Mesut Dogan/iStock Editorial via Getty Images

Investment thesis

I started a position at Unilever PLC (New York Stock Exchange: First) in February 2021 at a share price that I believe offers a compelling valuation and strong dividend yield. Three years later, the stock price rose It rose 18%, and dividends received contributed another 12%. I believe a 10% CAGR is a reasonable rate of return for a slow-growing core consumer business that contributes to a diversified portfolio. The aim of this article is to evaluate Unilever’s ongoing performance status and future outlook for shareholder return.

introduction

Unilever PLC (UL): The household staples business remains fairly valued after the recent share price increase. The exit from the ice cream business is expected to strengthen the balance sheet through a spin-off, which the board has decided to do The best option at this time. The liquidation process is expected to be completed before the end of 2025.

After divestment in ice cream, Unilever will focus on the following four areas:

-

Beauty and luxury.

-

Personal care.

-

Home care.

-

feed.

Unilever’s latest trading report provides an update on the business and its €800m cost saving programme, which is expected to impact 7,500 employees over the next three years. The divestment in the ice cream business is expected to be completed by the end of 2025.

A three-year internal reorganization and business separation programme, amid ongoing inflationary pressures, is likely to create short-term headwinds for Unilever’s share price, particularly as the restructuring is estimated to cost 1.2% of the group’s revenue per annum for each of the businesses. . Next 3 years.

commercial activities

The divestment in ice cream will reduce the group’s revenue by $7.9 billion, however, on the upside, I expect debt repayment to form part of this divestment.

Additional divestments already completed include the disposals of Elida Beauty, Dollar Shave Club and Suave in North America, which were identified as non-essential products.

The recent acquisitions of Yasso, a premium Greek frozen yogurt maker in the US, and premium hair care brand K18, will reduce the impact of the spin-off of the ice cream business.

The latest earnings confirm that market share across the business units has remained stable, and this stability comes at a time of rising product prices, which consumers appear to be absorbing with minimal impact on volumes.

Over the past decade, Unilever’s operating areas have been reorganized from three units (Home Care, Food & Refreshment, and Beauty & Personal Care) to five units, including the ice cream business. Unilever’s proposed reorganization will create four separate business areas: beauty and well-being, personal care, home care and nutrition. Within these units, 30 energy products have been identified to improve growth.

UL product areas (Unilever charts)

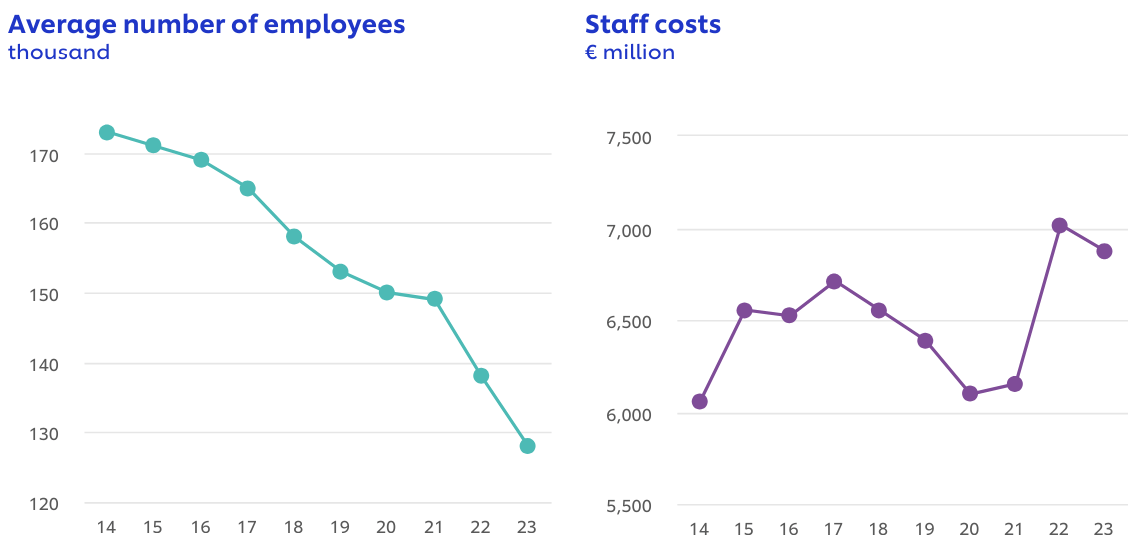

The news of up to 7,500 employees being affected by the ongoing restructuring struck me as fairly significant given the decline in headcount over the past 10 years, and digging deeper, I investigated staff costs, which have been rising rapidly in recent years. Reducing staff made sense given the lack of growth in many areas of the business.

UL Recruitment Costs (Unilever Investor Relations)

Shareholder returns

Unilever announced the commencement of a €1.5 billion buyback license from May 17 with the first tranche of €850 million, which is expected to be completed by the end of August 2024. Although €1.5 billion is a large amount, it represents only Just a big amount. 1.2% of the market value. I believe this buyback will reduce the impact of restructuring costs, but it may not be enough to support the stock price during the restructuring program.

Stock buybacks have long been used to return excess cash to shareholders; However, dividends are the bulk of shareholder returns, with no withholding tax on UK listed shares, which can be beneficial depending on the tax circumstances. Earnings growth has been disappointing in recent years; However, management recently reaffirmed its intention to continue rewarding shareholders through dividends.

Earnings Growth (Looking for Alpha Charts)

religion

Unilever’s stable credit rating was unchanged, with Standard & Poor’s at A+ and Moody’s at A1. Being one of the top listed companies in Europe, this has enabled UL to obtain debt at very reasonable rates, ranging from 0.5% to 3.5%. I think there’s not much to worry about for investors from a debt perspective. Repayments are well thought out, and interest rates are expected to fall in the not too distant future.

Debt maturity (author, data from Unilever IR)

Prospects

Unilever’s latest trading update is promising for shareholders; Sales growth of 3-5% is expected for 2024. The restructuring program is expected to improve productivity, enabling gross margin improvement and savings of €800 million across the business.

Trading forecast for 2024 (UL Q1 trading statement)

Unilever plans to simplify the business and focus on its core brands, which have a strong position in their category, and these core brands currently account for 75% of revenue. The divestment in the ice cream business is expected to be a net positive for the growth of both the ice cream business and Unilever.

With cash accumulating on the balance sheet, I believe a potential use of this excess cash flow would be additional stock buyback announcements. Dividends covered by cash flow are expected to continue to grow in the low single digits.

Peer comparison

If I were to buy now either UL or PG which one should I choose? The comparison between Unilever and Procter & Gamble (PG) provides a useful benchmark when determining the decision to invest in UL. P&G has set the standard in terms of share price growth, which, combined with growing dividends and share buybacks, means that P&G shareholders have outperformed Unilever by a large margin.

Taking a closer look at similar financials, it is clear that PG is the more stable and consistent business. PG’s revenues are approximately 25% higher than UL, with stronger operating income. Cash and debt comparisons are stronger for PG; However, I think UL is in a good position with respect to cash and debt. As shown in the chart below, across all operating metrics, PG is outperforming UL, which goes some way to explaining why PG’s share price has performed so strongly. On the other hand, this outperformance means that the shares are now trading at a forward P/E of 25x. So, to answer the question, at the current valuation, I don’t favor PG over UL, because I think the valuation is an issue for both companies.

Peer comparison metrics (author, date from SA)

evaluation

Evaluation is one area where PG does no better than UL evaluation. I think UL is slightly more attractive than PG, however, recent share price increases have reduced the margin of safety.

-

Unilever’s P/E is 20x, which is higher than the five-year average of 18.7x and higher than the industry average of 17.4x.

-

Unilever’s P/B ratio supports my valuation thesis, as a forward P/B of 7.15 suggests little value to investors at the current share price.

-

The forward PEG ratio of 3.07 indicates a possible overvaluation at current prices.

Additionally, Seeking Alpha’s Quant Rating is currently a C- Rating, further supporting the valuation metrics.

Evaluation Ranking (SA Quant)

Risks

Economic Recession – Consumer staples tend to be more resilient than most sectors in times of recession. However, consumer purchasing power remains key for UL, especially with discount brand products available in store. Higher interest rates are expected to create headwinds for consumer spending; However, experience from previous economic cycles suggests that when interest rates start to fall, household balance sheets start to strengthen and consumer sentiment starts to turn more positive.

Efficiency Program – The ongoing divestment process in the ice cream industry remains uncertain; Spin-off appears to be the preferred method of divestment; However, no details have been revealed publicly. This represents a potential risk if divestment is not implemented. In addition, the efficiency program and upcoming layoffs pose a risk when workloads are redistributed. A 3-year cost impact of 1.2% across the business is hurting the financials. Focusing efforts on growing the 30 strong brands may result in a lack of interest in the remaining business products. I think it will be important to monitor the efficiency program for any indication of deterioration in older non-energy branded products.

Conclusion

Unilever has made the difficult decision to divest its ice cream business, as part of efforts to streamline its remaining business units, while targeting key product areas referred to as strong brands for future growth. These 30 strong brands represent 75% of revenue, making the decision to focus on these brands understandable. I think it will take some time for the company to reorganize before we see improvements in the financials. The three-year duration of the reorganization is likely to impact free cash flow. The ice cream business is expected to be spun off before the end of 2025, which is longer than I expected. There is no reason, however, for any assets to be sold at a bargain price. , the two years from announcement to divestment are longer than expected.

For existing shareholders, it seems prudent to retain the position and monitor the progress of the efficiency program. Shares are trading above recent lows with a forward P/E of 20x, leaving little room before they become overvalued. Since the guidance is for 3-5% growth this year and a similar future outlook, I think a P/E ratio of 20x leaves no margin for safety.

While I have some concerns about where Unilever’s share price will head over the coming years of restructuring, I see no reason to sell this consumer staple. I expect UL stock to continue to underperform compared to its peers, which means those looking for alpha should consider alternatives. In summary, my investment thesis remains unchanged, and I believe divestment in the ice cream business will be a net positive, allowing full focus on growth of the reorganized core business. The recent increase in the share price has removed the margin of safety and I think the valuation is unattractive. I rate Unilever shares as Hold pending further progress on the restructuring programme.