Venice Investment explained that VICI properties are likely to remain profitable in the future

imagedepotpro

We previously covered VICI Properties Inc. (New York Stock Exchange: VISI) in March 2024, to discuss the 2023 fourth-quarter earnings call and promising guidance for fiscal 2024, which has demonstrated management’s competency to date.

Combined with its decline, we thought the stock was still at a level A compelling investment thesis, thanks to the improved upside potential of its fair value coupled with an expanded dividend yield for those looking to dollar-cost averaging.

Since then, the VICI continues to decline -3.7%, with the market trading sideways at +0.3%. However, we believe it remains a gift, as the pullback has fueled increasingly affluent REIT returns, as strong profitability and a healthier balance sheet in fiscal Q1 2024 support the dividend investing thesis.

This comes in addition to the REIT’s recent investment in The Venetian Resort, which underscores management’s ability to grow profitably on a combination of Despite the high interest rate environment, which is due to higher annual rents coming.

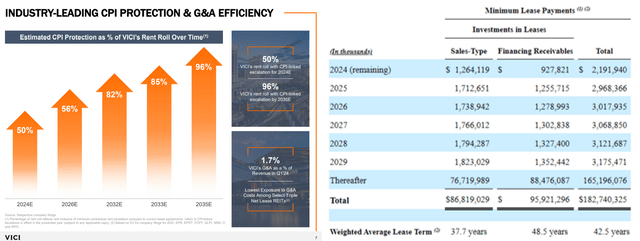

Combined with the very long lease term remaining for the overall portfolio and upcoming CPI-linked lease increases over the next few years, we believe VICI still represents a compelling buy.

VICI remains profitable enough to fund its growth opportunities – with shotgun deal explained

Currently, VICI announced another excellent earnings call for Q1 2024, with total revenue of $951.48 million (+2.1% QoQ/+8.4% YoY) and AFFO per share of $0.56 (+1.8% QoQ/+6.1% YoY).

Much of the tailwind was attributable to the strong performance seen in the gaming segment, which accounts for 98% of total rental revenue, with Las Vegas recording twelve consecutive quarters of total gaming growth with visitation numbers continuing to grow by +4.2% year over year in FQ1′ 24.

As a result, we can understand why VICI has entered into a strategic agreement to provide up to $700 million of capital to The Venetian Resort Las Vegas for extensive renovation and improvement work, representing 67% of its Q1 2024 investment.

Part of the pessimism embedded in its stock price may be attributable to a disappointing investment spread of 1.625%, based on a 7.25% cap rate in yield and a new 2052 bond of $750 million with an interest rate of 5.625%.

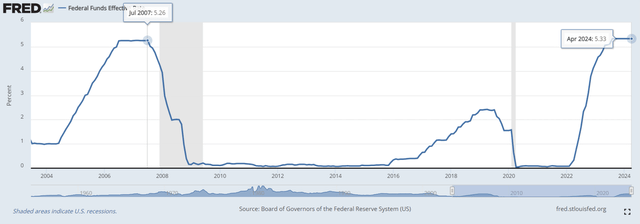

The effective federal funds rate

unique

Then again, we think it might be more prudent to look at VICI’s overall blended investment returns instead, especially since interest rates are at their highest levels over the last 20 years, thanks to sticky inflationary pressures.

Based on total REIT debt of $17.12 billion (QoQ/+0.4% YoY) at weighted average interest rates of 4.364% as of March 2024 (+0.013 points QoQ/+0.024 YoY Annualized), we are still looking at a relatively healthy 2.88% total spread.

At the same time, readers should also note that the annual rent is under the existing Venice resort The lease is expected to escalate annually “following each capital financing”, with FY2024 likely to deliver improved numbers from the $256.25M reported in FY2023 (+20.4% YoY) and the $265.2M annualized amount achieved. Reported in fiscal 1Q24 (+2.9% QoQ) / +5% YoY), well offsetting the initially low investment margin of 1,625%, as discussed above.

VICI Wallet

Visi

These developments also confirm that VICI’s investment efforts remain profitable in the long term, especially as the extensive renovation works completed on its properties will be mutually beneficial for the tenant and the REIT.

Readers should also note that the Venice portfolio is expected to be CPI-linked from March 2031 onwards, joining the rest of the REIT portfolio with a weighted average remaining lease term of 42.5 years, providing a very long-term view to the promising top /bottom lines.

In addition to the net debt to EBITDA ratio of 5.42 times in the first fiscal quarter of 2024, compared to 5.55 times in the fourth fiscal quarter of 2023 and 5.91 times in the first fiscal quarter of 2023, while approaching 4.45. Back in fiscal 2019, the key taking away from our Q1 2024 performance is that we believe VICI remains well-positioned to grow profitably as a leading gaming stock/REIT, regardless of near-term macroeconomic uncertainty.

VICI is inherently undervalued – offering opportunistic investors double returns

Visi Reviews

Seeking alpha

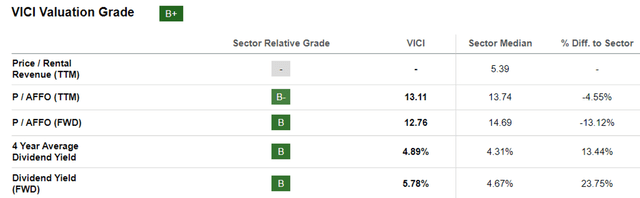

As a result of the promising developments discussed above, we believe VICI remains inherently undervalued at FWD/AFFO price valuations of 12.76x, down from the previous article’s 12.96x, its 1-year average of 13.62x, and its pre-pandemic average over 3 years is at 14.05x, and the sector average is 14.69x.

This is particularly because consensus forward estimates remain stable since the previous article, with the REIT expected to deliver an expansion of top/bottom net income at a CAGR of +4.2% and +4% through FY2026.

We believe VICI is not expensive compared to its peer, Gaming and Leisure Properties, Inc. (GLPI) at FWD Price/AFFO valuations of 12.01x, the latter is expected to report an expansion in net profit/income at a CAGR of +3.1% and +2.6% through FY2026.

So, is VICI stock a buy?Sell, sell, or hold?

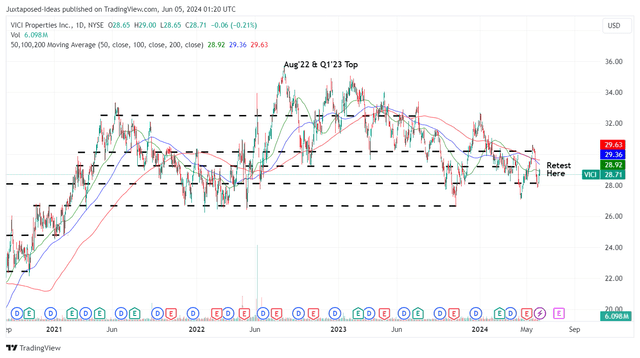

VICI 5Y stock price

Trading offer

Currently, the VICI continues to draw lower lows and lower highs, while temporarily setting $28 as its support level, which is relatively consistent with the previous article at $29.

For context, we provided a fair value estimate of $30 in our last article, based on fiscal 2023 AFFO per share of $2.15 and benchmark price/AFFO valuations of 14x.

Currently, based on VICI’s recurring guidance for FY2024 AFFO per share of $2,235 at the midpoint (+3.9% YoY) and the same P/E valuations of 14x, it is clear that VICI is trading below our estimated fair value. $31.30 USD.

We maintain our belief that there remains potential capital appreciation of +18% to $33.80, based on FY2026 consensus AFFO per share estimates of $2.42 and benchmark price/AFFO valuations of 14x, with normalization in economy costs. Total/borrowing only. It is a matter of time and the Fed expects it to shift from the fourth quarter of 2024 onwards.

At the same time, these lower levels increase VICI’s forward dividend yields of 5.78%, compared to the 4-year average yield of 4.89%, the sector average of 4.67%, and US Treasury yields of 4.49% to 5%. 37%.

Its dividend investing thesis also remains strong, based on a stable TTM AFFO payout ratio of 74.66% compared to the sector average of 73.61%, with Quantitative Alpha continuing to grade the REIT with an A for dividend growth and a B for dividend safety.

As a result, we believe VICI remains a compelling buy for opportunistic investors, especially as the stock has found strong support levels at $28, providing an improved margin of safety for those looking to dollar-cost averaging.

Risk warning

It goes without saying that as long as interest rates remain high, short-term REIT investments may post lower spreads depending on management’s choice of capital (either leveraging debt or offering equity).

This is particularly because VICI operates in the gaming sector, a sector that banks typically consider high-risk. Making matters worse is the fact that two large tenants, including Caesars (CZR) and MGM Resorts (MGM), account for nearly 74% of rental income, though they are well balanced by an impressive 100% rental collection during the worst Epidemic periods.

At the same time, inflation remains excessively sticky, leading to a prolonged macroeconomic normalization with the Fed pivot expected only by the fourth quarter of 2024 and a normalization of borrowing costs likely by 2027, based on the Fed’s latest forecasts.

As a result, VICI investors should monitor these key risks while tempering their near-term expectations, as we may naturally see a decline in investment volume and growth in the future.