FelixMizuzhnikov

So far in 2024, Sweetgreen (New York Stock Exchange: Saint-Germain) It has turned out to be an excellent investment as the company is up more than 160% since the beginning of the year.

I first reviewed Sweetgreen in December of last year and gave it a “Hold” rating. since then, The stock has definitely exceeded my expectations.

Let’s dive into the financials as well and the company’s recent changes to see if this company can continue to deliver market-beating returns.

Company updates

In the most recent quarter, Sweetgreen opened six new restaurants. It looks like the new restaurants are off to a great start as company CEO Jonathan Neiman said in the first quarter earnings call, “The portfolio of new restaurants we opened in the first quarter of 2024 has average weekly revenues, which already exceed the average of the existing fleet. Building on the momentum created by the opening of Totem Lake, which quickly became one One of our best-performing restaurants, the South Lake Union location in Seattle, had one of the strongest opening weeks in the company’s recent history“.

I think this clearly shows that there is demand for Sweetgreen’s offerings and that the company has plenty of room to continue expanding. Neiman stated this on the call, saying:Openings like this prove that our brand has a much greater reach than our current physical footprint, and that there is huge white space for our category definition concept.

Sweetgreen is poised to open between 23-27 new restaurants in 2024. Additionally, the company plans to open 7 new Infinite Kitchen restaurants and upgrade 3-4 existing locations. Management noted that the company continues to see benefits from its Infinite Kitchens. These advantages include faster productivity, consistency of parts, and lower employee turnover.

Neiman also mentioned the new menu offerings on the earnings call. Sweetgreen has launched several new steak-related items, including a new caramelized garlic steak. Nieman said that since the testing phase in Boston, the caramelized garlic steak has already become popular with customers.

The management also mentioned making investments to promote a better environment for employees. Nieman specifically mentioned giving bonuses to “head coaches” and creating tipping opportunities for team members.

In my first article, I criticized Sweetgreen’s culture as the company’s Glassdoor reviews were not great nor were employees’ views of Neman. I realize this is a fast food (or casual) restaurant but compared to many of its peers, Sweetgreen was still seen as an undesirable place to work compared to many other restaurants.

For example, CAVA Group (CAVA) has better reviews (as I noted in a previous article) and generally seems to do a better job of engaging their current employees and future leaders through their Academy GM network.

For Sweetgreen, it was good to see that employee turnover in Q1 2024 was lower compared to Q1 2023, and the company appears to be promoting more internally as more than 50% of Sweetgreen’s “Master Trainers” are From internal appointees. Neiman noted that he would like to see this percentage continue to grow.

Finance

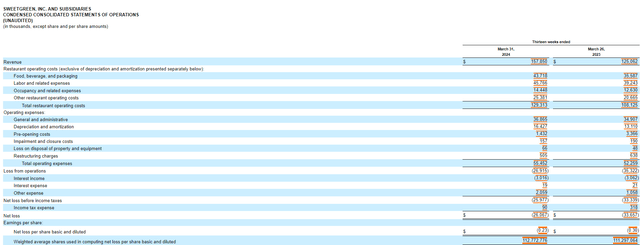

In the first quarter of 2024, Sweetgreen generated revenue of approximately $157 million, which represents an increase of approximately 26% compared to the first quarter of 2023. Despite still posting a net loss in the quarter, Sweetgreen is closer to profitability compared to In the first quarter of 2023, as you can see from its income. Statement below:

SEC.gov

Management indicated same-store sales in the quarter grew 5% compared to the previous year, and restaurant-level profit margin was 18.1% compared to 13.5% in the first quarter of 2023. The company updated its forecast for 2024 and now expects same-store sales to be close Who is this. 5% range Management expects the profit margin at the restaurant level to range between 18-20%.

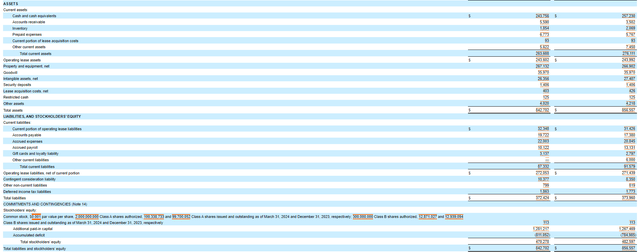

Sweetgreen still has a healthy balance sheet, as you can see below:

SEC.gov

The company’s cash balance has decreased slightly since December 31, 2023, but Sweetgreen’s current asset balance can still cover all of the organization’s current liabilities.

evaluation

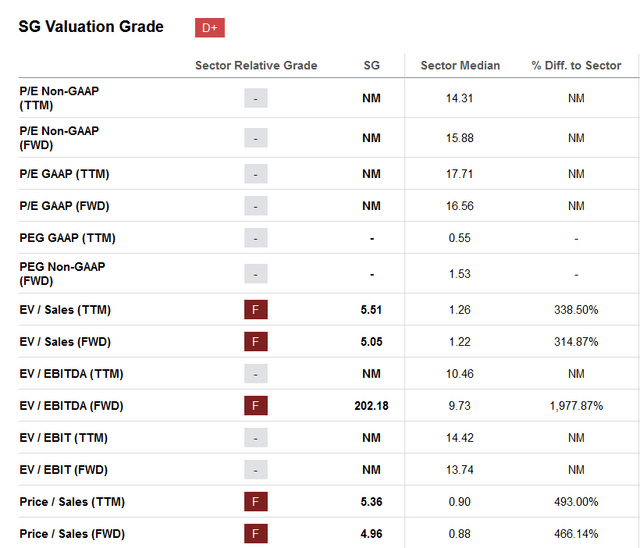

As you can see from the rating metrics below from Seeking Alpha, Sweetgreen’s overall value score is “D+.”

Seeking alpha

Since Sweetgreen is unprofitable, I think price versus sales is the best measure to view this enterprise.

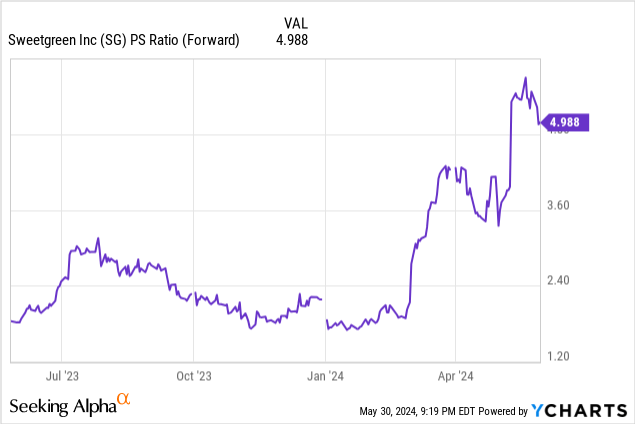

Sweetgreen appears to have a high price-to-sales ratio compared to its peers in the sector, and the company’s current (future) price-to-sales ratio is much higher compared to what this ratio was at the beginning of the year.

I agree with Seeking Alpha’s assessment that this stock is likely overvalued. Sweetgreen stock has risen significantly this year, and I recommend investors wait until the stock falls back to January levels before considering adding shares.

Risks

Aside from the risks I mentioned in my previous article, there is a new risk I would like to mention which is consumer sentiment. As many news articles have reported, many consumers are feeling rising inflation. Recent earnings from McDonald’s (MCD) and Starbucks (SBUX) illustrate the point that many customers feel that food (and drink) prices at restaurants are too high. (Although I think Starbucks has some operational issues as well).

New restaurant chains like Sweetgreen and CAVA appear to be unaffected so far in 2024. These chains may be offering great deals given the price. I know I would rather spend $15 or $20 on a healthy, nutritious meal than a fast food burger if the price was the same. These could also be the trendy restaurants of the time. If inflation holds, it will be interesting to see if Sweetgreen has similar issues compared to these more established restaurants.

Conclusion

This has been an impressive quarter for Sweetgreen. The rise in revenue and same-store sales growth is bringing the company closer to profitability.

For long-term investors, it’s good to see the company’s new restaurants are doing well and there appears to be plenty of room for the company to continue to grow. Additionally, I believe Infinite Kitchens will likely continue to provide several benefits to the company, ultimately increasing restaurant level margin for those stores.

However, I cannot justify the company’s valuation given the significant increase in the company’s stock price so far this year. With the stock price up over 160% since the beginning of the year, I would be inclined to wait for the market to pull back.