US Bancorp Shares: Gradual Improvement in Interest Margin (NIM) Ratio Could Boost Shares (NYSE:USB)

Diverse photography

Shares of American Bancorp (New York Stock Exchange:USB) had a strong performance over the past year as the bank benefited from the recovery from the regional banking crisis in early 2023. It also had positive regulatory results for Capital needs after the acquisition of the Union Bank branch. Given these tailwinds, I rate the stock a buy November. Since then, USB has returned 11%, which is a strong absolute return, but pales in comparison to the market’s 15% gain. Shares are also down about 10% from their recent highs, forcing me to reconsider my view. While his recovery at NIM is taking a little longer, I remain optimistic.

Seeking alpha

In the company’s first quarter, USB generated a profit of $0.90, and we saw earnings fall slightly short of my expectations as net interest margin (NIM) pressures persist longer, given the interest rates held by the Federal Reserve. with Inflation has proven more sticky than expected and the real economy is fairly resilient. I currently expect the Fed to cut interest rates once this year towards the end of the year, with limited impact on this year’s financials and keeping deposit costs high.

As I talked about in my coverage of regional banks, I believe that stable deposits are essential when investing in this sector, as deposits are the lifeblood of a bank’s finances. For US Bancorp, average deposits were down about 1.4% from a year ago, slightly better than the industry average, and were flat sequentially. I would point out that deposits at the end of the period jumped to $528 billion, but this was happy with the Easter event at the end of the quarter, which makes the average a better indicator of performance. Q1 can be more seasonally challenging as cash can be accumulated at the end of the year and then distributed at the beginning of the year, so I see sequential fixed deposits as a positive outcome.

US Bancorp

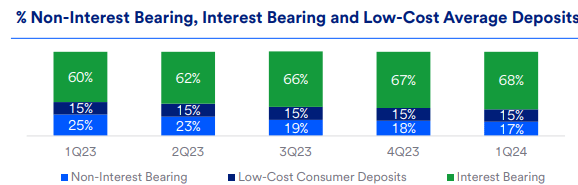

About 52% of deposits are retail, and similarly, 51% of deposits are insured, which is relatively low. Most uninsured balances work (i.e. payroll account), but uninsured deposits can be less sticky. As such, I find its resilient deposit performance particularly impressive, in keeping with its status as a safe haven bank. But with insured deposits declining, maintaining strong capital is crucial to maintaining depositor confidence, and as I will discuss in more detail below, USB has made tremendous capital progress over the past year.

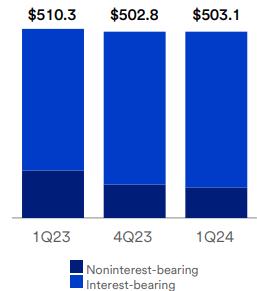

The biggest challenge facing the bank was the unfavorable shift in its deposit base. As you can see below, it has been steadily losing non-interest bearing balances (NIB) to interest bearing balances. High transaction accounts typically do not pay interest, and when rates are lower, customers allow additional cash to be deposited into these accounts. With interest rates remaining at more than 5%, there is a strong incentive to reduce cash balances here and move money into interest-bearing accounts. Since customers need to have enough cash in NIBs to meet their transaction needs, there should be minimum balances, but we are not there yet.

US Bancorp

Importantly, we are seeing some slowdown in this shift, because after a year of rising rates, clients have had plenty of time to adjust account balances, and USB’s share of NIBs is moving around 1%/quarter, representing a 3 basis point NIM headwind. almost . At a conference last week, management said it was seeing stability and slower movement from the National Investment Bank to interest-bearing deposits. It has taken a little longer to reach the bottom than expected, but we should reach the bottom of NIB balances before the end of the year in my view.

In addition, as interest rates remain higher for longer, the cost of interest-bearing obligations has risen, albeit at a slower pace. In the fourth quarter, the cost of interest-bearing liabilities increased by 10 basis points to 3.12%. Much of this reflects the implementation of a full quarter of rate increases during the fourth quarter of 2023. Going forward, management expects “stability” to the rate paid on deposits. This is somewhat consistent with the rhetoric we’ve heard from other banks, like Ally (ALLY). We are unlikely to see significant declines in deposit rates until the Fed cuts rates materially, but these headwinds should fade. As such, while some drift from NIB balances to BI balances may pressure net interest margin, incremental pressure on net interest margin relative to the liabilities side of the balance sheet should be limited from here.

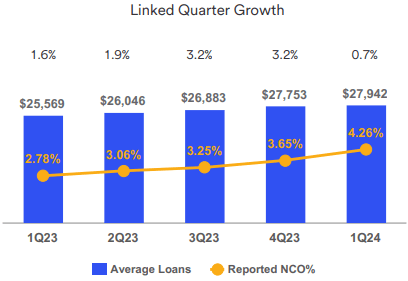

On the asset side, loan growth has been slow, due to weak demand from corporate borrowers given the pricing environment. Since new loan originations generally generate higher returns than the existing asset book, this has been a headwind. Last week, the administration reiterated its forecast for “modest” loan growth, focusing more on the consumer side than the business side. In the first quarter, average loans fell by $2 billion sequentially to $371 billion, due to lower demand from businesses.

Aside from loans, US Bancorp also has a large portfolio of fixed income securities. Since most assets have fixed interest rates and were bought when rates were lower, this has been a headwind for USB’s NIM, a headwind widely shared among regional banks. It has held this portfolio largely constant, at $162.4 billion. Just by reinvesting maturing securities at higher prevailing yields, this portfolio’s return rises by 7 basis points per quarter, and should continue to do so. It is now yielding 2.96% from 2.64% last year.

Due to weak loan growth and slow movement in the securities portfolio, the bank achieved a 5.25% gain on assets, an increase of 3 basis points from the fourth quarter, which is a smaller increase than what was seen in its liabilities. As such, the net interest margin was compressed to 2.70% from 2.78%. While I had thought that net interest margin might recover to 2.90% this year, this forecast now looks overly aggressive. However, we are expected to see liability cost headwinds decline towards 3 basis points in the quarter as interest-bearing costs stabilize and NIB flows slow. Meanwhile, assuming USB can return to modest loan growth, we should see asset yields rise by 6-10 basis points sequentially, which could push net interest margin to 2.80-2.85% by the end of the year. While net interest income declined by $127 million sequentially, I expect it to be broadly stable in the second quarter and then rise by about $200 million per quarter in the second half. This would leave the company on track to reach a maximum net interest income of between $16.1 and $16.4 billion.

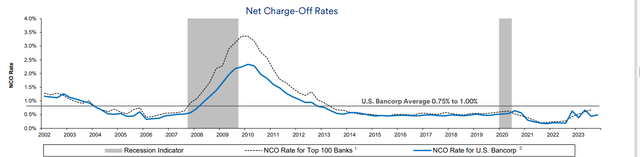

Of course, apart from NIM, credit quality is an important metric for any bank. Here, I still have strong confidence. As you can see below, USB has historically been a prudent lender with lower-than-industry losses during major recessions and industry-like losses during periods of strong credit quality (when defaults are so low, even companies with loose standards see limited losses, after all). Currently, only 0.08% of business loans are more than 90 days delinquent, demonstrating its conservative underwriting stance.

US Bancorp

USB combines strong credit performance during the cycle with strong booking. USB currently has $1.8 billion in non-performing assets and 0.48% of non-performing loans, up 8 basis points sequentially. In exchange, it holds reserves worth $7.9 billion, providing more than 4x coverage. I see roughly 2.5x coverage as a measure of hard reserves, so USB has a big cushion here. It could see non-performing assets rise by $1.3 billion and still meet that test. As such, even if we see continued degradation, USB has already taken on additional reserves, and additional builds should be fairly modest.

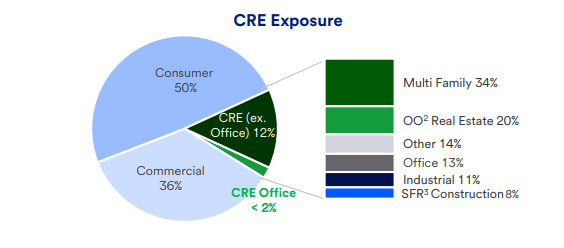

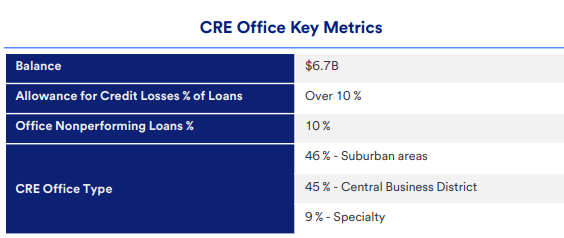

In terms of credit trajectory, commercial real estate (CRE) is the biggest area of concern. Importantly, USB has limited exposure to CRE of only $53 billion, or about 14% of its loan book. This is fairly modest compared to its peers and should help limit losses. In addition, not all racial equality rights are of equal concern. Multifamily is an area I feel more comfortable in given the tight housing market while office has more structural issues. Overall, 1.71% of CRE loans are non-performing, about 4 times the rate of other loans.

US Bancorp

This is concentrated in positions, not surprisingly, as 10% of loans are non-performing. However, USB has great capabilities here, and a diverse mix of features. Because they represent only about 1% of assets, I view the potential additional reserves here as manageable, and unlikely to exceed $25 million per quarter. Even if it took an additional 10% loss, its impact on EPS would be about $0.35 after taxes, likely to materialize over several years. Even an extreme scenario is quite manageable for a company with earnings power of nearly $4.

US Bancorp

Separately, I’d like to note that credit card charges are on the rise, tracking the rise in delinquencies last year. With employment strength and results now more similar to 2019 levels, after being very low for several years, I expect credit card losses to begin to stabilize in the second half, absent a recession.

US Bancorp

Finally, USB is well capitalized. Common Equity Tier 1 (CET1) ratio increased from 9.9% to 10.0% sequentially. This is also up from less than 9% last year as it was completing the purchase of Union Bank, and this strong capital improvement speaks to the bank’s earnings generation. I previously expected the company to reach a 10.4%+ CET1 ratio by the end of this year, and I continue to see this as a likely endpoint for capital. Because it purchased fixed income securities with lower yields, it incurred a loss of $8.7 billion in AOCI associated with these purchases. As the bonds mature and move toward par, this loss will decline to $6.6 billion by the end of 2025 at the 31/3 interest rate curve. While USB will need to hold more capital to offset these losses as they are gradually factored into the accounts, this natural combustion of losses over time will act as a tailwind.

I previously felt that USB could initiate buybacks in 2025 given its capitalization position. The administration confirmed last week that it needs to clarify regulations before the buybacks, which should take place by the end of this year. At this point, given its strong capital generation, it can use the capital to accelerate growth, reduce the number of shares, or increase profits. Given the ongoing regulatory discussion on the final rules, I do not expect buybacks to begin before mid-2025, but I do expect some buybacks next year.

Back in November, I was looking for $4.20-$4.40 in 2024 per share, driven by a rebound in net profit margin to 2.9% and non-interest revenue growth of 5%. With non-interest income growing at 7.1% in the first quarter, the company is on track to reach this benchmark. However, slowing loan growth and an unfavorable shift in deposit mix have slowed the recovery of net interest margin, although management still believes it can reach 3% net interest margin over time. With my NII forecast of $16.4 billion, I expect USB to earn between $3.90 and $4.00 this year, meaning the stock lives for about 10 times earnings.

Importantly, although it has taken a little longer, favorable deposit trends and continued ROA improvements should support net margin expansion and dividend growth in 2025 exceeding $4.30 per share. Furthermore, the quality of its credit portfolio is strong, and a significant capital improvement means shareholder payouts should increase next year. Meanwhile, investors collect a 4.8% yield. As such, I expect the stock to move into the upper $40s over the course of the year or 11-12x 2025 earnings, given its better regional condition. Its recovery continues with improved balance sheet flexibility, and USB remains attractive.