Colin Anderson Productions Pty Ltd/Digital Vision via Getty Images

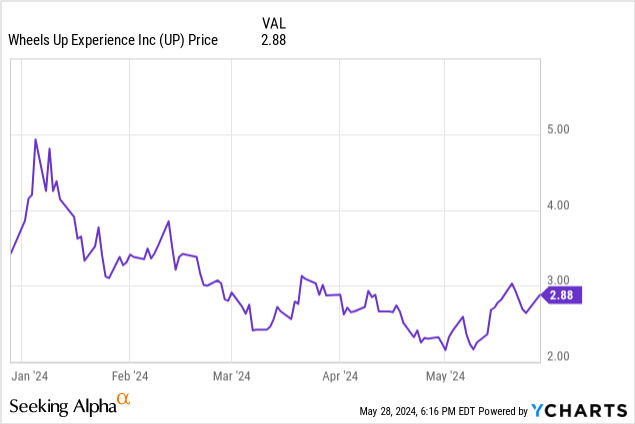

2024 has proven to be a difficult year for turnaround stories, especially for SMEs. This is especially true for Wheels Up (New York Stock Exchange: UP), the private airline that It was among the first (along with NetJets) to take the subscription/membership model to something previously thought to be the bastion of the wealthy: private jet travel.

However, in the years since Wheels Up’s IPO in 2021, the stock has lost billions in market value as demand waned and profitability declined. The company has brought on new management, new investors, and a new plan to turn the proverbial course: But the question for investors now is: Will Wheels Up succeed?

Wheels Up is undoubtedly one of the most interesting and unique companies to go public in the past few years. The years, and the steep decline in its stock price since the euphoric days of the pandemic era when nearly all new issues were greeted by meme-chasing enthusiasts, are worth at least a look. To cut to the chase: I’m starting the Wheels Up at neutral. While I’m broadly positive about the company’s deal with Delta Air Lines (D) and the opportunity to increase revenue through corporate group sales, it is not clear whether Wheels Up will right the ship quickly enough before exhausting all its resources again.

I now have this stock on my watch list, but I’m content to stay on the sidelines until we see a significant drop in the stock price or additional news on the company’s turnaround plan.

Wheels Up overhaul plan

We’ll start with the basics first: What exactly is Wheels Up doing to change itself?

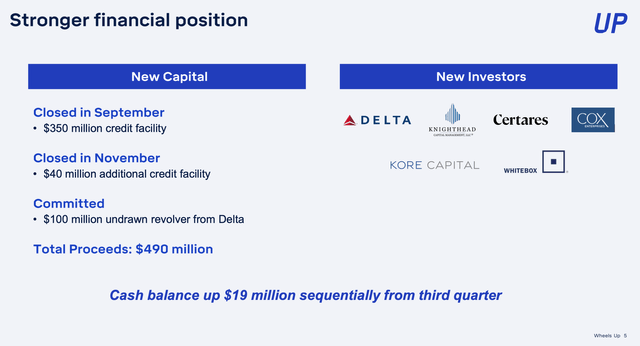

Late last year, Wheels Up struck a deal with a consortium of investors, led by Delta Air Lines (the leading US airline by many measures) to provide $490 million in additional liquidity, much of it in dry powder, in new credit facilities.

Wheels up investment partners (Wheels Up Q4 Contributor Group)

Beyond the massive expansion of liquidity here, many investors viewed the deal as a sign of confidence in the company: If Delta, the most profitable airline in the U.S., is willing to sink capital into Wheels Up, it’s unlikely to be a disruptive deal. . Adventure – or so the thinking went.

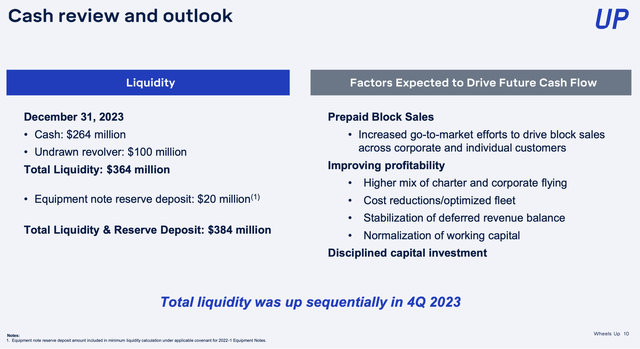

But the partnership was also more than just financial. Wheels Up also sought to support the weaker charter and membership application More corporate sales. In particular, by partnering with Delta and its business network, the company plans to achieve more prepaid sales, directing focused sales efforts to reserving capacity on its aircraft early.

Wheels for raising liquidity and the transformation plan (Wheels Up Q4 Contributor Group)

According to the company, corporate sales have many additional benefits. First, a lot of business travel takes place Monday through Thursday, which has helped Wheels Up increase capacity and fleet utilization and further diversify away from weekend travel. Secondly, the company also noted that corporate customers tend to spend more on flights than individual members.

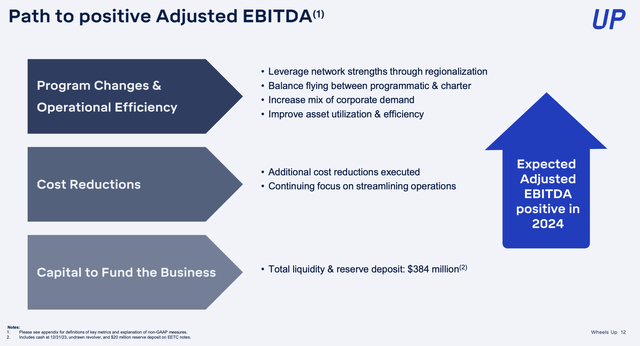

The company combines these enterprise sales efforts with more cost-conscious aviation as well. It has reduced its choice of routes and focused on regions with profitable aviation sectors. On top of continued OPEX cost discipline, the company continues to forecast Positively adjusted EBITDA in 2024:

The path to positive adjusted EBITDA (Wheels Up Q4 Contributor Group)

How are things going so far in 2024?

It’s still early days, of course, in the Delta partnership, but the stark reality is that as things stand, it’s not a pretty picture for Wheels Up. The company really depends on these mass sales to succeed, because without them, revenues would decline dramatically (also partly driven, it must be said, by the company’s own decision to cut back on unprofitable routes).

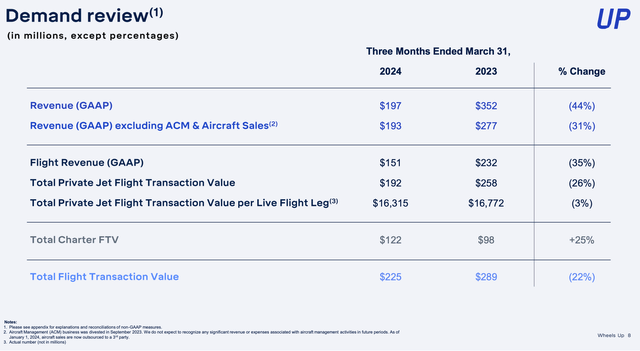

Revenue declined in the first quarter, which Wheels Up reported in early May -44% on an annual basis. Now, much of the revenue decline is due to the company’s decision to also exit the business of managing and selling aircraft. However, when we look at the revenue from the flights themselves (which is now the only source of revenue, alongside memberships), the company saw a 35% decline year-on-year.

Wheel demand overview (Wheels Up Q1 Contributor Group)

Meanwhile, total private jet transaction value (the sum of total member spending on private jet flights) declined -26% year over year to $192 million. The good news: Charters are growing, thanks in part to much-needed big-ticket sales. The company is noticing an uptick in comp sales, according to CEO George Mattson on a first-quarter earnings call:

Charter’s total FTV for the first quarter grew 25% year over year, reflecting increased customer spending on Charter’s services. This lucrative flying, which is not guaranteed and based on market rates, represents just over 50% of the value of flights offered to our customers. We are also seeing improved mix in our commercial businesses, thanks in part to continued momentum in our partnership with Delta, supported by our strong operating performance. Our private aviation solutions complement Delta’s premium business offerings, offering high-value business customers the choice between business and private travel, while creating more opportunities for weekday travel to complement the weekend focus we typically see from our leisure travelers. This balance is a key element of our financial plan to enhance asset utilization and profitability in the future.

We saw progress over the course of the last quarter with our fastest growth in comp sales, which exceeded 30% year over year. We also saw a 40% year-over-year increase in group purchases over $1 million.

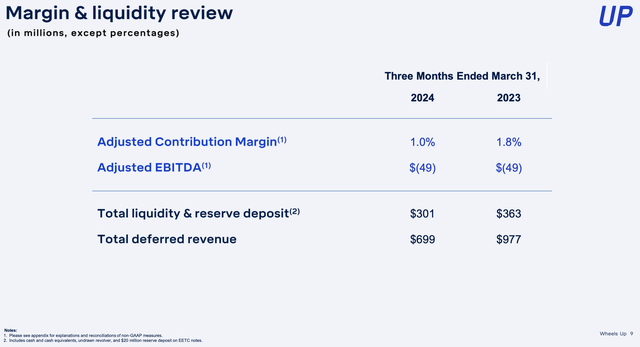

Unfortunately, profitability remained a challenge. The company burned $49 million in adjusted EBITDA in the quarter (flat compared to last year, but with a lower revenue base), while adjusted contribution margins, which essentially strip out a portion of setup and consolation costs, fell by $80. basis points on an annual basis to 1.0%.

Wheels up the latest liquidity (Wheels Up Q1 Contributor Group)

However, management noted that fleet reductions helped March exit trends show a higher adjusted contribution margin than the entire first quarter. However, liquidity remains limited: Even after accounting for Delta’s investment, Wheels Up only has $301 million in total liquidity remaining, including undrawn capacity on its revolvers.

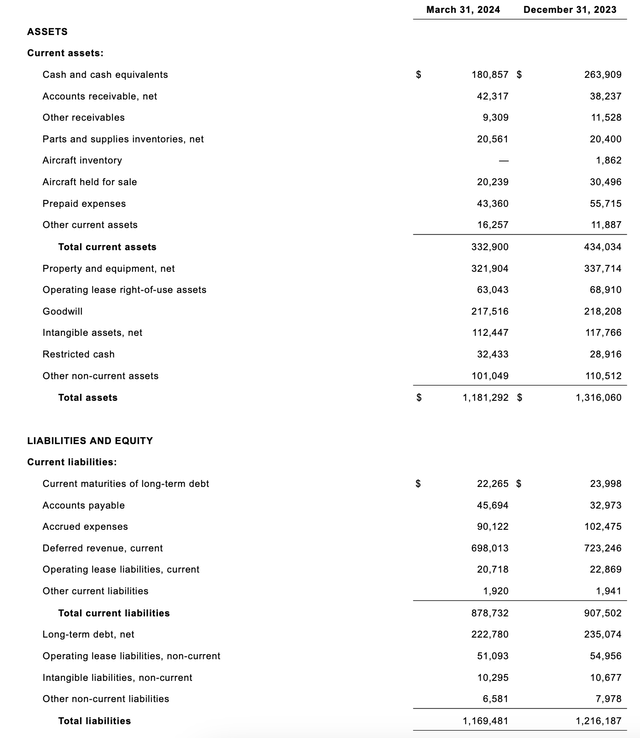

As shown in the chart below, actual cash on its books was just $180.9 million, compared to $222.8 million in drawn down debt.

Wheels up the balance sheet (Wheels Up Q1 Contributor Group)

Meanwhile, first-quarter free flow was $77.7 million, even higher than the $49 million in adjusted EBITDA losses. At this current burn rate, Wheels Up will exhaust its available liquidity very quickly.

Main sockets

Needless to say, there are big risks for Wheels Up on the horizon. At current stock prices near $3, the company trades with a market cap of just $2 billion, reflecting investors’ lack of confidence in Wheels Up’s turnaround plan. Two factors we will need to see play out in the remainder of this year, namely collective corporate sales success and improvements in contribution margins that could help turn adjusted EBITDA positive and stop cash burn. But until then, I will continue to be cautious on the sidelines.