Tebabat

Some time ago I wrote a cautious article about the Global Health Care Fund abrdn (New york stock exchange: thw) (formerly known as Tekla Global Healthcare Fund), noting that it appears to be a “capital return” fund to avoid. By investors. While some analysts said claimed That the THW Fund is an investment for the next decade, I was not entirely sure about the THW Fund and preferred the abrdn Healthcare Opportunities Fund (New York Stock Exchange: THQ), which has a more sustainable distribution policy.

Although I don’t know how the rest of the contract might play out, based on their respective returns so far, my preference seems correct. Since my January 2023 article, the THQ Fund has generated double-digit total returns while the THW Fund has generated negative total returns (Figure 1).

Figure 1 – THW has underperformed THQ since January 2023 (Searching for Alpha)

However, with so much time having passed since my last article, I wanted to take a fresh look at THW and THQ to see if my recommendation would remain the same.

Unfortunately, the recent increase in distribution by THQ Fund has raised the distribution yield to a level that is likely unsustainable. Over time, I think the THQ fund will suffer from NAV amortization like THW.

Instead of THW and THQ funds, investors can create their own “high yield” fund by buying a low-cost sector ETF and periodically selling units to pay themselves high “cash flow.” As long as the total returns are sufficient to fund the cash flow, this may be a better alternative.

A brief overview of the fund

Tekla Capital Management is a healthcare investment firm and manages both the abrdn World Healthcare Fund (“THW”) and the abrdn Healthcare Opportunities Fund (“THQ”). British asset manager abrdn acquired Tekla in 2023, changing the name of the funds.

In addition to THW and THQ, Tekla/abrdn also manages abrdn Healthcare Investors (HQH) and abrdn Life Sciences Investors (HQL) closed-end funds (“CEFs”).

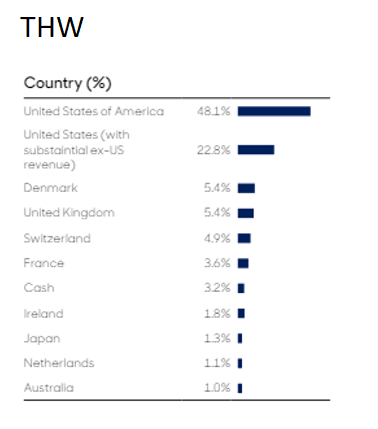

Both THW and THQ are broad healthcare funds that invest mostly in public healthcare companies. The main difference between THW and THQ is that THW is a global fund, while THQ mainly focuses on US stocks (Figure 2).

Figure 2 – THW geographic allocation (abrdnthw.com)

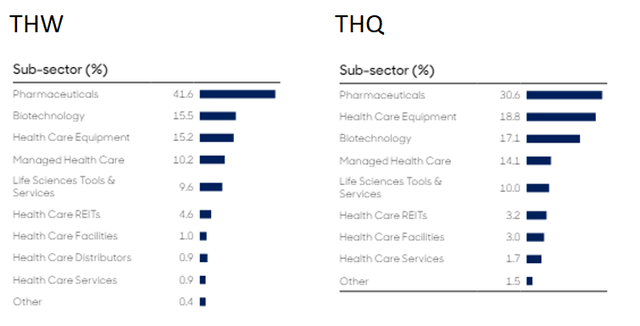

Figure 3 compares sub-sector allocations between the two funds. The key difference here is that the THW fund has a higher allocation to pharmaceuticals (41.6% vs. 30.6%), while the THQ fund has higher allocations to other healthcare subsectors such as healthcare equipment (18.8% vs. 15.2%). Biotechnology (17.1% vs. 15.5%), and Managed Healthcare (14.1% vs. 10.2%).

Figure 3 – THW and THQ sub-sector allocations (abrdnthw.com and abrdnthq.com)

Beware of major money backs

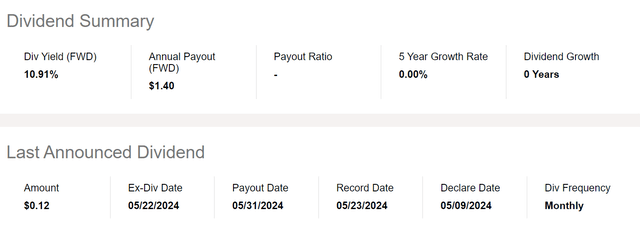

The main issue I had with the THW fund was that its distribution rate, currently set at $0.1167 per month or a 10.9% forward return on market price, is higher than the fund’s total returns since January 2023 of -2.9% (Figure 4).

Figure 4 – THW pays a very high distribution yield (Searching for Alpha)

Usually called funds that do not receive their distributions “Return of capital” Funds are characterized by amortization of net asset values (“NAV”). This is because “capital return” funds typically fund their distributions by liquidating net asset value; That is, the fund’s high distribution returns are financed by the investor’s own capital.

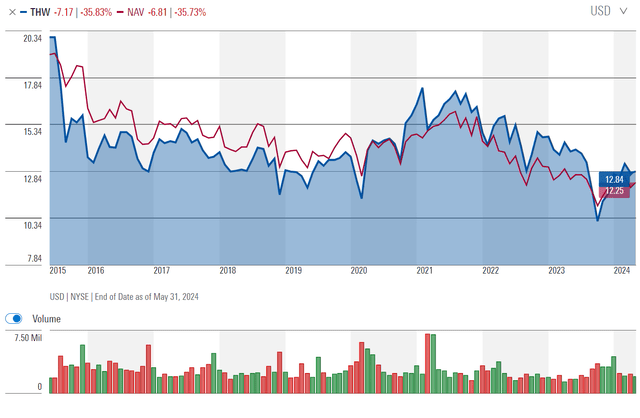

Since the market prices of closed-end funds tend to track their net asset value, “capital return” funds also tend to consume market prices. Since its inception, the THW Fund’s NAV has declined by 35.7% and its market price has declined by 35.8% (Figure 5).

Figure 5 – THW has an NAV amortization problem (morningstar.com)

While income-oriented investors typically claim that they have not “lost money” because market price declines are “unrealized,” the reality is that these unrealized losses are unlikely to be recovered, as the fund’s assets have already been liquidated and paid out to investors on Distribution format.

For example, imagine a retired investor who bought a THW fund at $16 per share in May 2021 but now needs to sell the investment to fund a major purchase or expense. At the time of his investment, the investor was looking at an attractive forward yield of 8.75% ($1.40/$16).

Fast forward to today, the fund is worth just $12.85 on the public markets with an NAV/share of $12.25. While it is true that the investor received “distribution income” of $1.40 per year for three years or a total of $4.20 in distributions, the value of his investment decreased by $3.15 per share in the public markets. The market doesn’t care about the investor who bought his stock at $16 per share. The market is only paying the value of the shares at the moment. So Total returns For an investor holding a THW fund for three years it is only $1.05 per share, or ~2.2% per year.

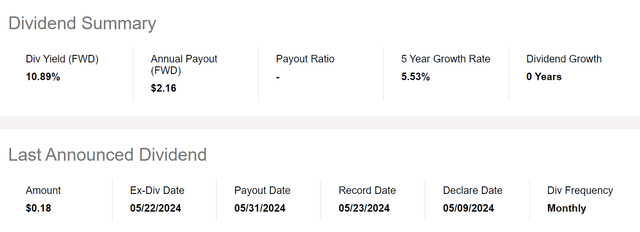

THQ is now unsustainable as well

Unfortunately, since coming under abrdn’s management, THQ has recently raised its monthly dividend from $0.1125 per share to $0.18 per share (Figure 6).

Figure 6 – THQ raised its dividend (Searching for Alpha)

On the surface, this sounds great for investors, as the forward yield on the THQ fund has now been boosted to 10.9% over the market price (Figure 7).

Figure 7 – THQ returns 10.9% (Searching for Alpha)

Unfortunately, I think the $2.16 per year forward distribution on the THQ fund may set up the THQ fund to become yet another abrdn “capital return” amortization fund.

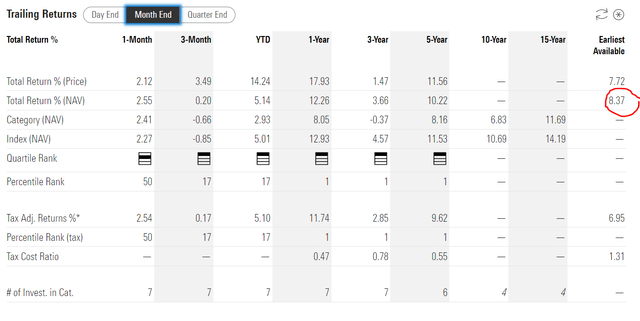

Since inception, the THQ Fund has averaged annual returns on NAV of just 8.4% per year (Figure 8). Based on a recent NAV of $21.45, the THQ Fund pays a forward yield of 10.0%. The gap between long-term returns and forward returns will be funded by the gradual erosion of THQ’s net asset value.

Figure 8 – THQ Historical Returns (morningstar.com)

What do you do for income-oriented investors?

With THQ also quickly becoming an amortization “capital return” fund, what should long-term investors do? First, investors should not panic. The amortization of NAV mentioned above is a long and gradual process and does not happen overnight. So investors should not panic by selling their investments in THW or THQ. Instead, they should start looking for alternatives.

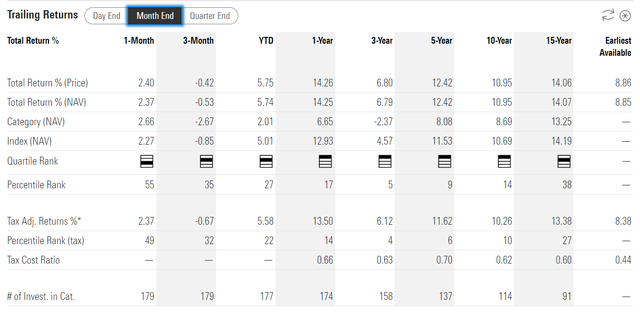

One potential alternative is to consider the Healthcare Select Sector SPDR ETF (XLV). XLV is a low-cost passive ETF focused on the healthcare sector. Historically, XLV is a top-quartile fund that has outperformed most healthcare-specific mutual funds like THW and THQ (Figure 9).

Figure 9 – Historical Returns45 (morningstar.com)

The main drawback of the XLV ETF is the low distribution yield, which is currently only 1.5%. However, investors can create their own “high yield” fund of XLV by liquidating a fixed amount of the investment each quarter to match their cash flow requirements.

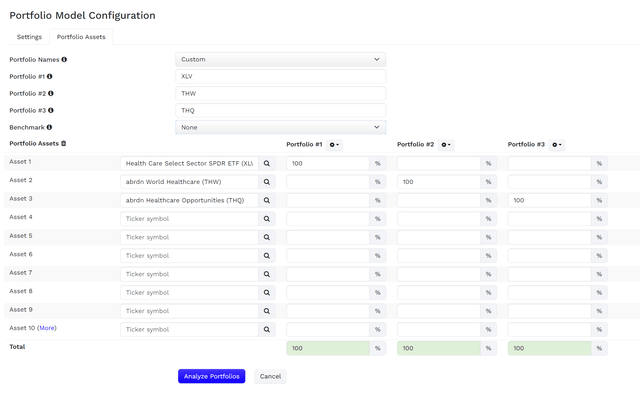

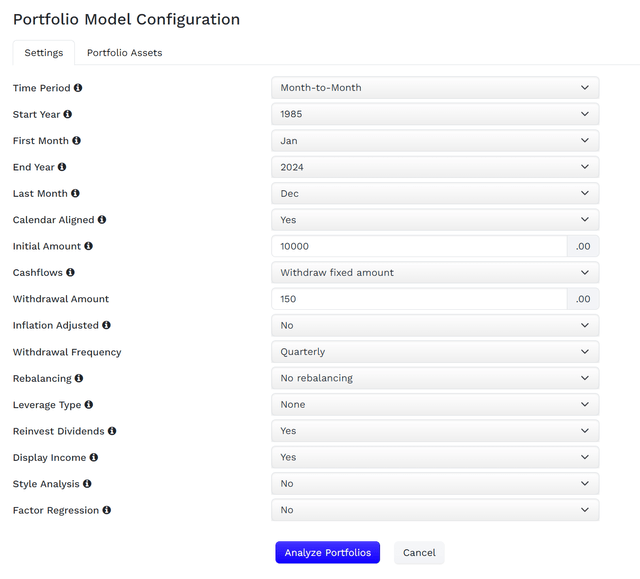

For example, consider a hypothetical comparison between XLV, THW, and THQ (Figure 10). The investor invests an initial $10,000 in each fund and makes a quarterly withdrawal of $150, or an annual return of approximately 6% (Figure 11).

Figure 10 – Hypothetical comparison between XLV, THW and THQ (Author created using Portfolio Photographer) Figure 11 – The analysis assumes a constant cash withdrawal of $150 per quarter (Author created using Portfolio Visualizer)

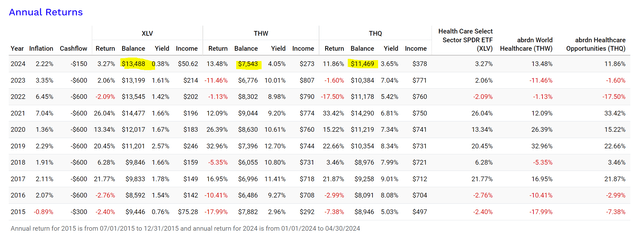

In the long run, we can see that the XLV portfolio ends up with a higher ending balance because it… Total returns Top (Figure 12).

Figure 12 – XLV portfolio ends with a higher ending balance (Author created using Portfolio Photographer)

When comparing securities, investors should always consider total returns and not just distribution yields.

Conclusion

Since January 2023, the THW Fund has generated negative total returns and has underperformed my favorite healthcare fund, the THQ Fund. Unfortunately, THQ Fund recently boosted its distribution rate following abrdn’s acquisition of the fund manager, Tekla. I believe this will turn the THQ fund into a long-term “capital return” fund like the THW fund.

I recommend that income-oriented investors looking for exposure to healthcare may be better served by investing in low-cost ETFs like XLV and creating their own “high-yield” fund by selling units periodically to provide high cash flows.