JHVEphoto

Investment work

I recommend a Buy rating for Thomson Reuters (tsx:tree:ca) (New York Stock Exchange: TR) when I wrote about it in February of this year, as I was anticipating low-teens EPS growth expectations, which, along with earnings, could deliver Attractive total return over the next two years. Based on my current outlook and analysis, I recommend a Buy rating. The main update to my thesis is that I expect organic EPS to grow faster than I originally expected, as TRI has seen a strong adoption rate for its AI-related products. As more of these products are introduced, I expect organic revenue growth to accelerate. The improved organic growth profile should also support outstanding valuation multiples versus peers.

review

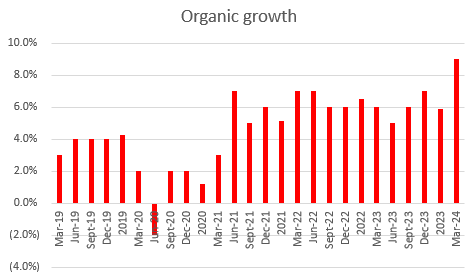

TRI’s recent performance (1Q24 results reported on 2Second abbreviation May) instill more confidence in myself The business fundamentals remain strong. Revenue growth of 8.5% was strong, and growth was even better on an organic basis, growing 9% in the first quarter of 2024, with the three largest segments posting 9.9% organic growth. EBITDA margins expanded accordingly, from 38.9% last year to 42.7% in the first quarter of 2024.

I believe TRI is set to see its organic growth accelerate to potential teens in the coming quarters due to its investments in generative artificial intelligence (GenAI) products. An analysis of TRI’s sector performance shows that management has been able to convert AI investments into actual organic growth:

- TRI was able to achieve accelerated organic revenue growth from 7% YoY in 4Q23 to 9% in 1Q24, with particularly strong adoption in corporates, tax and accounting (T&A) professionals, and Reuters News due to content licensing Artificial intelligence innovator.

- Reuters News, a segment that has traditionally grown in mid-digits, accelerated its organic growth to 17% in 1Q24, marking the second consecutive quarter of strong sequential acceleration (3% in 3Q23, 9% in 4Q20 From ’23, and 17% in the first quarter of ’24). .

The sector/focus area that I expect to help drive overall organic growth is the Legal Professionals segment (largest mix of total revenue), where TRI has committed a lot of resources and seen successful adoption to date. Specifically, over 5,000 customers (quoted from Investor Day) now have access to one or more of the three Gen AI products available: Westlaw AI-Assisted Research, Ask Practical Law AI, and CoCounsel. The reason I say this is because TRI’s Westlaw Precision AI-assisted search (introduced in late 2023) solves a big problem for law firms using GenAI: reducing LLM hallucinations and, at the same time, improving the relevancy and accuracy of search results, And generate answers based on factual data rather than language patterns. In my opinion, this will increase product confidence and adoption rates. The implication here is not only more adoption, but also that TRI has more reasons to justify price increases, and I think customers will be willing to pay because the increase in productivity outweighs the price increases.

A growing number of law firms have noticed the potential positive effects of GenAI adoption, and I don’t see this trend slowing down any time soon. In fact, as more law firms adopt GenAI, there should be an acceleration in adoption because competing law firms do not want to lose their competitive edge. In particular, GenAI significantly enhances the productivity of subscale law firms. In the past, sub-scale law firms tended to be less productive because they lacked the staff/resources to conduct research, which meant that it generally took longer to conduct the same research than a large law firm with multiple law firms. Teams of legal experts. Using GenAI, it enables these small companies to compete effectively against larger companies (for example, GenAI significantly reduces the time needed to find a specific case study); Therefore, I do not think that adoption will be limited to large companies only.

So, I am very optimistic about the soon to be released AI products like Ask Practical Law AI, Intelligent Drafting, Checkpoint Edge AI, Westlaw AI, CoCounsel for UK, Canada, Australia and others.

Law.com

With over 300 AI/ML experts, TRI is certainly well positioned to expand its AI offerings in the future. What really sets TRI apart from its competitors, in my opinion, is its more than 2,500 subject matter experts, who are essential in keeping TRI’s proprietary content up to date and improving the output of LLMs. (Figures and product launches taken from TRI Investor Day 2024).

Margin outlook for TRI is weak in the near term due to required investments in AI-related products. Management indicated in the 1Q24 earnings call that it will reinvest all 75 basis points of margin expansion from operating leverage back into the business in 2024, with most of it going toward generative AI initiatives. Instead of being disappointed, I think investors should be happy that TRI is doing this, because it helps drive organic growth. In this regard, management has raised guidance for the Big 3 segment from approximately 7.5% for organic growth to 7.5% to 8%, and I believe this number will continue to rise, perhaps reaching lower levels as TRI continues to roll out more AI products.

evaluation

Author’s work

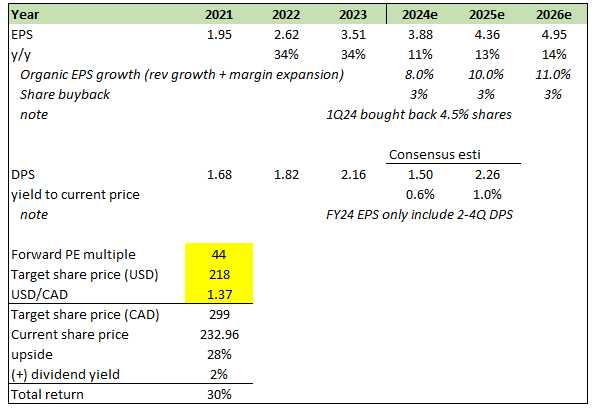

The key updates to my model are an increase in the organic EPS growth assumption from 5% to 8% (the high end of the FY24 organic growth guide) for FY24 and a 100 bps increase to organic EPS growth for FY2026 as I expect AI related products to roll out To continue driving growth. I anchor the EPS growth assumption to organic revenue growth because I expect management to reinvest excess margins into R&D for AI products.

Management also continues to repurchase shares at an attractive pace of 4.5% in Q1 2024. As such, I remain confident that TRI will repurchase at least 3% of the stock over the foreseeable future (note that 3% is the average historical).

Finally, I believe the market will continue to value TRI at an excellent multiple to its peers, at 44x forward PE. The reason for my confidence is that organic EPS growth expectations are accelerating.

Author’s work

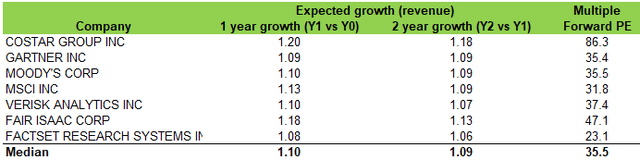

Investors who have followed the TRI stock story for a while will know that a common response to a high valuation has been weak organic growth compared to other database peers. Their peers (shown below) have generally grown from the high single digits to the low teens and trade at around 35x forward PE on average; This contrasts with TRI of the past, which only grew to mid-single digits but traded at over 30x as well. With this Gen-AI-led strategy, there’s a good chance TRI’s organic growth will outpace its peers, perhaps growing organic revenue by over 10%, and that should justify TRI trading at a premium. On a historical basis (forward PE), over the past five years, TRI has mostly traded at a premium to its peers (about 14% premium). The premium is currently 21%, and I believe the additional 7% premium is justified by the accelerating organic growth profile.

Author’s work

risk

TRI’s capital expenditures as a percentage of revenue are expected to continue to increase due to investments in M&A-related integration and product development, including support for its generative AI product roadmap. Depending on the size of the investment, this may affect the TRI capital return policy, which will reduce the EPS growth assumption of 3% per year. New AI-related products may not see the same rate of adoption as those being deployed today, which would make my estimates overly optimistic.

Final thoughts

My recommendation remains a Buy rating for TRI. Despite the weak macro environment, TRI achieved strong organic revenue growth and expanding margins. TRI’s strategic focus on products is accelerating growth, particularly in the Reuters News, Legal, Tax and Accounting segments. While near-term margins may come under pressure due to AI investments, I expect the long-term benefits to outweigh the costs. Looking ahead, I now expect high organic EPS growth, which should justify TRI’s premium rating.