Yaghi Studio

introduction

I had a thesis on Tesla company (Nasdaq: Tesla) with a “Strong Buy” recommendation, was shared in early March. The stock price is down 2.5% since my previous post about the stock, compared to +4% from the S&P 500 (SP500).). The environment remains challenging for auto companies due to high interest rates. The overall headwinds in the company reversed first quarter report, As auto margins deteriorate and sales stagnate.

However, the broader economy and interest rates are cyclical, meaning the challenges Tesla faces are temporary. On the other hand, Tesla continues to pursue its long-term goals and the company strives to maximize its potential to capture favorable secular trends. The valuation remains very attractive, and I’m inclined to echo a “Strong Buy” rating for TSLA.

Fundamental analysis

And I think that Headlines regarding intensifying competition are one of the biggest reasons why Tesla stock is having a difficult 2024 with a 29% decline since the beginning of the year. As a fundamentals-only investor, I want to start by sharing my insight into “increasing competition.”

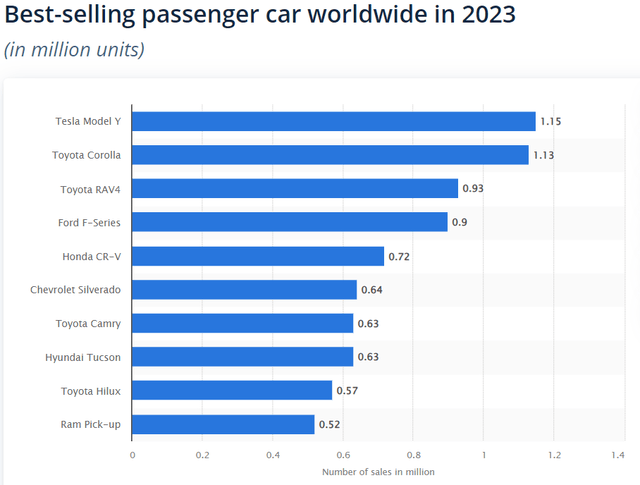

Competition in the broader electric vehicle (EV) industry may already be heating up, but Tesla appears to be on another level. The Model Y became the world’s best-selling vehicle in 2023, beating long-term leaders Toyota(TM), Corolla and RAV4. This achievement is special because the Toyota Corolla and Toyota RAV4 are both internal combustion engine models (“ ICE”), which means that despite all the controversy, EVs could be more attractive than ICE cars. My point that Tesla is on another level among EVs is underscored by the fact that no other EV model is in the top 10 best-selling chart for 2023. What’s the competition?

Statista

There’s another big reason why I think the phrase “intensifying competition” is overrated. While it was certain to me that the export potential of Chinese electric vehicle manufacturers was severely limited due to the Cold War between West and East, it was merely my prediction supported only by my judgment. However, in May, President Biden imposed a 100% tariff on Chinese-made electric vehicles. This means that Chinese OEMs are unlikely to enter the US market because it would be unrealistic to compete on prices with a 100% tax burden.

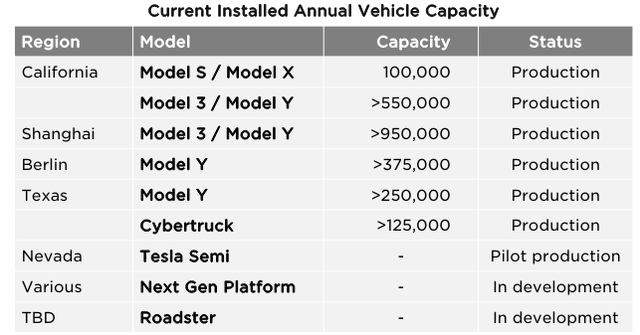

I think the possibility of the same move from Europe is also high. According to the source, there are about 2.4 million direct manufacturing jobs in the automotive industry throughout the European Union (“EU”). This represents about 8.3% of total employment in the EU manufacturing sector, which is a significant proportion. It is therefore very likely that the European Union will seek to exploit opportunities to protect its auto industry from Chinese exports as well. Tesla, on the other hand, seems protected from these potential regulatory changes as it already has huge production in Europe, at the Berlin Gigafactory. Its current capacity is modest compared to the Shanghai factory, but Tesla has near-term plans to expand capacity to 1 million electric vehicles per year.

First quarter earnings presentation

It is also important that Tesla prepares to improve its competitive position further. The lack of a low-cost model seems to be the only weak point in the company’s model line. However, there is light at the end of the tunnel. According to Elon Musk, an affordable $25,000 model is on the horizon. The new entry-level model is expected to be introduced next year, which also makes me more optimistic. I think that when Tesla management announces a price of $25,000, this seems to indicate that the new model is planned to outperform the Toyota Corolla leadership positions. Currently, the Toyota Corolla starts at $23,145 in the United States

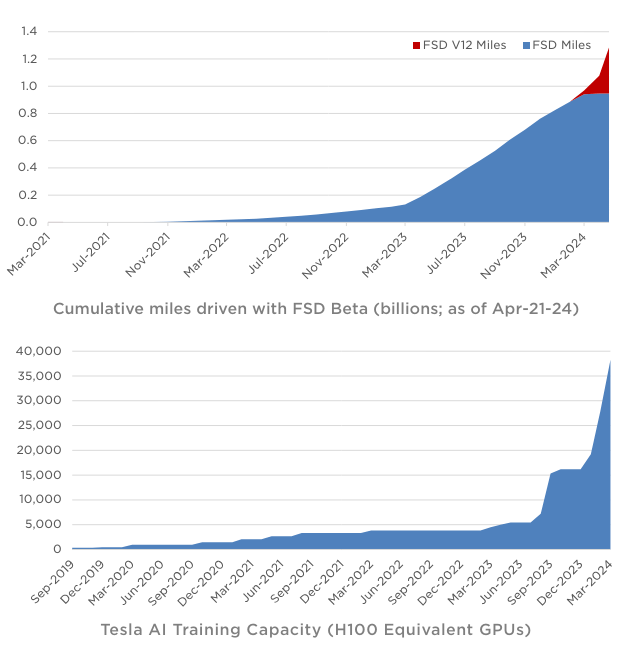

Furthermore, many people forget that Tesla is not just a car company. Aside from selling the “hardware”, the car itself, Tesla is also investing heavily, increasing its potential by leveraging its cutting-edge software. Much has been said about the enormous potential of Tesla’s Full Self-Driving (“FSD”) capabilities, and I won’t waste my readers’ time reading the same information. It seems that Tesla is still hungry enough to expand its AI endeavors beyond FSD.

First quarter earnings presentation

Recent news suggests that Elon Musk plans to build a “Gigafactory of computing” by fall 2025, powered by 100,000 Nvidia (NVDA) H100 GPUs. Last week, Elon Musk’s xAI company raised $6 billion to develop its Grok chatbot. While xAI is a separate entity that is unlikely to become a Tesla subsidiary, I believe that under joint control Tesla will be able to leverage the generative AI capabilities developed by Grok in the future. Microsoft (MSFT) with its early investment in OpenAI is a great example of how a hyperscaler can enjoy technology synergy with an innovative startup.

Q1 10-Q Report

As I said before, TSLA is not purely a car company. Its energy generation and storage businesses are showing strong growth, supported by its Megapack and Powerwall products. This sector continues to show revenue growth. More importantly, the overall profits of this business expanded significantly year over year, from about 11% to about 25%. However, the business is benefiting from increased volume and can expect further expansion in profitability. The industry is expected to see a CAGR of 16.3% by 2029, which is another strong tailwind for Tesla.

In short, I think secular trends suggest that bullishness on TSLA is reasonable. The company continues to invest in its strategic priorities, and headlines about intensifying competition seem to generate hype. There is strong non-automotive potential as well.

Evaluation analysis

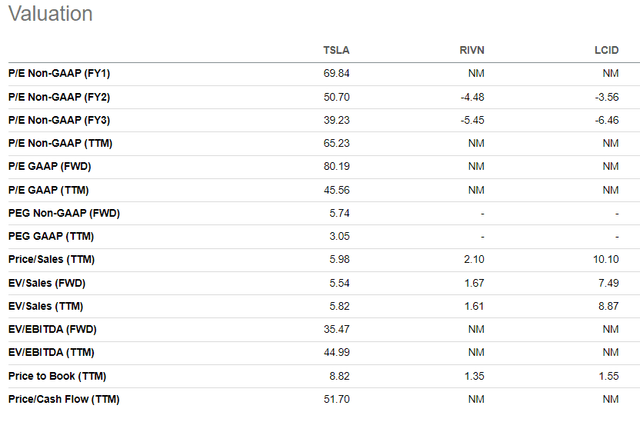

Conducting a peer pedigree analysis for Tesla is very difficult. BYD ( OTCPK:BYDDF ) is the only similarly sized electric vehicle company, but it is a Chinese manufacturer, and it is largely undervalued due to significant political and geopolitical risks.

Therefore, I will compare Tesla’s valuation ratios with US companies like Rivian Automotive (RIVN) and Lucid (LCID). These two companies are not yet sustainably profitable, and we can compare the three companies mostly based on revenue-related metrics.

Tesla is significantly more expensive compared to Rivian, based on price/sales and EV/sales ratios. However, compared to Lucid, Tesla’s valuation is very modest. However, looking at peer pedigree analysis does not give many answers.

Sa

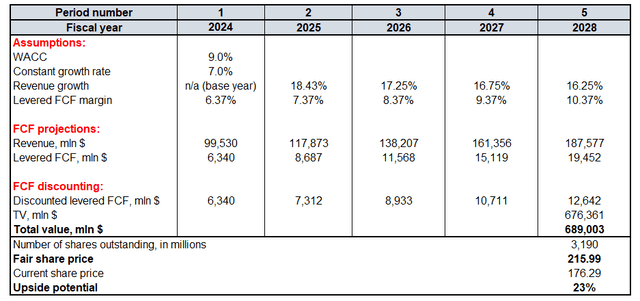

A discounted cash flow (“DCF”) approach would likely help with greater clarity. Future cash flows will be discounted using a weighted average cost of capital of 9%, a slightly more conservative level than the recommended level of 8.6%.

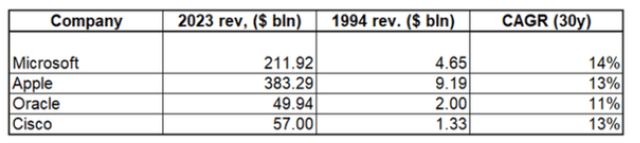

FY 2024-2026 revenues have been forecast by more than 30 Wall Street analysts, which I consider to be a representative sample. For years after 2026, I incorporate a slight 50 basis point deceleration in revenue growth annually. The constant growth rate is 7%, which some may disagree with. However, it is difficult to argue that Tesla is at the forefront of an emerging and young industry with strong growth potential. Something like Microsoft (MSFT), Apple (AAPL), Oracle (ORCL), or Cisco (CSCO) thirty years ago. So, let me show you the CAGR that these four companies have shown over the past three decades.

How much capital

They’ve all achieved double-digit revenue CAGRs over the past 30 years, which means that a steady 7% growth rate for calculating Tesla’s terminal value (“TV”) is fairly conservative.

The base year FCF margin is the average of Tesla’s last five years, with an expected annual expansion of 100 basis points. Conviction in the ability to improve FCF is high due to Tesla’s excellent profitability and strong long-term revenue growth potential. According to Seeking Alpha, there are about 3.2 billion TSLA shares outstanding.

Calculated by the author

The discounted cash flow model indicates a target price of $216, which represents 23% upside potential. I find this upside for a stock like TSLA to be a compelling opportunity.

Mitigating factors

Higher interest rates appear to be the main headwind for TSLA’s auto business, and since the US economy remains strong and unemployment rates are low, monetary policy may remain tight for a while. The uncertainty surrounding the Fed’s monetary policy is unfavorable for investor sentiment and could pose a drag on TSLA’s near-term rally.

Enhancing production capacity and investing in innovation requires huge amounts of money. Therefore, TSLA will need to invest huge amounts in research and development. This will likely undermine the company’s financial position and put pressure on the stock price if these projects are not completed on time.

Conclusion

This year’s decline provides a compelling buying opportunity for Tesla investors. The valuation is very attractive despite the rapid improvement in Tesla’s fundamentals. Therefore, I am aggressively adding more shares to my Tesla stake.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.