pcess609

Investment summary

My recommendation for Vertex (Nasdaq: FX) is a Buy rating. The strong execution demonstrated so far, coupled with the visible growth catalyst, makes VERX an attractive buy, in my opinion. In particular, potential opportunities from organizations moving from ECC to S/4HANA can be the driver behind this Strong acceleration in VERX’s growth over the next few quarters. Even if I just assume mid-teens growth is coming, at the current multiple, I see at least a 13% upside.

Business overview

VERX provides an on-premises and cloud-based platform to help clients comply with their tax requirements. At a high level, the platform helps automate end-to-end indirect tax processes (document and data management, tax determination, etc.) involving complex tax transactions. In terms of segment, VERX has only two reporting segments: Subscription Revenue, which consists of cloud and on-premises subscriptions, representing 84% of total revenue, and Service Revenue, which represents 16% of total revenue.

VERX released its results for the first quarter of 2024 two weeks ago. Total revenue grew 18.1% compared to Q1 2023, an acceleration of Q1 2023 growth of 15.5%. This growth was driven by subscription revenue, which grew by 18.8%. Gross margin increased 70 basis points to 72.5%, showing that this strong growth performance was profitable. And at the bottom of the income statement, adjusted EBITDA margin saw a massive expansion from 15.2% in 1Q23 to 23.4% in 1Q24.

VERX’s competitive moat, such as its leadership position in the enterprise tax automation industry, has a very established customer base giving it a clear stream of cash flow to reinvest in its business to stay ahead of the game. I believe the basis of this leadership position is their product that is designed to meet the needs of enterprise customers (e.g., can meet complex tax requirements, customizations, etc.) that their smaller peers cannot provide due to the fact that their product caters to simpler uses. Good reviews and a good reputation in the industry also help to win customers, as the majority of large organizations (in key markets) are usually hands-on in terms of software adoption.

Growth isn’t slowing down any time soon

VERX’s growth outlook remains strong, and I have great confidence in its ability to maintain this level of growth for the foreseeable future given its strong execution, SAP ECC tailwinds, expanded partnerships, and pricing power.

Redfox Capital Ideas

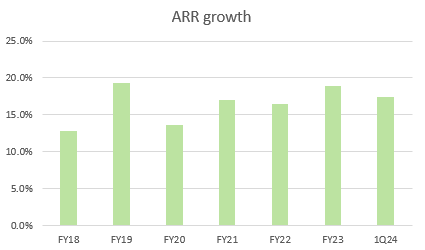

Upon execution, Q1 2024 performance was exceptional given the difficult and challenging macro environment. While headline annual revenue growth was flat compared to Q4 2023, at 18.1%, the important part to note is that subscription revenue grew 18.8% in Q1 2024, representing a sequential acceleration of 90 points. 4Q23 basis. Additionally, VERX has been able to maintain strong annual recurring revenue (ARR) growth at a high level over the past few years, with little to no signs of impact from the challenging macro environment. 1Q24 also represents the number 13y For the second consecutive quarter, VERX exceeded quarterly revenue guidance, clearly demonstrating management’s strong revenue vision and ability to execute and deliver on goals.

On top of its strong implementation profile, I expect VERX to continue to reap the benefits from ECC to the S/4HANA backend. Recall that in the 2Q23 earnings call, management noted that there are over 1,000 customers still using ECC, and SAP will stop supporting ECC in 2027. As for the customers still using ECC, they are largely ought to Go elsewhere and find another solution and go through the pain of tearing up and replacing the digital real estate of the entire organization – an alternative that I think most organizations would try to avoid. The opportunity for VERX is that a lot of existing ECC users probably don’t have an automated tax solution (like what VERX offers), and when they move to S/4HANA, it opens up an opportunity for them to upgrade to an automated solution, and those deals are huge in volume.

We’ve also helped one of the world’s largest manufacturers of branded food products automate Their manual processes around use tax To ensure we are not overpaying suppliers and creating audit risk. In each case, the transition is made to the SAP platform for Mid-six figures of annual recurring revenue For Vertex, which shows the magnitude of this opportunity. We expect this to continue to be a new business driver for Vertex in the coming years There are still thousands of customers at ECC, a platform that SAP announced it would stop supporting in 2027, moving to S/4HANA. Second quarter earnings transcript 23

Now that we’re already halfway through 2024, the timeline for all ECC users to move to S/4HANA has run out (only 2.5 years to go), and I expect an accelerating rate of migration over the coming quarters as most organizations do. You may migrate before support ends. The bear case is that organizations simply no longer use ERP systems after support ends, but I think this is very unlikely given that ERP upgrades to the cloud will be a priority for organizations as they want to adopt AI tools in the future (Which requires cloud computing to do so). Furthermore, VERX has proven to be a superior product, as seen in a case study where a client originally chose an alternative indirect tax solution, but due to inadequate support and a pricing model that led to significant cost overruns, they returned to VERX. Finally, in terms of co-selling momentum with SAP, it has shown very positive continued momentum. In Q1 2024, SAP sales representatives were instrumental in bringing VERX to the early stages of multiple deals.

VERX’s expanded partner relationships with Microsoft, NetSuite, Shopify, etc. should also help drive incremental growth as they help expand VERX’s distribution capabilities to a wider range of potential customers. Note that the partnerships target both ends of the market (i.e. Microsoft for large enterprises and Shopify for SMBs), and I really like this because it gives VERX exposure to a full range of customers. Last but not least, VERX can continue to raise prices, and has done so by raising prices at an average of 5% per year (according to Q2 2020 earnings data).

evaluation

Redfox Capital Ideas

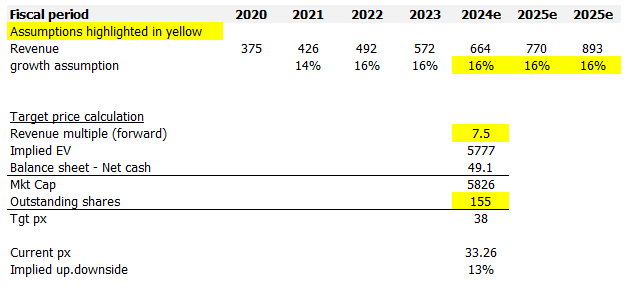

I model VERX using the forward revenue approach, and using my assumptions, I believe VERX is worth $38. I believe VERX’s growth trajectory is strong, and the company can easily sustain this level of growth into the mid-teens at least. Note that VERX has been growing at this level even without the incoming migration flow (from ECC to S/4HANA), so there is a high probability that we will see an acceleration in growth due to this migration. Because timing is difficult, I chose to assume growth in mid-adolescence only. Any upside surprise in growth would make the upside more attractive. However, I think the market is already starting to appreciate the potential for growth acceleration as valuation has trended towards 7.4x forward revenue (1.4x above the average of 6x), and assuming this multiple holds, I think VERX is an attractive option. long.

risk

My growth estimates could be overly optimistic if downselling or new banner pressure is more severe than I expect or if the macro environment has more severe impacts on VERX than I expect, although I believe VERX will be more resilient in a bear market given the environment. Reduced competition (subcompetitors are forced to exit the market as demand declines).

Conclusion

My view for VERX is a Buy rating given its strong execution and strong growth potential. Regarding the former, VERX has a proven track record of exceeding expectations. As for the latter, the upcoming wave of migration from SAP ECC to S/4HANA represents a huge catalyst for growth. VERX’s partnerships with industry leaders such as Microsoft and SAP further strengthen its position. Even assuming a conservative growth rate in the mid-teens, VERX offers upside potential at its current valuation.