View Ballygally Images/iStock Editorial via Getty Images

introduction

He knows a lot Deere & Co (New York Stock Exchange: D) as a low-growth American League stalwart, but they miss The transformation the company is currently undergoing that will potentially transform it into Better business and attractive investment going forward (Not that the company has also been a great investment in the past.) This article aims to briefly review the company’s history, what it does, and illustrate my investment thesis. Of course, how an investment thesis is interpreted depends largely on the individual’s investment horizon. This article is not intended for investors with short-term orientations or those who chase “Quick profit“.

Without further ado, let’s start with the company’s history.

History of Derry

Deere has a very long corporate history. Founded in 1837 By blacksmith John Deere in Mullins, Illinois, the company decided to set foot in it In the Agricultural industry. Mechanization did not exist at that time, so she focused on innovation in farmers’ existing tools. These were the tools They are usually powered by horses.

Mechanization arrived around the 1920s, and Derry had to adapt as industry replaced horses. Initially, the company tried to manufacture its own tractor but gave up and Purchased Waterloo Gasoline Engine Company. This company was known as Waterloo Boy Tractor.

Deere then took advantage of its newly acquired company’s expertise and began manufacturing tractors under its own brand. The most popular tractor in the early days was the The Model B tractor, which has been a bestseller for more than 15 years.

Mechanization and population growth continued to advance, so Derry needed to find a way to adapt to the new model; The company decided to take the “energy route.” In 1960, Deere held an event called “A new generation of powerMany merchants and farmers attended, beginning the next era: Manufacture more powerful equipment.

Deere has always maintained its commitment to power, but in the 1990s, with the arrival of technology, the company realized that… It had to make its machines more productive (Not just more powerful). To achieve this goal, the company established Bought Navcom, a leader in positioning technology. This event began the next era for the company: Technological era. This is the era in which the company still lives today, and it is the era that is responsible for its attractiveness as an investment (as I will show later).

Finally, in 2017The company decided to make its most important acquisition ever: Wirtgen for $5.2 billion. Vertgen is The leading company in the field of road construction equipment It helped Deere establish itself in the construction industry. The company currently derives about 21% of its sales from this segment.

A brief overview of Derry

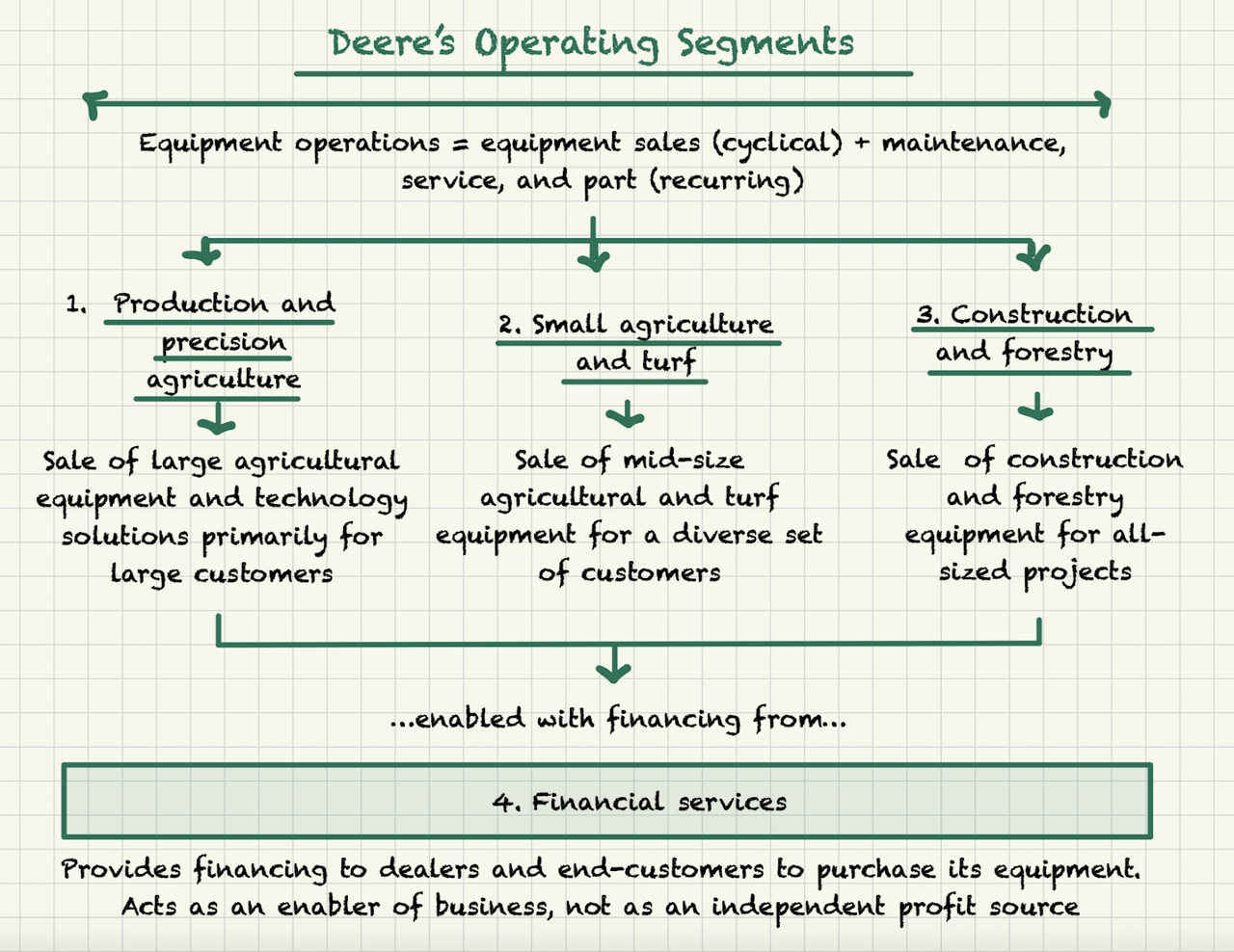

Derry It manufactures heavy equipment for agriculture, construction and forestry industries. The company makes money by selling this equipment and all associated services, such as service, replacement parts, and software subscriptions. The company’s goal has always been Become a farm ecosystem.

Its Equipment Operations business includes several subdivisions, all of which are supported by the company the financial sector. Deere helps its dealers and end-consumers finance equipment purchases through its financial subsidiary.

Here’s a visual summary I made of what the company does:

Made from the best anchor stocks

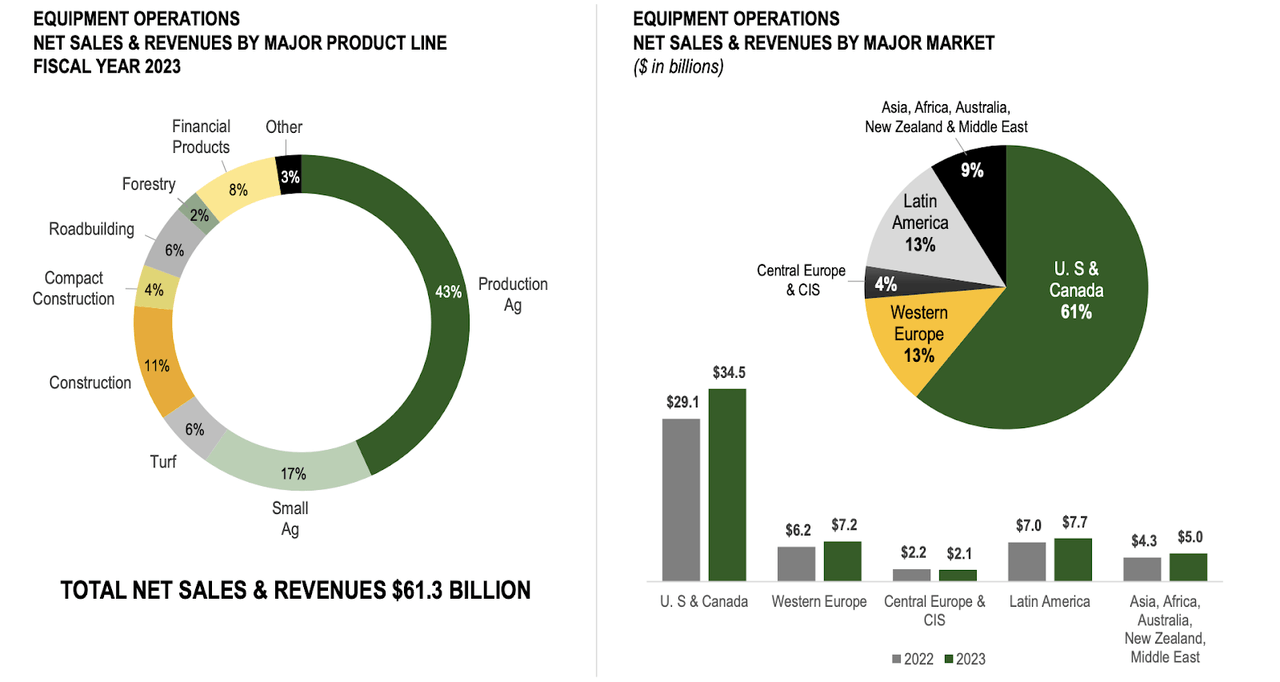

Derry’s operations are It skewed heavily into production and precision agriculture in North America. This makes sense not only because it’s where technology can have the most significant impact, but also because it’s where Deere has historically operated:

Derry Investor Day

Brief investment thesis

there 6 prongs For my investment thesis. Let’s take a look at each individually.

(1) Deere is moving to a much better business model

Management confidently stated that Deere is a technology company (not a manufacturing company) and that they will accelerate the transition towards… Sell solutions to build repeat business.

They can The recurring portion of the business could account for about 40% of sales by 2030Given the higher margin nature of this revenue stream, I think it is It’s reasonable to see a path to +60% recurring revenue in the future. These recurring earnings should help dampen Deere’s historical cyclicality, something management rightly pointed out in a recent earnings call:

We are confident in our ability to achieve higher levels of returns over the cycle while reducing the variability in our performance over time. this It will lead to higher highs and higher lows for our business.

(2) Deere operates in a secular industry where transformation is taking place

The industry has traditionally been agricultural Cyclical yet secular at once (similar to the semiconductor industry). However, thanks to increasing technological penetration, Deere (and its peers) It will shift from benefiting only from farmers’ capital expenditure to benefiting from both capital expenditure and operational expenditure. In an industry where income is generated solely from equipment sales, players will begin to monetize the use of this equipment and related technology.

Why is this appropriate? because Capital expenditures are cyclical, but operating expenditures are highly flexible in the industry responsible for feeding the population. There are few trends more durable than this one, and therefore, I think Deere has a high terminal value protected by its strong moat (more on this later).

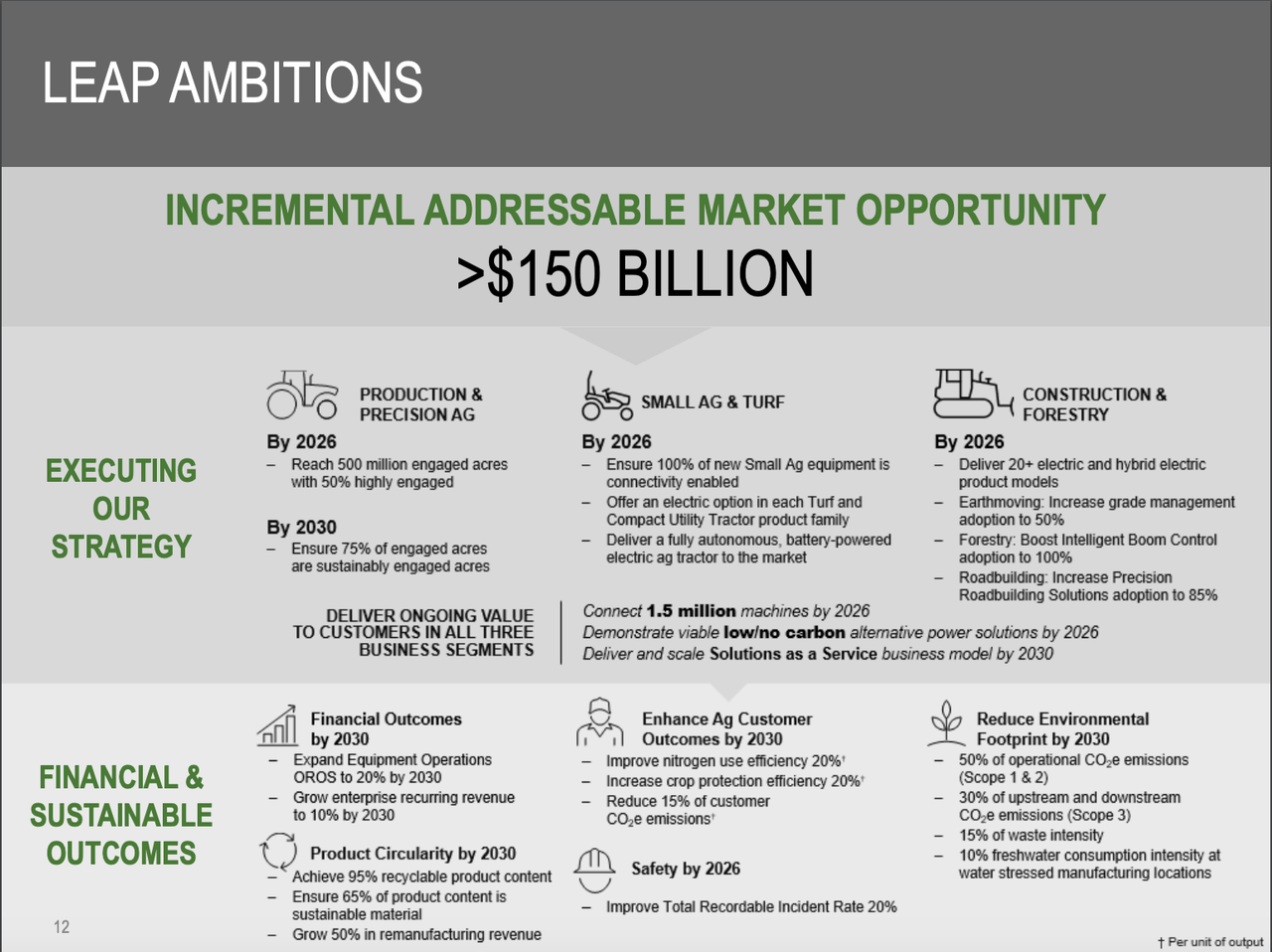

(3) Significant growth opportunity

Growth is always a “concern” for strong companies, but the transformation Deere and the industry are seeing is coming to the fore New growth avenues. Without technology playing this crucial role as expected in the future, Deere has been able to grow revenues at a compound annual growth rate of 5% over the past decade. I know the dire cycle is cyclical, but 2013 was the peak of the previous cycle, so cyclicality is not a relevant consideration in these calculations.

I think Derry You will not be limited by chance Taking into account the emerging opportunity for monetization of farmers’ operations. Management believes Additional addressable market opportunities greater than $150 billion:

Deere Investor Presentation

Management expects to obtain 25% of the added value, which means that… The incremental opportunity for Deere is about $38 billion. Please remember that due to their nature, these revenues will come with a very large margin.

However, we must always be careful as investors in total addressable markets, especially when they come from management. Deere may not reach its estimates, but that does not deny that the opportunity is great.

Another thing worth noting is that They expect their peers to follow a similar strategy But we also expect it to be More aggressive with their “take rate”. AGCO, one of Deere’s peers, hopes to capture about 50% of the value it adds, which is much higher and could make Deere’s value proposition more attractive.

(4) Strong moat and management team

Both our moat and management team are critical aspects of our expected future returns. I believe Derry has a strong moat with several pillars:

-

Installed base: Technology in the agricultural industry needs data to be developed, and this data is collected by the installed base. After more than 60 years of industry leadership, Deere has the most comprehensive base for collecting this data.

-

Traders network: Traders are important in the agricultural industry because farmers cannot afford to go out of business. The company has a fairly extensive agent network, and these agents have long-standing relationships with many farmers. In short, the dealer plays a critical role in any farmer’s purchasing decision, and Deere is well served here.

-

size: Deere is by far the largest player in the industry, which, in addition to allowing it to benefit from a larger installed base, allows it to invest more in absolute terms in R&D while remaining more profitable than its peers.

-

The brand and its history: This leadership also created significant conversion costs, as most farms are family-owned and have been passed down through generations. Switching costs are high because farmers are brand loyal, and equipment costs typically make up a low portion of the total farm cost (about 15%).

Besides this strong moat, Derry has a bit of a Unique compensation structure Focus on growth…but not at any cost. Short-term motivation depends on Operating return on assets and salesThe long-term incentive is based on value added to shareholders. Added value to shareholders Ensures that the management team They are compensated only on the basis of growth that creates value. It was implemented around 2007 by former CEO Bob Lane, who believed this was what Deere needed to become an excellent company for shareholders. Spoiler: It worked.

(5) Reasonable evaluation

Deere is currently trading at a reasonable valuation. To judge the cyclical valuation, we must always be careful with the current earnings level. By the end of this year, management expects to be at or just below mid-cycle earnings. This statement may come as a surprise to many who expect Derry to currently be on a super cycle, but I think what these people are missing is that The company’s recent growth has been largely driven by prices rather than volume. The latter is what creates cycles.

So, keeping in mind that we will be at mid-cycle earnings by the end of the current fiscal year and management expects $5.2 billion in free cash flowand this translates to FCF yield of about 4.7%. This isn’t fully normalized because management believes the company will make about 90% mid-cycle earnings, but it’s close enough and helps us be more conservative.

Assuming the company is able to grow its free cash flow at a CAGR of 5% or more, shareholders should ultimately receive a double-digit return over the long term.. That’s not too shabby for a company that’s considered solid and low-growth.

What’s interesting is that FCF’s CAGR looks very conservative for several reasons. First, this is the pace at which we can expect the company’s revenues to grow, but the new business model should bring several advantages…

-

Margin expansion From the nature of new revenue sources

-

Improve cash conversion Of the working capital benefits that subscriptions bring.

One might also think that its transition to becoming a better company should lead to some multiple expansions for the company, but that’s something I’d rather not count on.

(6) The thesis that began to appear

Deere recently reported its second-quarter earnings. I think this was important because They report that the thesis is starting to take shape. I could write a lot more about this, but I think it can be summed up in the following quote by management during the call (emphasis added):

If we look at 2020, the business was there, or call it, 90% mid-cycle, which is not too far off from where we are today in terms of production and precision Ag. We achieved operating margins of about 16%, and today the middle of our guide is 21%.

Margins have already improved significantly over the course of the cycle, and the company is still in the early stages of its turnaround.

Conclusion

Deere is a good company that is transitioning to a great company and is currently trading at a reasonable valuation. I do not intend to time the crop cycle (which I believe I will not be able to do precisely) and I am well aware that this exposes me to opportunity costs. I don’t care about that opportunity cost, as long as Derry ends up in a better place in the long run.

Meanwhile, keep growing!