Kirpal Conner

Shares of UDR, Inc. (New York Stock Exchange: UDR) has performed poorly over the past year as higher interest rates weighed on real estate stocks. The cooling in the apartment rental market also weighed on stocks. behind In January, I rated UDR a ‘Hold’, as I felt its dividend was safe but its reliance on ‘B’ quality characteristics limited the upside. Since that recommendation, shares have underperformed, returning 4% versus the market’s 12% rise. We are seeing signs that the rental market has bottomed out, which makes me increasingly more positive on UDR, although I maintain my Hold rating.

Seeking alpha

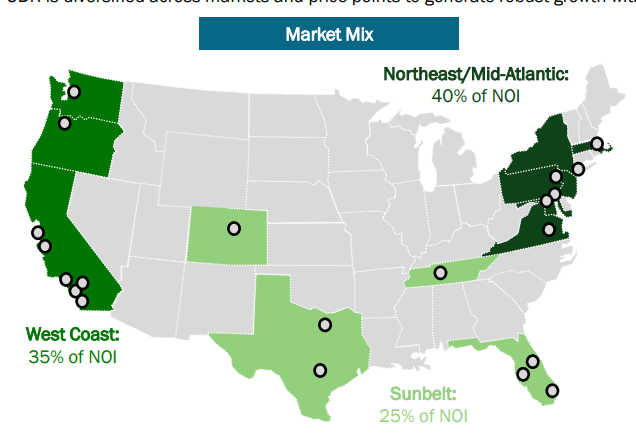

UDR is a diversified multifamily owner. The majority of its business focuses on vintage markets on the Northeast and West Coast. These markets like New York and San Francisco saw less new construction, but they were also less favorable Population dynamics compared to the Sunbelt, which is growing more quickly but also has more new supply. UDR’s focus on average quality has also been a concern for me. 56% of its properties are Type B; 53% in coastal markets and 66% in the Sun Belt. These properties may face more challenges from new supply in a higher vacancy environment. 69% of its area is located in the suburbs. The average age of residents is 36 and the household income is $162,000; 158% of the market average, although this average is somewhat inflated by its average of $372,000 in New York.

UDR

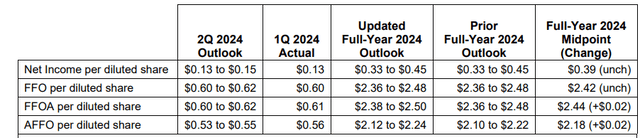

Entering the year, it expected the company to grow same-store revenue less than 2%, resulting in $2.40-$2.50 in FFO. This was based on my view that we are likely to see modest rental growth, with greater emphasis in the back half of the year, as the market has seen oversupply. Based on Q1 results as well as the company’s June investor update, I see UDR performing in line with these expectations, with FFO likely in the upper half of my original range.

In the company’s first quarter reported on April 30, the company generated $0.61 cash from operations (FFO), in line with guidance and up 2% from a year ago. Same-store revenue growth was up 3%, but expenses were up 7.5%. As such, net operating income was up just 1.2%, though it was up 2.7% excluding the one-time tax credit last year. There was a 13% rise in operating and maintenance costs, although property tax bills are now stable, which should slow future expense growth. Sequentially, NOI fell 1.6%, as the rental market was weak in a seasonally quiet Q1 period.

In the first quarter, the occupancy rate increased to 97.1% from 96.9% in the fourth quarter, which is encouraging. Mixed rental growth in the first quarter was up 0.8% from a year ago, which is a very modest rate. However, this is an improvement from the 0.5% decline in the fourth quarter. We are also seeing several notable differences. First, new leases fell by 2.5% while renewals rose by 3.8%. With rents rising so rapidly in 2020-2022, rents for existing tenants are often below current market levels, and UDR has been able to continue increases here. Importantly, even with this increase, its sales were down 300 basis points from a year ago, suggesting its rents are still relatively attractive.

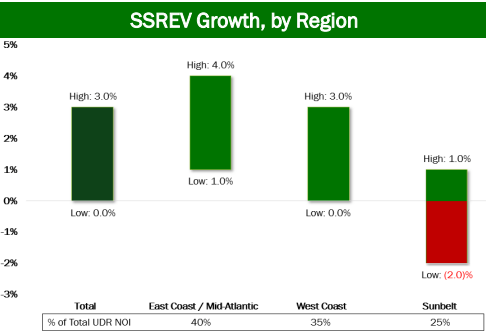

We are also seeing a significant shift between geographies. In the Mid-Atlantic region, revenue growth was 4.4% while it was only 1.5% in the Sun Belt. A lot of this has to do with the levels of supply that reach the market. There has been a spike in construction as Sun Belt rents soared post-coronavirus, and that supply is now hitting the market. Conversely, California and New York saw weak rent growth after the pandemic initially, resulting in weak construction and a lack of new supply today. According to UDR estimates, Sun Belt new construction levels are above historical levels while New York and most California markets are in line with history. As you can see, UDR expects this geographic dispersion in performance to continue.

UDR

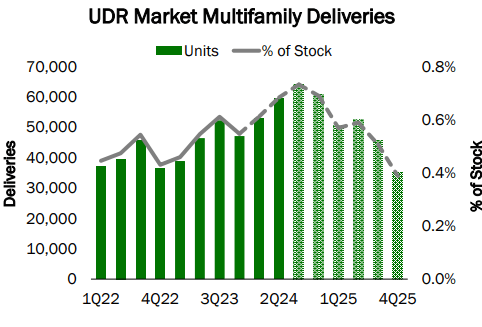

I expect older coastal markets to outperform the Sun Belt in 2024, which is a positive for companies like UDR and AvalonBay Communities, Inc. (AVB) which focuses on ancient areas. However, in the long term, I believe that favorable migration trends to the Sun Belt should support higher rents and allow new supply to be absorbed. I view the current weakness as a supply-driven cyclical decline amid a secular recovery. I would also note that during Q2/Q3, we should see a new peak in supply across the UDR portfolio with some players positioned in the Sun Belt seeing a peak a little later in Q3/Q4.

UDR

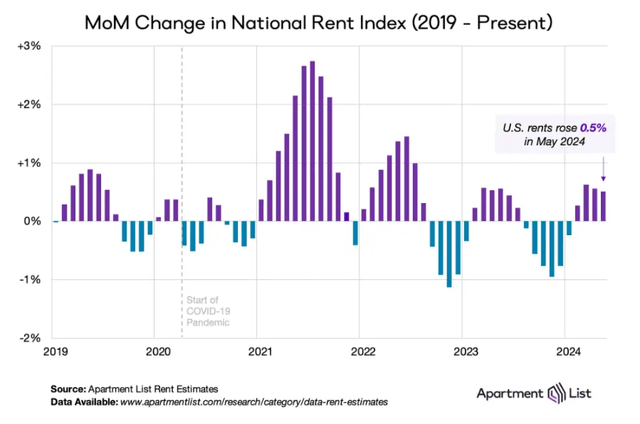

Lower supply should help provide support to rental prices, especially as employment continues to be strong and wages rise. This is indeed what we seem to see. In its June investor update, UDR reported an encouraging acceleration in blended rental growth to 3% in May, although occupancy fell slightly to 96.9%. Blended rent growth represented a 220 basis points acceleration from Q1 levels, and May’s result of 3% was up from 2% in April. Of course, monthly data can be volatile, but it is encouraging. It also corresponds to the peak of the display. Furthermore, the combination of rising rates and rising housing prices has worsened housing affordability, meaning some potential homebuyers may have to remain renters longer. This additional rental demand could support rentals, and what the UDR reported at QTD is similar to what Invitation Homes Inc. reported. (INVH), although the single-family rental market is somewhat different than multifamily rentals in my view.

At a higher level, ApartmentList’s national data also shows rents rising month-on-month, although they are still slightly lower than they were a year ago. UDR has been able to outperform national rental indexes over the past year, thanks to its focus on the Northeast and West Coast.

List of apartments

Along with the first-quarter results, UDR raised its full-year guidance slightly, raising FFOA by $0.02 to $2.36-$2.48. With the improvement we are seeing in Q2 data so far, I expect to see UDR results towards the higher end of guidance. I expect to see sequential improvements in results in the second half as the supply backdrop continues to improve, which should enable continued rental growth. I’m looking at $2.45-$2.50 worth of money from operations as a result.

UDR

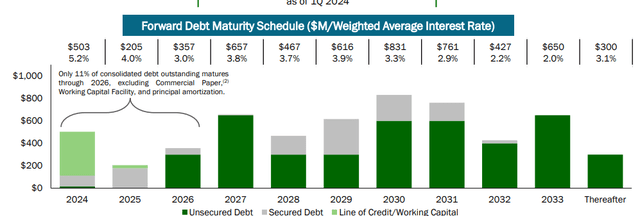

Finally, I’d also like to point out that UDR has a good balance sheet. It carries $5.8 billion in debt with an average term of 5.4 years. This leaves it with 5.7x EBITDA leverage. Due to higher revenues, interest expenses rose 10% to $48 million compared to last year. They have modest near-term maturities. However, as debt costs decline, and as debt is refinanced, we will see continued increases in interest expenses, although they should slow from the increase seen last year.

UDR

Overall, UDR has been able to weather the oversupply fairly well, and its business is now seeing some improvement. UDR offers a dividend yield of 4.3%, which I consider very safe, given its 1.5x coverage. Now, it has about $0.26 of recurring capital needs, and given that, it has a potential distributable return of about 5.5%. Given the structurally supply-constrained US housing market, I expect rent to outperform inflation over time, rising by about 3%, providing a potential return of about 8.5%, which I consider “market-like” and consistent with a hold rating.

Looking at relative valuation, UDR trades at around 16.2x FFO while Mid-America Apartment Communities, Inc. (MAA) is at 15x, and AvalonBay is at 18x. AVB has very high quality characteristics, and like UDR has a focus on the vintage market; Given its premium assets, I expect the premium multiple to the UDR to continue. The MAA has much greater exposure to the Sun Belt, which has been unfavorable over the past year. However, when investing, it is important to be forward-looking. UDR rents outperformed the national index because they were in a group of markets with lower supply. Since they are not as affected by the rise in supply as a company like MAA, they will not see much benefit from the supply going back down. There are some benefits given the 25% sunbelt exposure of course, and we’re seeing that in the results.

However, if we see the rental market rise, as I believe it will, investors will likely see the best returns in those with more exposure to supply, such as MAA, especially as these supply concerns have pushed valuation into a discount to the UDR. Rising rents will still help UDR, and I see it generating returns of up to 8% for investors, but that still leaves the stock a ‘hold’. Its lack of Sunbelt exposure will likely limit share price appreciation as the rental market recovers, and as such I see greater upside potential in companies like MAA, or incidentally INVH. I will exit the UDR as a result.