UiPath (New York Stock Exchange: Track) shocked investors with a remarkably poor outlook for fiscal 2025. To be clear, as we headed into this earnings report, I was bullish on PATH.

However, I know from experience that There is no point in compounding a bad investment decision, through sunk cost biases, with another bad investment decision.

In fact, I believe that the only way to outperform the market is by being honest and admitting your mistakes. Everyone makes investment decisions. But the amateur blames others, and the professional blames himself and works to correct his bad decision.

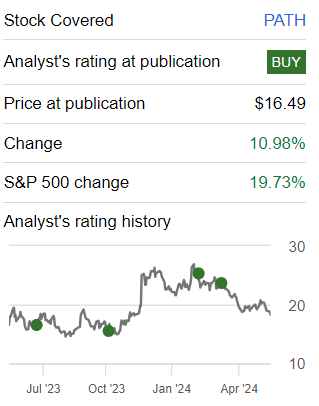

As it stands now, including the 30% pre-market sell-off, PATH is priced at 50x forward operating earnings. A completely unjustified premium for what it offers investors.

Quick recap

I said in my previous article

(…) After a difficult few years, UiPath changes its outlook, and at the moment, the stock is attractively valued.

The author worked on PATH

In hindsight, this turns out to have been a lie. UiPath has managed to put together a compelling story and convince several prominent investors of its strong market position. But unfortunately, apart from the engaging narrative, there wasn’t enough to support her assessment.

UiPath’s near-term prospects

UiPath creates software to help businesses automate repetitive tasks. This is the playground.

Think of it as a digital assistant that can handle routine chores, like data entry. UiPath, often called a “robot” or “robot,” can do these mundane tasks quickly and accurately. This helps customers save time, reduce errors and allow employees to focus on more important work.

Now, beyond the narrative, the reality has become a little less convincing. The departure of UiPath CEO Rob Enslin brings untimely uncertainty during this critical period.

Additionally, UiPath described a challenging environment with slower deal closings and increased scrutiny on multi-year contracts, particularly impacting mid-market clients.

Inconsistent execution, including contract challenges and changes in sales compensation, changed its forecasts significantly from 90 days ago.

So, given this context, let’s now delve into its financials.

UiPath directives surprise negative

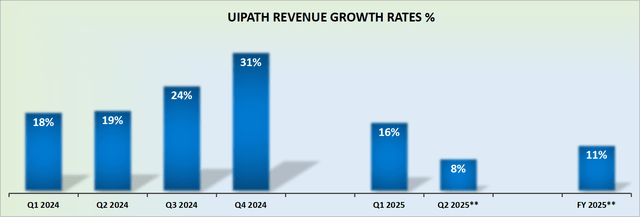

PATH revenue growth rates

We can forgive a lot about growing companies. In fact, a lot of colorful CEO stories can be bought provided the company continues to experience strong growth. Basically, a growing company must achieve strong growth.

What a growing company should not do, under any circumstances, is back away from its guidance. This, my fellow readers, is a grave sin that cannot be forgiven. And this is the sin that UiPath committed.

Not only that, but do we have to revise the company’s full-year guidance downward just 90 days after the previous result, by at least 1,000 basis points approximately at the midpoint of the range? Oh my goodness, this leads to a complete and utter loss of trust in the company’s colorful stories. And besides, the premium that investors are willing to pay.

Including the 30% pre-market decline, PATH is priced at 50 times forward operating earnings.

For a while, Thesis was one of the companies that could be counted on to re-accelerate their business line, along with a rapid improvement in profitability.

More specifically, UiPath was supposed to grow its non-GAAP operating profit from $233 million last year to nearly $300 million this fiscal year. And now?

Now, not only will there not be any increase in profitability, but profitability is expected to shrink by 35% year over year.

Given this context, are investors really more likely to pay 50 times non-GAAP operating earnings? Obviously not.

Bottom line

In conclusion, UiPath has taken investors on a wild ride with a bleak outlook for fiscal 2025, triggering a major pre-market sell-off and raising serious doubts about its valuation.

Initially, the promise of UiPath’s automation solutions convinced many prominent investors of its potential. However, the departure of its CEO and the difficult economic environment have exposed cracks in the narrative, leading to slow deal closings and inconsistent execution.

The company’s radical revision of its full-year guidance, just 90 days after its previous forecast, has shattered investor confidence and highlighted the cardinal sin of growth companies: falling behind on guidance.

As investors reassess the valuation of forward operating earnings by 50 times, it’s clear that UiPath’s once alluring story has taken a turn for the worse. In the unforgiving world of investments, failure to achieve growth is a sin that is too terrible to forgive.