Editor’s note: Seeking Alpha is proud to welcome Johannes Kirchmeier, CFA as a new contributing analyst. You can become one too! Share your best investment ideas by submitting your article to our editors for review. Get published, earn money and get exclusive access to SA Premium. Click here to learn more »

Hiroshi Watanabe

Investment thesis

Start coverage on Uber (New York Stock Exchange: Uber) with a HOLD rating because I find that Uber is valued fairly in line with its industry peers at an average of 3.2x EV/Sales TTM.

Furthermore, I believe Uber is well positioned to benefit from the long-term self-driving trend with the positive market dynamics surrounding the company. Uber leverages its moat in the ride-hailing industry driven by its market-leading position, scale, and platform-based network influence.

I expect the stock to be able to deliver an annual return of more than 10%. investors in the next five years. This forecast is based on financial projections using conservative revenue estimates that are well below historical growth rates (10% CAGR23-28).

For investors looking to build a position in Uber, I suggest waiting for the stock’s current downtrend until a clear trend reversal occurs.

Introduction to Uber Business model

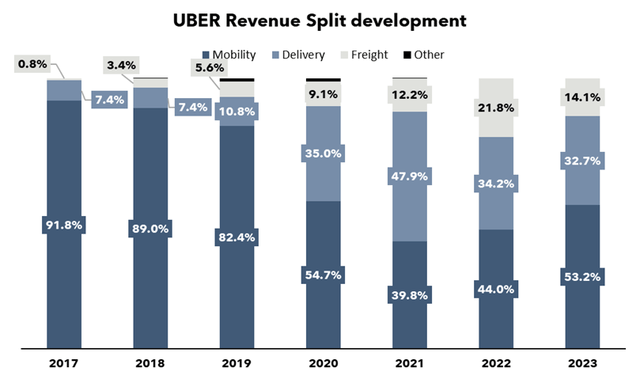

Today, Uber generates revenue across 3 different revenue streams:

- Uber Mobility (53% of 2023 revenue)

- Uber Delivery (33% of 2023 revenues)

- Uber Freight (14% of 2023 revenue)

Uber transportation

At 53%, mobility is by far the largest business sector and the backbone of business. It’s the classic ride-sharing business we know as Uber. Today, Uber is active in more than 70 countries and more than 10,000 cities.

Uber delivery

The second largest unit is the delivery segment, which accounts for 33% of Uber’s revenue. Through its “Uber Eats” brand, Uber operates an online food ordering and delivery platform that Uber launched in 2014. In the US, Uber Eats has a 23% market share because the most dominant player DoorDash covers 66% of the market.

Uber for shipping

The freight forwarding sector is the newest among all the business sectors having started in 2017. However, it has only grown significantly with the acquisition of the logistics platform “Transplace”. On this platform, Uber connects truck drivers with goods that need to be shipped, making transportation of goods and shipping easier and more efficient. The platform also facilitates real-time shipment tracking as well as live chats for both parties to communicate in case of any changes.

In the chart below, you can see how Uber has diversified its business model over the years:

Developing Uber’s revenue mix (author)

Finance

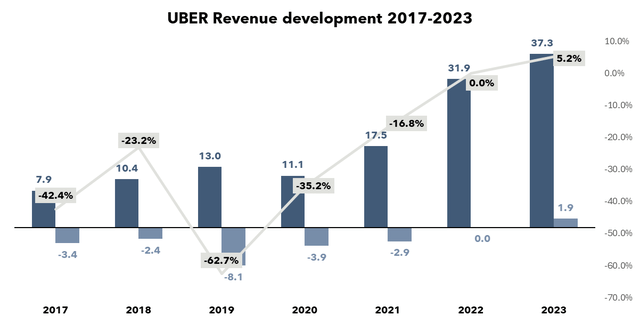

In 2023, Uber finally broke even for the first time, achieving EBITDA of $1.9 billion on revenue of $37.3 billion (5.2% margin). Furthermore, despite a coronavirus-induced decline in 2020, the company has grown at an impressive +29% CAGR from 17-23.

Financial overview 2017-today (author)

In Q1 2024, revenues were up +15% year over year and average. EBITDA was up +82% year over year. Additionally, management’s guidance for Q2 2024 reported +18% to +23% growth in gross bookings year-over-year on a constant currency basis and adjusted EBITDA of $1.45 billion to $1.53 billion, which is This represents a growth of 58% to 67% year-on-year. This seems very realistic as it is very much in line with Q1 2024 year-over-year gross bookings growth of +20%. I’m also not too concerned about the earnings miss ($0.31 loss per share vs. $0.53 analysts’ estimates for earnings per share) because it’s mostly related to one-time things like settling legal disputes and delisting shares.

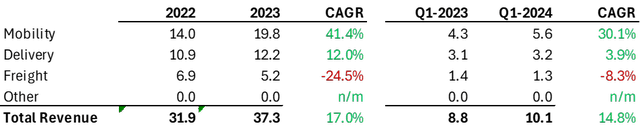

However, one area of concern to me is the cyclical freight business which continued to decline again in Q1 2024 after falling from US$6.9 billion in 2022 to US$5.2 billion in 2023 (-24.5%) and declining dramatically. -8% greater from Q1 2023 to Q1 2023. Q1-2024. As this trend continues after the Transspace acquisition, it makes me wonder whether current management has complete control over the integration of the new business unit.

Revenue growth by business unit (Uber 2023 10K, Uber’s first quarter earnings release)

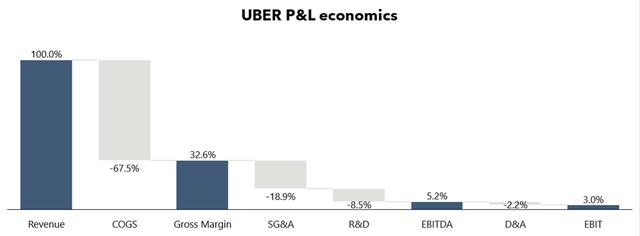

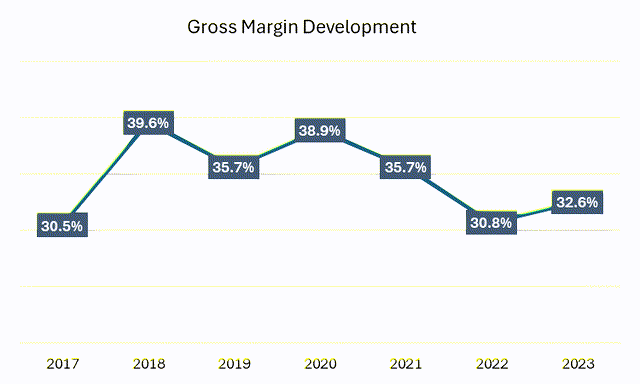

Additionally, the company’s gross profit margin remains fairly low at approximately 33%. This puts a lot of pressure on Uber’s cost structure and is a result of Uber’s low-margin business model:

Profit and Loss Economics 2023 (author)

You can see in the chart above that Uber spends approximately 67% of its revenue on cost of goods sold. This is mostly related to driver commissions and insurance expenses. However, historically, Uber has also been able to achieve gross margins between 35% and 39%, which I find carries additional upside to EBITDA margins over the long term.

Improving gross profit margin (author)

Market and key trends

In the US market, Uber is the leader by a wide margin with a 76% market share, while the second-largest direct competitor in the US is Lyft (NASDAQ:LYFT) covering the remaining 24%.

Market share between Uber and Lyft (Bloomberg II scale)

However, the platform-based business model is largely dependent on critical scale because it requires a strong network effect to remain competitive. In my opinion, most of these markets are characterized by monopolistic tendency due to the strength of the network effect which usually leads to a strong moat and a “winner takes all” outcome.

However, despite this strong entry barrier, Uber faces other market risks. The main concern for investors has been the technological disruption caused by autonomous driving. Uber’s main competitors in the self-driving race are Waymo and Tesla (NASDAQ:TSLA). The most advanced is probably Waymo, a subsidiary of Google (NASDAQ:GOOG). Waymo already offers its own app where passengers can transport a fully self-driving car. According to their website, the company is active in 4 cities so far. While it is unclear today how this technology will impact Uber’s business model, investors are concerned about the potential for disruption. Uber will therefore have to stay on top of these developments and constantly reinvent its business model to match the autonomous driving trend.

However, I think there are some arguments that speak against the potential disruption of Uber’s business model:

- Autonomous driving is still in its infancy. This technology is still very new, and according to experts, it will take centuries for widespread adoption. There are still many technological, legal and regulatory hurdles that need to be resolved. As such, Uber will have plenty of time to adapt its business model accordingly.

- Uber is involved as a technology leader in this same field It ran its own self-driving vehicle business before selling it to Aurora in 2020. Despite the divestment, Uber still owns a significant stake in Aurora and has a close partnership that allows it to benefit from Aurora’s technology without taking on the full development risk. As CEO of Uber, Dara Khosrowsky is a member of Aurora’s board of directors.

- I see limited ability to scale At the same pace as Uber given the asset-heavy nature of autonomous vehicle manufacturing and the strong moat of Uber’s existing platform. In my opinion, the leaders of self-driving (Waymo or Tesla) are more likely to become software companies that sell self-driving technology, which would be a much more attractive business. As such, I believe it is a scenario where asset owners (self-driving vehicle owners) will replace existing drivers on the Uber platform to leverage their assets. The assets are likely to be manufactured by traditional auto OEMs that buy technology from companies like Waymo or Tesla.

- Uber’s business is becoming increasingly more complex and diverse. Uber has also added a delivery and shipping business, which not only makes it less reliant on its mobility business (which has especially helped during the coronavirus with food deliveries booming) but also becomes more complex and therefore more challenging for a leader in self-driving technology. To repeat. And compete with.

As I explained in the financials section of this article, Uber’s profit and loss is based largely on its cost of goods sold, which mostly includes driver commissions that are deducted from the price of the trip paid by customers. However, I believe that in the future where self-driving vehicles roam the streets, the driver will likely be replaced by the car owner. While the owner still expects a share of the price, staff costs for the driver cease to exist which ultimately lowers the cost per mile. Therefore, management explains that lower fare costs will lead to more consumers and increased participation as you can see in the slide below:

Impact of AV on Uber’s TAM (Uber 2024 Investor Update)

Valuation and expected return

Uber is currently valued at a multiple of 3.7x EV/Sales (TTM). Looking at their closest industry peers like Grab (4.3x), Lyft (1.3x), DoorDash (4.5x), and Instacart (2.2x), we get an average valuation of 3.2x.

Peer analysis (author)

Based on these multiples, it’s fair to say that a reasonable valuation for the industry would range from 2.0x EV/sales (minimum) to 5.0x EV/sales (maximum).

As such, I create a straightforward sales forecast that conservatively assumes lower future growth rates and calculates a potential stock price based on the EV/sales range presented (the analysis also takes into account the $7B announced share buyback):

Stock price forecasts (author)

Assuming a conservative 10% CAGR of 23-28 and an EV/sales multiple that fluctuates from 2.0x – 5.0x EV/sales, the expected 5-year return bandwidth ranges from (1.9%) to 17.9% per year. However, it should be noted that the stock price could also be volatile and fall to $42.9 if the EV/sales ratio declines to 2.0x by the end of 2023.

Investment risks

Although I have articulated mostly positive reasons in favor of investing in Uber, there are also some risks to my investment thesis.

In the analysis above, I assumed constant EV/sales margins to forecast the company’s stock price in the future. As such, there is a risk that the EV/overall sales multiple will fall below the expected range of 2x-5x EV/sales, which could subsequently result in a lower return to investors. However, I see this risk as mitigated by the fact that Uber’s EV/sales ratio has historically never fallen significantly below 2.0x but has increased significantly above 5.0x as you can see in the chart below:

Historical sales/EV chart (Searching for Alpha)

Another risk to the investment thesis is that self-driving technology will be more disruptive to Uber’s business model than expected. However, for the reason explained above, I do not expect this to be the case.

Finally, I see there is a certain risk that management’s expectations of adding the shipping business model do not pan out as expected. As sales of the Shipping business unit continued to decline in the first quarter of 2024, I have some concerns about the current integration of the business unit.

Conclusion

Uber has come a long way and has proven its ability to grow and operate profitably. I believe Uber is well positioned in the current market environment and that the self-driving trend could lead to lower fare prices and ultimately higher engagement and more consumers.

In terms of valuation, I believe Uber is currently fairly valued within its peer group with a valuation that may offer some room for upside given the company’s historical EV/sales multiple. I expect investors to be able to achieve an expected return of more than 10% over the next five years, with volatility within the bandwidth presented in my analysis above.

However, given the stock’s current downward trajectory, I recommend waiting for a trend reversal before buying into the stock, thus initiating a hold recommendation for the stock.