Richard Drury

Written by James Knightley

First, a good month on inflation should become a trend

We continue to look forward to the Fed cutting interest rates from September on the basis that it believes monetary policy is constrained At 5.25-5.50% in an environment where they see the neutral interest rate as around 2.6%. They don’t want to cause a recession if they don’t have to, and if the data allows them to start making monetary policy a little less restrictive, we think they will seize that opportunity.

In order for them to feel comfortable taking this course of action, we think they need to see three things. First, core inflation must show evidence of decline. The first quarter numbers were very hot, but we did get a 0.2% month-on-month reading in the Fed’s preferred measure of inflation, the core personal consumption expenditures deflator for April. If we can get two or three More in quick succession, which would indicate a moderation in price pressures, would be a necessary but not sufficient outcome leading to a rate cut.

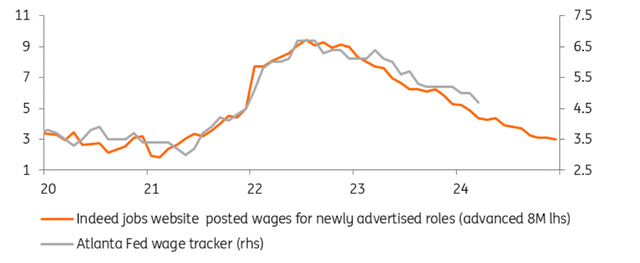

Second: More stagnation in the labor market and cold wages

Second, if we see evidence of labor market stagnation, the Fed will likely be more convinced that inflation pressures will continue to trend toward the target and stay there. The unemployment rate rose from 3.4% to 3.9%, and if that moves convincingly above 4% to say 4.2% with more evidence of a slowdown in wages, that will also help tip the argument in favor of lower interest rates. Supporting this story is a low quit rate, weak employment readings from the ISM, and weak hiring at small businesses amid a growing labor supply.

Wage trackers point to continued slowdown in wage rates and inflation (YoY%)

Source: Macrobond, NJ

Third: slowdown in consumption

Third, we need to see consumer spending, which has been the main driver of economic activity over the past two years, decline. There was some evidence of this happening in Q1 GDP revisions and weak April monthly data, but we need to see more. As we wrote last month, consumer fragmentation makes this difficult, with the top 20% of households in terms of income spending the same as the bottom 60% of households.

The top 20% of the population are well off thanks to their high incomes, which means that inflation is a nuisance rather than a severe constraint. They also have housing and stock market wealth that has risen dramatically and also benefit from higher interest rates – they can put their money into money market funds at 5-5.5% while mortgage borrowing costs may be closer to 3.5%.

It is a completely different situation for those low-income families where high inflation was a much greater burden. There is also growing evidence that the savings these households accumulated in the pandemic era have been exhausted and financial stresses are beginning to set in, with delinquencies on credit card and auto loans rising sharply. There is evidence to suggest that discretionary spending is starting to shrink, and with the New York Fed telling us that 18% of US credit cards are within 90% of their maximum limit, we expect this to become increasingly clear.

The US elections and the issue of interest rate cuts in 2025

The resilience of the US economy in the face of high interest rates has been remarkable, but we expect the pressures felt by low-income families to become more apparent and consumption to slow. So, if we get a combination of cool inflation, a more resilient jobs market, and stalling consumer spending growth, we think the Fed will actually look to move monetary policy from “constrained” to “slightly less restrictive” with a 25 basis point cut in interest rates in September. Federal Open Market Committee meetings in November and December.

We acknowledge that there are a range of possibilities. If inflation fails to slow, the Fed will not cut interest rates, but that could create a more tense economic environment leading to sharp rate cuts next year.

Regarding 2025, we also recognize that the US elections will have a significant impact on the course of the Fed’s policy. For example, the main differences in Donald Trump’s policy versus Joe Biden’s policy are more tax cuts, more controls on immigration, more tariffs, and the potential for major geopolitical shifts. Our feeling is that this would be more supportive of domestic demand while restricting labor supply and raising business costs, which could ultimately lead to a slightly stronger growth story for the US, but also with higher inflation rates. This could mean that the Fed will be more cautious about cutting interest rates aggressively under a Trump administration versus a Biden-led administration.

Content Disclaimer

This publication has been prepared by ING for information purposes only without regard to a particular user’s means, financial situation or investment objectives. The information does not constitute an investment recommendation, nor is it investment, legal or tax advice or an offer or solicitation to buy or sell any financial instrument. Read more

Original post