com.champpixs

introduction

As you probably know, BDCs have long been considered risky investments due to their business models and high returns. For me, they are ideal investment vehicles, as income is my main focus in retirement. However, not all BDCs are created Equal, every investment comes with some type of risk. Furthermore, with the current high interest rate environment putting downward pressure on many companies, some BDCs with lower credit quality have seen their portfolios negatively impacted.

This indicates the term: Quality over quantity, one of my core values when investing. One BDC that comes to mind that doesn’t currently fit these criteria is Triple Point Venture Growth (NYSE: TBVG). As a result of persistent headwinds, lower financial conditions and tight earnings coverage, I maintain a Sell rating on BDC. In this article I Discuss their fundamentals, recent quarter and earnings coverage.

Previous evaluation

I previously covered the growth of the Triple Point project once before back in December in an article titled: Triple Point Project Growth: This 15% return is a cautionary tale. Although the yield was attractive at the time, BDC saw a decline in fundamentals, leading me to rate it as a sell nearly 6 months ago. Fast forward and the share price has continued to fall an additional 14.6% at the time of writing.

I previously discussed the company’s third-quarter earnings, which saw it beat analyst estimates on both its top and bottom lines. I also touched on Brookings Doha Bank’s balance sheet, which was strong with manageable debt maturities. But despite this, TPVG has seen a worrying rise in its outstanding receivables, resulting in poor performance compared to its peers.

Why quality matters more than quantity

Business development companies (BDCs) are considered risky investments mainly because they lend to lower and middle market companies with lower EBITDA. This is just the nature of their business model, but some of the business development companies that provide loans to these companies are considered high quality. What’s more, many of them have performed well in a rising interest rate environment, even outperforming the S&P in the process.

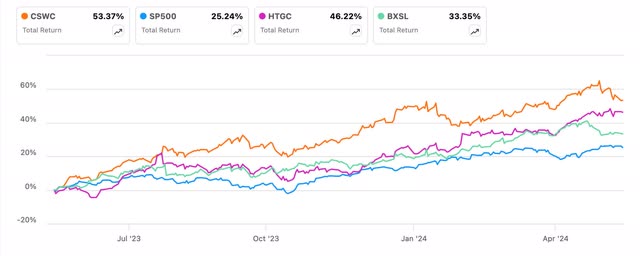

To name a few, Capital Southwest (CSWC), Hercules Capital (HTGC), and Blackstone Secured Lending (BXSL) are three BDCs that have performed exceptionally well, outperforming the S&P in total returns in the past year. There are many other business development companies that have also performed well, but these are three that are better known within the sector.

Seeking alpha

As a result of their higher returns, many investors have turned to this sector over the past couple of years, leading many to trade at premiums above their historical valuations. But don’t forget, just because a company has a higher yield, doesn’t mean it will outperform when it comes to total returns.

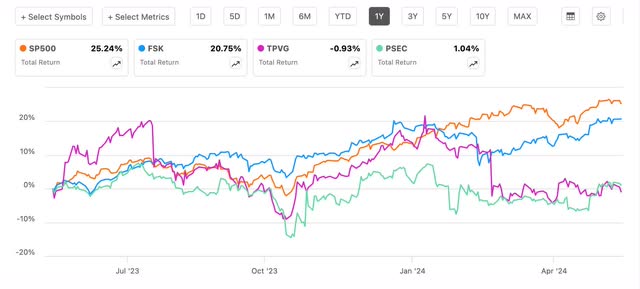

However, those with stronger fundamentals were the exception, with the three mentioned previously included in those I consider to be of higher quality. Looking at the chart below, there are examples of business development companies (BDC) that have performed poorly over the past year. Although this does not mean that they are necessarily lower-tier business development companies, their profiles have proven to be riskier, resulting in their poor performance.

Seeking alpha

Latest earnings

Triple Point Venture Growth reported first-quarter earnings on May 1 with a loss on both the top and bottom lines. Net investment income of $0.41 missed by $0.02 while gross investment income missed estimates by less than $1 million.

On a quarterly basis, the value of national insurance fell by approximately 13% from US$0.47, while the value of international investment fell from US$33 million. Companies go through periods when their financials decline, but seeing them decline on an annual basis should raise concern. Both NII and TII declined year over year as you can see in the chart below.

|

S1’23 |

S1’24 |

|

|

National Insurance (In millions) |

$18.6 |

$15.5 |

|

TII(In millions) |

$33.6 |

$29.3 |

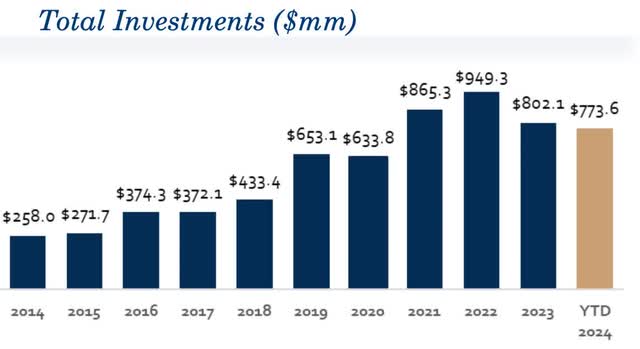

This can be attributed to the decrease in their overall investment. You can see from 2022 so far that the value of TPVG’s portfolio has shrunk significantly from $949 million to $773.6 million at the end of the first quarter. The venture capital market in particular has faced difficulties as a result of high interest rates. While TPVG’s total investments are down, management said it suspects activity will pick up in the latter half of the year.

TPVG Investor Presentation

New growth

Investors have become more cautious and selective as a result of the macro environment, but the Brookings Doha Center was able to make some investments during the quarter. So, some positives to start the financial year. Triple Point saw an increase in term sheets signed, which continued from the fourth quarter. These increased by an additional 30% to $130.5 million and they have already signed nearly $30 million of new term sheets for next quarter. This was up from $100 million in the previous quarter and $58 million in the third quarter.

Additionally, they committed $10 million of new commitments to one new portfolio company and management reported that they actually closed on double that amount in the second quarter with $20.5 million of new commitments. Therefore, the upcoming quarters currently look positive, which could lead to growth in its top and bottom lines in the foreseeable future. If the company can implement new commitments in the coming quarters while growing National Insurance and its investment portfolio, I would consider upgrading the BDC to a contract.

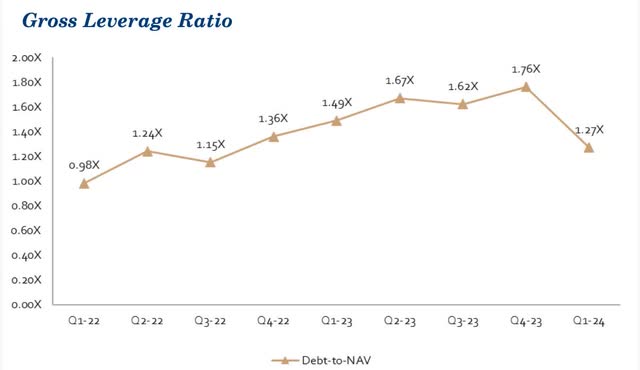

Low leverage

Although the decline in its financial position led to its weak performance, TPVG strengthened its balance sheet, which was another positive during the quarter. The leverage ratio decreased significantly from the previous quarter to 1.27 times, which is positive for the company.

TPVG Investor Presentation

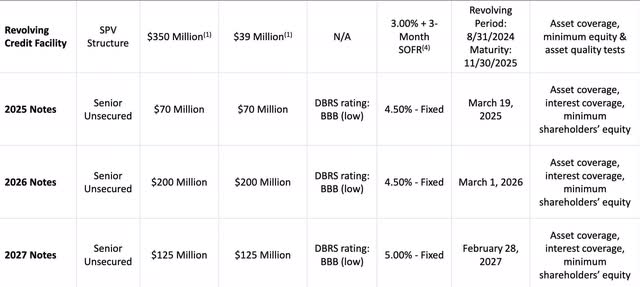

This compares to two of its venture capital-focused peers, Horizon Technology Finance (HRZN) and Trinity Capital (TRIN), which had leverage ratios of 1.16x, respectively. They also had ample liquidity of $312 million and $1 million in cash, which was down from $172 million in the previous quarter. This will likely be used to pay down debt, reducing leverage. Furthermore, its debt maturities are also good, with none due this year, and $70 million due in March 2025.

TPVG Investor Presentation

Persistent headwinds make it a sell

For starters, TPVG had non-distributable income of $42.3 million, which could be used to fund the dividend for a temporary period if coverage dropped below 100% for unforeseen reasons. As a result of Triple Point’s lower net investment income, its dividend coverage has become tighter, with coverage at approximately 103%.

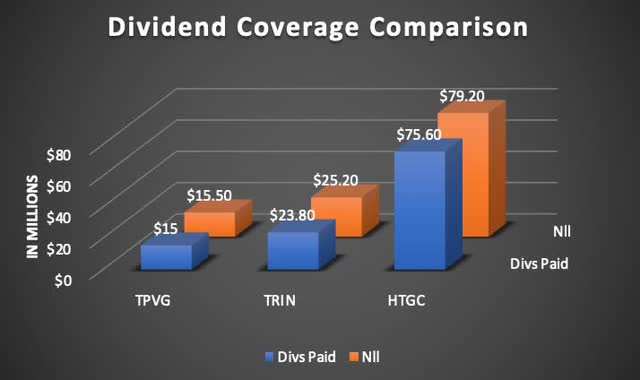

Using its 37,649 outstanding shares, TPVG’s net investment income of $15.5 million barely covers its dividend of $15,436. This compares to peers Hercules Capital and Trinity Capital whose coverage has been higher over recent quarters. HTGC had the highest coverage with $79.2 million in NII and $75.6 million in dividends paid. TRIN was a little tougher with $23.8 million paid out in dividends and $25.2 million in NII.

Author’s creation

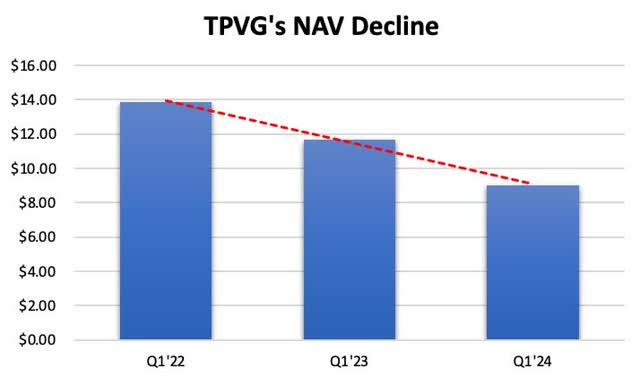

Both had earnings coverage of 125% and 108% respectively, which could also be a reason for their outperformance and TPVG’s lower prices. Furthermore, while its peer HTGC saw its NAV rise quarter-on-quarter, TPVG continued to erode to $9.02. While BDCs periodically see their NAV decline, an upward trajectory in their NAV is something investors should look for when holding a BDC.

In the chart below, you can see Triple Point Venture Growth’s NAV has continued to decline significantly over the past two years by approximately 35% from $13.84, which is a significant amount and something you never want to see from a BDC. For comparison purposes, HTGC’s NAV, which I consider the best of the venture capital-focused group, grew approximately 7.5% over the same period from $10.82 to $11.63. This also grew on a sequential basis, up from $11.43 in the previous quarter.

Author’s creation

Evaluation and risks

For the above reasons, TPVG is currently trading slightly above its NAV price of $9.31 at the time of writing. The price of BDC is down roughly 15% over the past year, and while its high yield is attractive right now, there are better options worth considering. As a result of the macro environment, which will continue to put downward pressure on borrowers for the foreseeable future, TPVG could also see further decline.

Especially if their outstanding receivables rise in the coming quarters, or if their fundamentals continue to deteriorate. As a result, I don’t think the valuation is sufficient to invest here at a P/NAV ratio of 1.02x. Despite the higher yield, I think investors should wait for improvements in their fundamentals, or a discount, which gives them a margin of safety in riskier BDC.

com. cefdata

Furthermore, Triple Point’s outstanding receivables continued to rise on a sequential basis. Although it improved compared to Q3 during my last thesis, it remained well above its peers at 8.5% at cost and 6.8% at fair value. This percentage increased from 5.3% and 4.0% in the fourth quarter and 8.3% and 5.1%, respectively, compared to the same quarter last year. So, the risks of TPVG at the moment are too much.

minimum

Triple Point Venture Growth is a riskier play within the BDC sector, and with interest rates remaining higher, at least in the near term, I think its risks are too much, outweighing the higher return, prompting me to assign a Sell rating for now. Additionally, there are better business development centers in this sector for investors looking for higher returns.

However, management expects activity to pick up in the second half and already has deals in place with term sheets signed and new commitments for next quarter. While this looks good for Brookings Doha Bank, the macro environment is likely to continue to pose challenges for borrowers. This could lead to a further decline in their fundamentals in the future. As a result, I continue to rate TPVG as a Sell as there are better options in this sector.