Monty Racusin

Investment thesis

With the investment world getting so excited about AI-driven stocks, I think I’ve found Unisys Corporation (New York Stock Exchange: International User Interface) to be a beneficiary of an AI-led growth story as the company delivers what seems to me very Innovative AI solutions to help customers do business more efficiently. With stable recurring revenue of about $2 billion, I ultimately believe the company can be profitable on a GAAP basis due to efficiency gains and lower SGA expenses in the future. Cash flows are still relatively strong and I think investors should consider buying this stock at its current cheap valuation.

Company overview

Unisys Corporation is “a global technology solutions company dedicated to driving progress for the world’s leading organizations,” according to its website. As a technology company, it comes up with innovative solutions that help customers run their businesses Workplace, digital cloud, and cybersecurity infrastructure. they Annual Report “We provide our global clients with advice and essential capabilities to design, develop, modernize, implement and integrate technologies that support their organizations,” he says.

The company declares its operations in three segments: Digital Workplace Solutions, Cloud Applications and Infrastructure Solutions, and Enterprise Computing Solutions. These solutions enable their customers to automate and streamline business processes for overall efficiency. The Unisys product portfolio includes solutions centered around data analytics, cybersecurity, cloud management, and more.

I believe that more and more companies are looking to use AI to enhance business efficiency and that Unisys products have a high potential to generate recurring revenue. Investors can see that sales have been around $2 billion annually since 2020, and have stayed there for the past few years. This indicates to me that the products are of high value and have a strong consistency with customers continually relying on them to support their business.

The company recently announced that it is “evolving its AI strategy,” naming Brett Barton as global AI practice leader according to this press release. This suggests to me that AI will be the primary focus that management will leverage to make their products technologically competitive in the market. Many of its solutions have won awards, demonstrating the great value customers get with Unisys’ digital workplace solutions.

In conclusion, I see this technology company as being very competitive in the market by offering AI-based products that help automate many of its clients’ business processes surrounding data, cloud management, cybersecurity, and other IT functions. With recurring revenue generated by the strong close, I believe the top line will remain steady while bottom line strengthens as the company reduces SGA expenses over time, resulting in significant dividends for shareholders.

New business indicates growing momentum

The company announced this in its latest quarterly earnings report

Unisys’ first-quarter results indicate growing market recognition of the transformation we have achieved within our solutions and services portfolio, which can be seen in the momentum of our new logo signings more than doubling year-over-year.

The new logo signatures are defined in the press release as follows:

Represents estimated revenue related to contracts signed in the period without regard to cancellation terms. New Business TCV represents TCV which is attributed to expansion and new scope for existing clients and new logo contracts.

Signing on new customers indicates that the company’s products are attractive, incredibly innovative, and relatively easy to sell. What this means to me is that sales should increase year over year because the company is not just relying on existing customers for sales anymore. It is also likely that their reputation across the industry will improve which may allow the company to build better knowledge around improving customer workflows and gathering valuable data and insights to enhance its product portfolio.

I think management has prepared for the additional business to come as they see the total contract value of their new logo doubling year over year, which explains why their operating income has improved, from $52.2 million in 2022 to $76.9 million in 2023 which represents a 47% increase. . I expect operating profits to continue to grow, perhaps reaching $100 million by 2025 or so as the company gains momentum by doubling down on new logo signings.

Cash flows remain strong, rising from $12.8 million in Q1 2023 to $23.8 million in Q1 2024, an increase of nearly 100%. This is a signal that I think investors should pay attention to because it shows that free cash is starting to flow, giving management additional flexibility in being able to grow their business. I expect cash flows to remain relatively strong as the company expects a very healthy backlog of $2.78 billion for the first quarter of 2024, enough to give investors steady sales coming in for at least next year. Overall, I’m happy with the momentum this company is gaining in terms of improving its product portfolio, gaining new business, and improving its reputation in the industry.

Customized AI solutions are attractive

Going forward, I believe the company’s customized AI solutions will drive sales as demand for these services is likely to be strong, as companies try to streamline processes, automate workflows and take their cloud and data analytics to the next level. According to the company’s brochure on its website which covers a specific case study of a typical client,

Through close collaboration with Unisys, the organization has set a strong path towards a future of improved operations. They achieve a low total cost of ownership and accelerate time to market.

Through this partnership, the organization unlocks greater value from previous technology investments and enhances flexibility and modularity, thus becoming a more adaptable and responsive organization.

To me, it seems like Unisys is looking to understand their customers’ operations from head to toe to completely revamp their entire IT systems and processes. This personalized approach is likely to be attractive and attract customers because Unisys is willing to modernize and migrate applications to improve performance, enhance security, and potentially reduce costs in the long term. I believe this service is highly valuable in today’s economy where many are trying to gain a competitive advantage in operational efficiency, so modernizing and moving their IT systems to a better place is essential to compete effectively in my opinion.

I believe reputation is very important in the world of IT consulting, and Unisys has a proven track record of success in designing custom solutions that work well. The company continues to win numerous awards, such as being the “Overall Market Leader by NelsonHall Seller Evaluation and Rating Tool.” Based on this track record, I believe their reputation has been a key driver of their success in customer acquisition and retention, which explains why their revenue and backlog continue to perform so well.

Valuation – Fair value $7

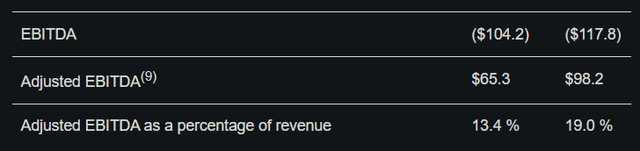

I believe sales will remain at around $2 billion for the foreseeable future, as I think sales appear to be flat, and I will use this higher number as a starting point for my assessment. Assuming an adjusted EBITDA margin of 10%, compared to the current quarter’s adjusted EBITDA margin of 13.4%, I see adjusted EBITDA of 200 million Dollars annually. I chose 10% because it is conservatively lower than the current quarter’s rate. EBITDA margin.

Find Alpha’s earnings for the first quarter of 2024

Adjective application. An EBITDA multiple of 9x, which is below the sector average of 14x, gives me an EV of $1.8 billion. I’m using adjusted numbers here because I believe they correctly reflect the company’s true profitability, because they “do not include pensions and post-retirement expenses.” However, to account for the large difference between EBITDA and adj. EBITDA, I think using a lower multiple in Adj. Earnings before interest, taxes, depreciation, and amortization (EBITDA) are better suited to account for this discrepancy.

Then, to account for the fact that I’ve excluded retirement and post-retirement expenses, I’ll account for these liabilities by subtracting debt and retirement benefits ($1.26 billion) from the EV of $1.8 billion. Subtracting $1.8 billion by $1.26 billion gives me a market value of $540 million. Dividing by the 70 million shares outstanding gets you $7 fair value, rounded down.

I believe the stock price is undervalued and it is not necessary to do a careful calculation to see the trade. Sales of $2 billion with a market capitalization of less than $300 million are considered very cheap, and the company is trading much lower than it was at the height of the pandemic in 2020. However, the company is arguably much stronger than it has been since 2020, and the stock It is somewhat less than that. I would argue that this mispricing is unjustified and that the market is missing the underlying strength and momentum of the company, which reinforces my belief that the stock is undervalued.

Risks

The company may lose its reputation and lose existing and new customers if they fail to continue providing innovative new AI-driven solutions. Competition in the industry is fairly fierce as many players join in to offer similar services at competitive prices.

Unisys itself could be targeted in a cybersecurity attack because it contains a lot of information about its customers’ operations. Management needs to be careful about maintaining the latest technology to defend its business from cyber attacks.

Catalysts are hard to find in this stock, so shares may be cheap for a while which could test investors’ patience. It seems to me that the market is missing this, but there is not much to accelerate the process of closing the valuation gap. It may take some time for investors to see returns in their portfolio as the company still reports net losses in EBITDA and GAAP, which may be unattractive to investors looking for straight-up earnings.

A company’s retirement plan may sometimes be underfunded, resulting in cash flow going to retirement benefit plans rather than to investors. The annual report indicates,

We estimate that cash contributions to U.S. defined benefit pension plans will begin to increase in 2025, increasing total estimated contributions to U.S. and non-U.S. defined benefit pension plans to about $110 million in 2025 and about $770 million $ in total as of 2026. Until 2033.

Although I took this into account in my assessment, increasing cash contributions to retirement plans can stress investors’ available free cash flow, presenting financial risks.

Buy Unisys

I think the market is completely off base here, with the company valued at less than $300 million in market cap when sales are over $2 billion. This write-down is very attractive because I believe the company’s numerous awards, track record of customizing innovative solutions, and new focus on artificial intelligence will likely result in increased shareholder value. Investors should consider purchasing Unisys if they love the IT consulting industry and want to have an award-winning market leader in their portfolio.