likely to go over the next few years.

Swedbank’s valuation is upside down (Swedbank’s valuation rises)

Because I consider it likely that these declines will materialize, I would be cautious in buying Swedbank at any price above SEK 190-195 because when things return to normal at the 8-10 P/E level, which is where Swedbank usually trades, the current It implies an increase in price. Up less than 12% annually, this includes a 7% dividend, which means it’s less than a 5% capital appreciation – which is what makes this company overvalued to me.

Not much, granted. But given how volatile Swedbank can be, it wouldn’t be wrong to say here that at over 210 SEK, the bank is priced for a bit of perfection that may not be achieved.

If you want a solid 7%+ return, that’s an option – but I see better options for such a return and such use, and ultimately, I’m looking for 15% per annum or better – and that’s on a conservative basis, not impulsive or bullish.

I am therefore raising Swedbank’s PT amount to SEK 195, but under no circumstances would I pay more than that under current estimates because that means the 15% annual rise is unlikely to be achieved.

This brings me to the following updated thesis for Swedbank as of June 2024.

thesis

- Swedbank isn’t significantly overvalued here, but it’s not cheap either and lacks compelling upside. I think operating results will deteriorate slightly over the next few years as the market deteriorates.

- Given this potential pressure but also some potential upside, I rate Swedbank conservatively and will hold the company at this valuation – but only to the extent that other alternatives are attractive at this time.

- I consider it time to raise my PT on Swedbank given what we are seeing here and what may happen next year.

- I give Swedbank a target of SEK185 here, which is higher than my previous target, and lower than the bank’s current share price. This means that Swedbank is a ‘Buy’, and I am updating my rating of the bank here.

Remember, all I care about is:

1. Buy undervalued companies – even if that discount is minor, not stunningly massive – at a discount, allowing them to normalize over time and reap capital gains and dividends in the meantime.

2. If the company goes beyond normalization and goes into overvaluation, I take the gains and roll my position into other undervalued stocks, repeating #1.

3. If the company is not overvalued, but hovers within fair value, or reverts to undervaluation, I would buy more as time allows.

4. I reinvest proceeds from dividends, business savings, or other cash flows as defined in #1.

Below are my criteria and how the company meets them (in italics).

- This company is all about quality.

- This company is fundamentally safe/conservative and well managed.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversals.

I will say that the company has upside, but I will also say that the upside is not as significant as some of the other companies out there. However, it is a risk that I consider worth taking with the right expectations, which is why even though I wouldn’t rate the company as cheap, I consider it a ‘buy’ here.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.