Editorial ricochet64/iStock via Getty Images

UPS shares (New York Stock Exchange: UBS) has been performing poorly since the post-coronavirus e-commerce bubble burst, and the company has been losing market share to Amazon (AMZN) at an accelerating pace at recent days. These situations may be difficult to time, but UPS still has a strong competitive position and is exposed to continued tailwinds of growth in e-commerce, which appears to have mostly normalized after the past few years of volatility. I share with you the reasons why I believe the overall picture could improve.

E-commerce tailwinds are still there

Retail e-commerce sales are expected to double by approximately 10% annually between 2024 and 2028. In the United States, the compound annual growth rate is expected to reach approximately 12%. Some of the more optimistic forecasts put the CAGR for 2024-2029 at around 16%. I think that remains a key driver for the industry, both in terms of growth Deliveries and parcel returns are increasing.

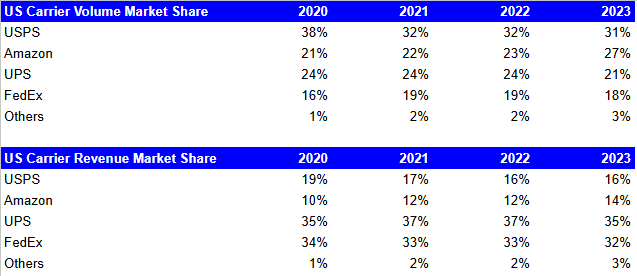

UPS, like FedEx and USPS, has lost market share to Amazon, and will likely continue to lose some. However, I think it’s highly unlikely that the world’s largest parcel delivery company won’t be able to somehow benefit from this positive structural growth in e-commerce. These are key tailwinds that could last a decade or more, and they don’t just affect Amazon. For example, Amazon’s share of US e-commerce may settle between 37 and 38%. This is the sector that Amazon has disrupted and which it dominates.

In my view, achieving a similar market share in logistics is more difficult. Established players like UPS have strong relationships with companies that may not want Amazon to dominate logistics as well as e-commerce. UPS and other more established peers also meet a wide range of delivery needs, including high-value items.

Amazon already boasts a whopping 27% market share in logistics now in terms of number of packages delivered, making it the second largest provider after USPS (31%), while announcing further network expansions. Amazon can certainly continue to gain market share by leveraging its dominant e-commerce position and global network, but market share gains don’t mean UPS can’t grow and thrive at a lower rate, making the current valuation a bargain.

Pitney Bowes, author

Since Amazon is also the top competitor for most retailers who may use it as a logistics provider, it is reasonable to assume that many retailers will be reluctant to rely on it fully.

For UPS specifically, there are a large number of large retailers that rely at least in part on its logistics services (along with Amazon), including Home Depot, Sephora, Lowes, Target, and eBay, to name a few. Big tech giants like Apple also rely a lot on UPS for shipping.

I think that for most retailers, Amazon’s market dominance where the company has massive contracting power is undesirable, and a balance of market share between the large logistics companies is probably the desired outcome. If Amazon’s market share growth slows, the bull case for the core business becomes relatively simple. A CAGR of 10-14%, in my opinion, is enough to allow the best players to flourish and grow without the need for a winner-take-all situation.

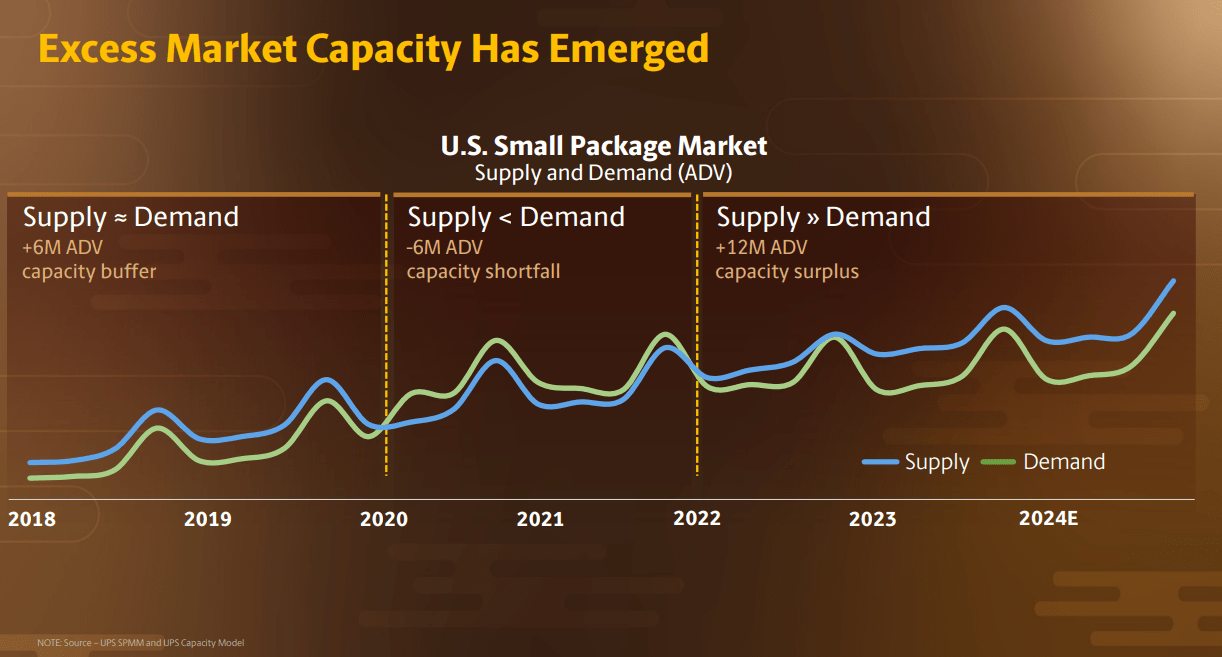

The problem of overcapacity is improving

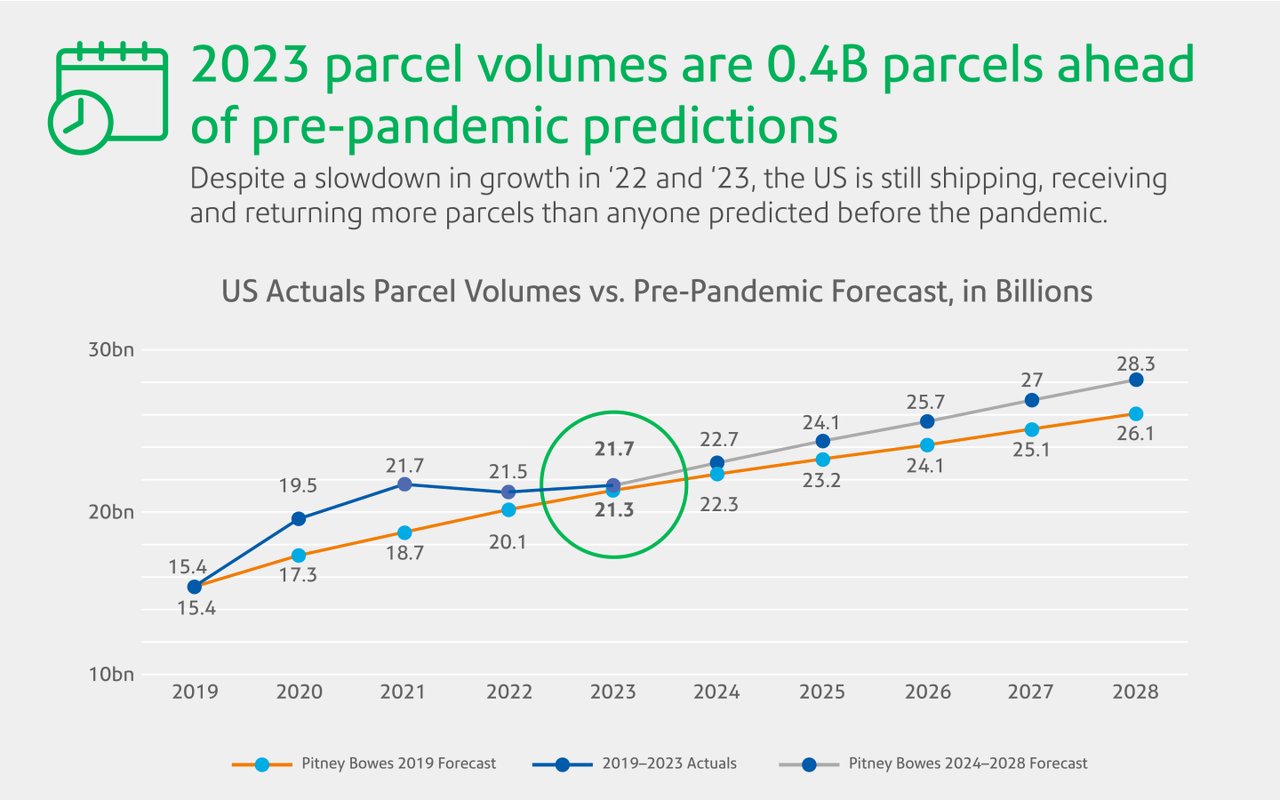

UPS has identified the problem of excess capacity, estimated at 12 million daily storage units in the U.S. small package market. This is a result of the lockdown-induced e-commerce growth that ended up falling after the reopening. The 10-14% CAGR that the e-commerce industry is experiencing is the structural driver that makes me certain that these overcapacity issues should gradually improve now that the demand trend appears to be normalizing. I say it looks like the market is back to normal because according to data from Pitney Bowes, actual package volumes in the US are now what we would expect had Covid not happened, suggesting that the industry is now poised to resume its structural growth trend.

Pitney Bowes

With the current U.S. small package market at between 84 million and 88 million packages per day, and assuming approximately 70% e-commerce, e-commerce growth will take less than a year and a half of 14% growth and approximately two years of 10% growth. Taking care of surplus capacity (assuming no further increases or very limited increases in capacity).

Reduction to full equilibrium may not be necessary. Even a reduction to a surplus of six million would return the market to a balance similar to 2018-2019.

UPS Investor Day

At that time, the company was able to achieve an operating margin of approximately 10%, in line with 2023 levels. 2023 margins were relatively good despite lower revenues and cost pressures, indicating that the company can still enjoy healthy profitability in A difficult year. Wage increases will begin in 2024 and may not pose persistent pressure if inflation remains at acceptable levels. Therefore, some margin expansion due to a lower supply/demand gap should help the company achieve its ~12% operating margin target for 2026.

Trends are expected to improve

2023 and the first quarter of 2024 have been difficult years on all fronts. Revenue guidance at Investor Day indicated a difficult first half, with revenues down 1-2% and operating profits down 20-30%, but pointed to a strong recovery in the second half, with revenues up 4-8% and operating profits up By 20-30%. .

Management shared a goal of generating $114 billion in revenue at an operating margin of more than 13% by 2026, which would mean $14.9 billion in adjusted operating income, with approximately $220 million in investment and other income, and interest expense of 700 $1 million and a tax rate of 21% means $11.4 billion in net income. At current market capitalization and assuming a fixed number of shares outstanding, this corresponds to a P/E ratio of less than 11x. If business takes place in the next three years, I view this as an attractive valuation, as UPS remains a strong, profitable, cash flow generating business with a strong market position and exposure to structural tailwinds despite losing market share.

If things don’t go well

I’ve mostly talked about traditional core businesses being exposed to e-commerce. I think we could see things improving as Amazon’s market share expands toward normal equilibrium and e-commerce growth returns to becoming a structural driver. There are still fundamental risks, and nothing guarantees that Amazon won’t become more aggressive.

However, even with continued pressure from Amazon in the next few years, there are potential mitigating factors. UPS Healthcare revenue is about $10 billion now (about 11% of total revenue, and more than a quarter of SCS’ revenue), but management’s goal is to double it by 2026. This is a higher-margin business with less competitive pressure from Amazon. (Even if it is not absent). Since half of revenue growth is expected to come from higher revenue per segment, I expect margins to expand further if management’s targets are met.

Regardless of what happens in the e-commerce exposed small package market, from a hybrid perspective, the top 10% of margin revenue will likely double in three years as margins expand further.

The valuation is considered much less risky, and is likely to be oversold

Even in a negative year like 2023, UPS was able to print over $5 billion in FCF. At its best in 2022, the company’s free cash flow was nearly $10 billion. A return to these levels would make it seem like a potential deal at 12x FCF, although that’s not expected to happen in the next few years due to the roughly $6 billion in annual capex.

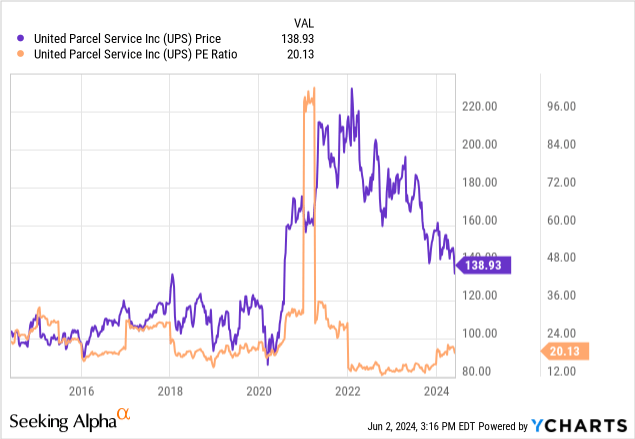

If we look at simple P/E ratios, which are currently around 20x, the current valuation suggests an attractive potential entry point. In the past 10 years, P/E ratios of 20x or lower have marked good entry points in 2016 and in 2019-2020.

Mid-term guidance shared at Investor Day was also bullish. Revenues of $111 billion (per the midpoint of the guidance range) by 2026 at an operating margin of 13% would mean $14.4 billion in operating income. With a conservative investment of approximately $220 million of investment and other income, interest expense of approximately $700 million and a tax rate of 21%, it provides approximately $11 billion in net income. At current market capitalization and assuming a fixed number of shares outstanding, this corresponds to a P/E ratio of less than 11x. If business takes place in the next three years, I view this as a potential deal, as UPS remains a strong, profitable, cash-flow generating company with a strong market position and exposure to structural tailwinds.

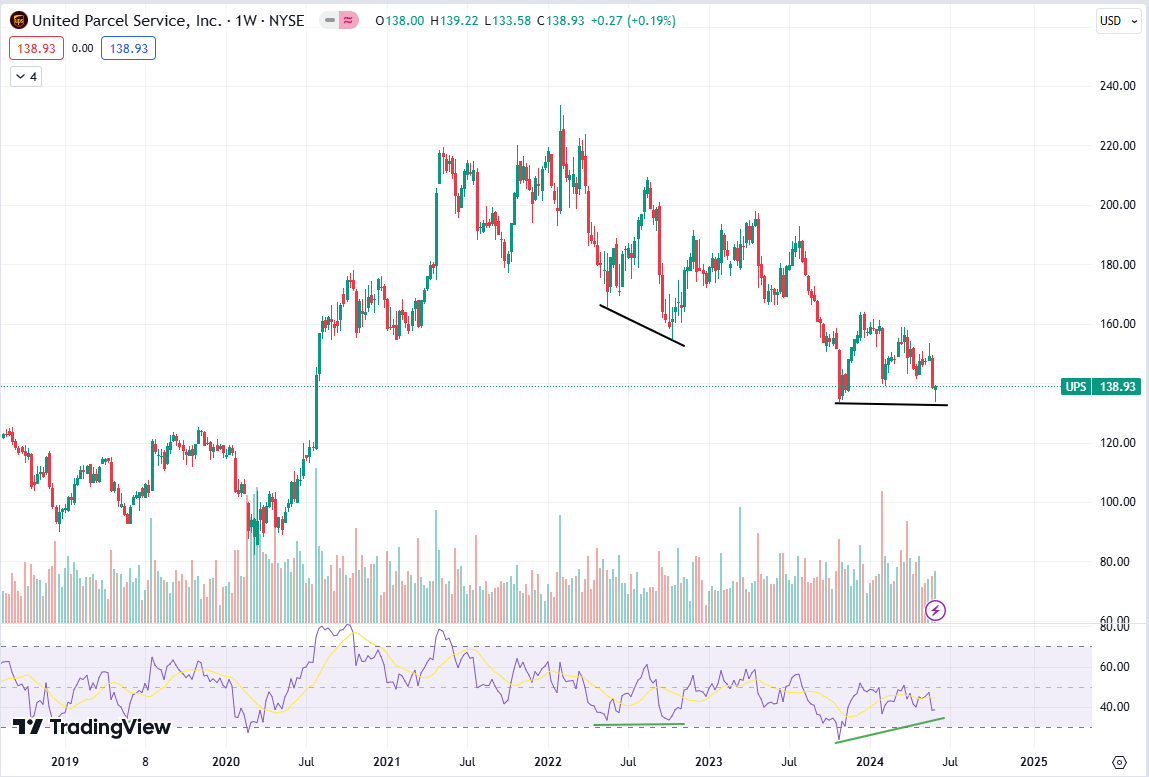

Possible double bottom?

The stock has been weak and technicals are approaching oversold territory again. Although it is not entirely clear, there is a possible double bottom forming on the weekly chart with a positive divergence on the RSI (14 weeks chart). This type of pattern has worked for UPS stock before (for example, from May to October 2022) and may offer another angle to suggest a constructive picture in the short term.

TradingView

Conclusion

UPS’ business is still under threat from Amazon’s growing market share, but I see a more positive picture emerging. Valuation is reaching attractive levels, while the e-commerce market returning to normal may see the small parcel market expand again. The positive mix effect is helped by growing high-margin healthcare revenues, and the valuation does not appear demanding, especially if achieved with execution on 2026 targets.

Improving financial trends for the rest of the year and a potentially constructive technical picture suggest that the risk-reward ratio has improved. I see UPS stock as a cautious buy here.