Evening pictures

Co-authored by Treading Softly

In the poem The road was not taken By Robert Frost, wrote:

Two roads diverged in the forest, and I took the less traveled path, and that made the difference.

I have I’ve always enjoyed this poem because it highlights the benefit of taking the road less traveled sometimes. This does not necessarily mean that people did not try this path, found it difficult, and went back and took the more popular or easier path. The ability to take the road less traveled and succeed can change everything for you. If you’re on Seeking Alpha, and reading the articles written here, you’re already on a very different path than most investors who use passive market ETFs – and for that, I applaud you. If you are an income or dividend investor, instead of trying to buy things at a discount price and sell it at a higher price to someone else, you’re already taking the road less traveled. You can take different paths on the road less traveled, leading to narrower and narrower paths with fewer people.

When it comes to market, many companies will try to take the road less traveled and discover that the niche route may not be a good one for them. They may not succeed, so they return to a more followed path, which, in their mind, has better potential for a successful outlook. When I worked in banking, very few banking institutions wanted to be the first innovator. They loved the innovation, but they didn’t want to be the ones paying money to research, test and see if it worked. Many banks were happy to adopt the successful initiatives of others. The last time I wrote about the BDC or business development company we’ll be reviewing today, I discussed how it has become a potential future leader in its sector.

Today, I want to examine its latest quarterly results to see if it’s still on track to become a future leader in the sector.

Let’s dive in!

Walking the road less traveled

The capital of the southwest (Nasdaq:CSWC), which yields 9.1%, is a BDC (business development company) that specializes in lower middle market companies that are at the small end of the spectrum of companies in which BDCs will invest. CSWC It focuses on companies with annual EBITDA between $3 million and $25 million. To help mitigate risk, CSWC places a significant emphasis on first lien secured debt. This underserved market niche can offer significant upside potential, as shown by CSWC’s older peer, Main Street Capital (MAIN). MAIN has proven that this market segment can outperform, even during the difficult times of the global financial crisis. CSWC is following the path paved by MAIN and doing a great job.

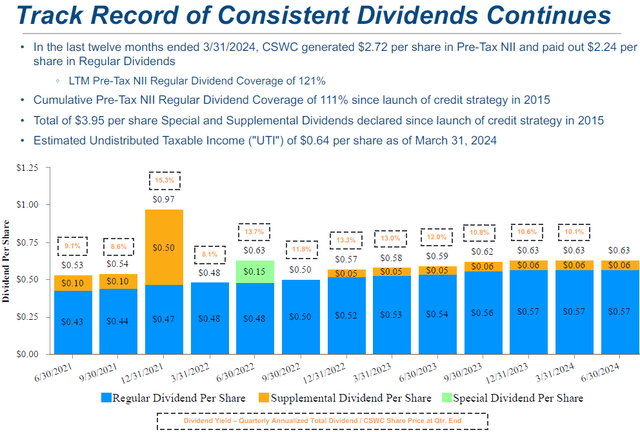

CSWC posted a strong quarter, prompting it to declare its dividend unchanged at $0.57 and pay another supplemental dividend of $0.06. This is in line with what CSWC paid last quarter. This can be easily covered by CSWC’s pre-tax NII of $0.68 for the quarter.

CSWC has done an excellent job in recent years of regularly increasing its profits, while pushing out supplements and special offers frequently. (source)

CSWC Q4 Presentation

Dividends are important because for startup companies, dividends tend to be the main source of an investor’s overall return in the long run. Since 2015, CSWC has paid a dividend of $16.16 per share. Over the next three quarters, CSWC will pay dividends greater than its 2015 net asset value.

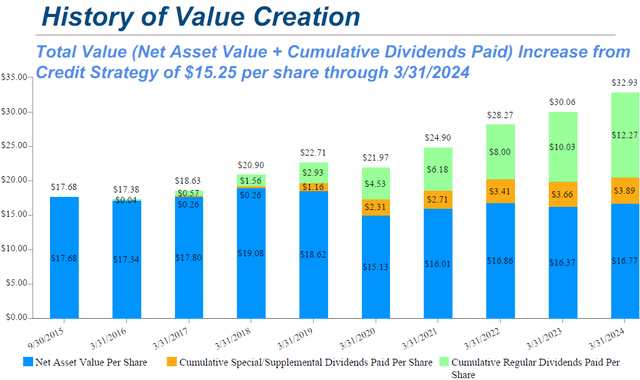

CSWC Q4 Presentation

CSWC’s NAV has been slowly trending upward. Although down from March 2019, it is worth noting that in December 2019, CSWC’s NAV was $16.74 as it paid a large special dividend due to a large asset sale.

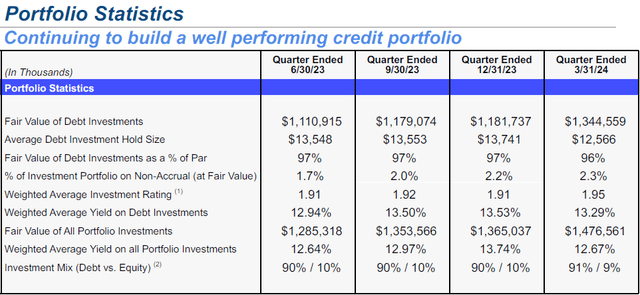

In terms of credit quality, CSWC continues to see nonaccrual as a small portion of its portfolio at around 2.3%.

CSWC Q4 Presentation

Given that BDCs lend using floating interest rates, it is very common for borrowers to begin showing signs of stress as interest rates remain high. It is “good” for the BDC since it is the BDC that receives the interest payments. However, if the borrower ends up filing for bankruptcy because they can’t afford the interest payments, this doesn’t help anyone. It’s good to see CSWC’s portfolio is holding up relatively well in this environment.

CSWC has benefited from BDCs’ excellent conditions, and the fact that their common shares trade at a significant premium to book value. Trading at a premium to book value is an advantage for a BDC because it can issue common stock at a high enough price that the capital can be invested in opportunities that produce earnings high enough to pay for the new shares, with some of the excess for the previous owners to see earnings per share and dividends rise.

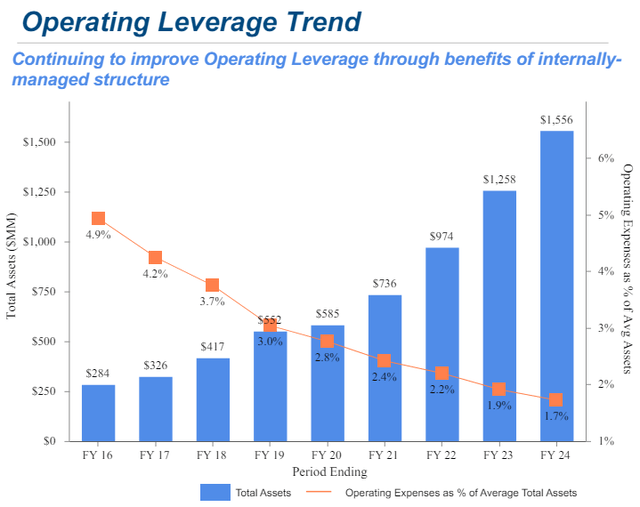

Additionally, this growth has allowed CSWC to reduce operating costs relative to the size of its portfolio.

CSWC Q4 Presentation

As this metric decreases, it becomes more difficult to find incremental improvement, so this benefit of CSWC growth will likely not play as important a role as it has in the past. However, CSWC’s low operating costs are a significant competitive advantage and positive for shareholders.

Looking to the future, we expect CSWC to continue to expand opportunistically. Earnings growth will not be as strong as we saw from 2021 to 2023, but we will continue to see supplements as long as interest rates are high, and we expect “normal” earnings to continue to grow at a slower pace.

CSWC is maturing into an established BDC. They tend to trade at a premium to book value, and they should continue to do so. For existing shareholders, this is quite a positive, as trading at a premium reduces risk and allows the company to create a “circle of virtue” where raising shares allows for growth that improves profits for everyone. This in turn reinforces market confidence that BDC should be trading at a premium.

Conclusion

CSWC has demonstrated its ability to quickly move into the premium tier of BDCs and is well positioned to eventually retain it in the same regard as other BDCs such as MAIN. When this situation is achieved, the early investors will be the biggest winners because they will be the ones who will achieve higher returns and will realize large unrealized gains. This is the biggest reason I want to invest in companies that others don’t know about. I’m willing to invest in companies that pay a high yield because they prove themselves incrementally. This way, when others demand to participate after they’ve been verified, I can exit if I feel the need to, or I can simply sit back and continue cashing in those sweet profits as they roll in.

When it comes to retirement, it’s a good idea to be paid. For decades, you have earned business income by pursuing the career you chose or the company you founded. Regular income flowing into your bank account that was supposed to extinguish the flames of your expenses. In retirement, you don’t have a full-time job anymore. You have to find a new source of income to fight that fire, lest it overwhelm your life and make your golden years the most miserable years of your life. That’s why I use my unique income method to invest in the market, to have an abundant stream of income flowing from the market into my account, extinguishing those fires and providing me with a buffer of additional capital. Financial freedom is found when you have excess wealth compared to your expenses. That’s the beauty of my income method. That’s the beauty of income investing.