DNY59

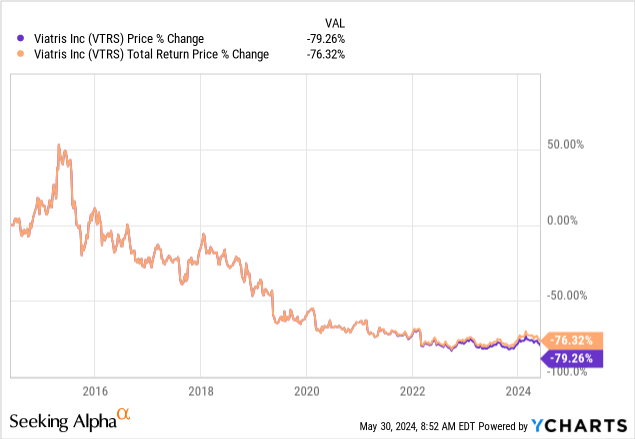

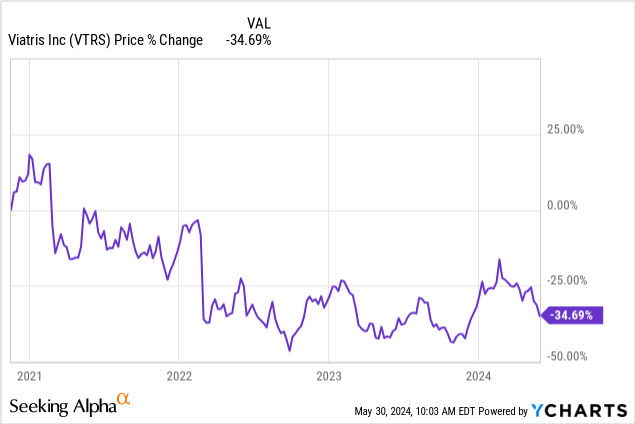

In our latest coverage of Viatris Company (Nasdaq:VTRS) We pointed out that the company was an example of a value trap. It looked cheap and attractive to the “low P/E” crowd. But the melting ice cube prevented any return For everyone except those who bought extreme dips and sold minor rips. The chart below shows the performance of VTRS and its predecessor Mylan Labs. Mylan Labs has merged with the generic unit of Pfizer Inc. (PFE) and began trading as VTRS in November 2020.

However, the stock has popped up a bit since we reviewed its Q3 2023 results.

Seeking alpha

Now look at Q1 2024 results to see if you should buy the role.

First quarter 2024

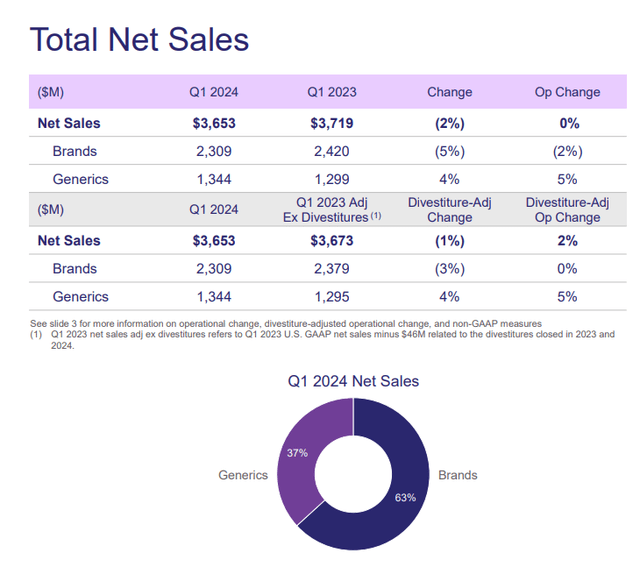

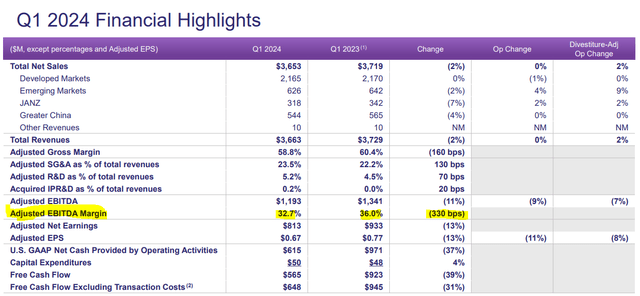

VTRS reported first-quarter 2024 results that were in line with expectations and revenue It comes in a lighter shade. Most of the VTRS’ “mistakes” have been on the revenue front, where analysts struggle to model how quickly the ice cube will melt. This quarter, net sales decreased by 2%. The change in operating sales, which removes the impact of currency changes, was flat. VTRS issues continue to emerge from its private label segment. This is down 5% year-on-year. Generics were able to offset some of the pressure here and improved 4%.

VTRS presentation for the first quarter of 2024

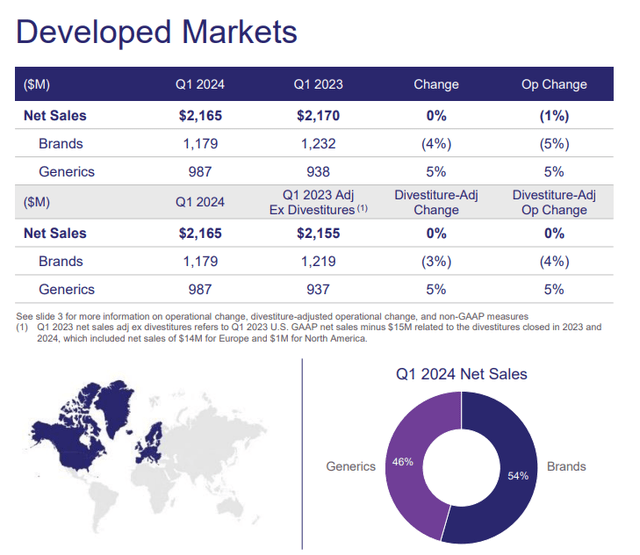

When broken down by regions, we saw that developed markets closely mimic the overall numbers.

VTRS presentation for the first quarter of 2024

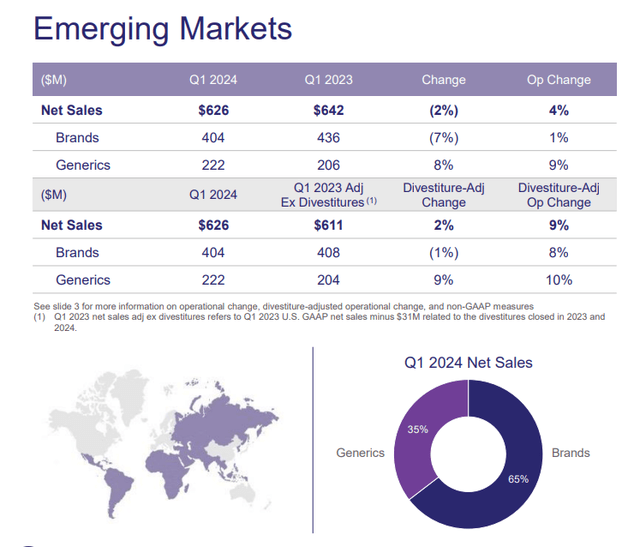

In emerging markets, the pressure on brands has been more acute, but the generic sector has once again risen to the challenge.

VTRS presentation for the first quarter of 2024

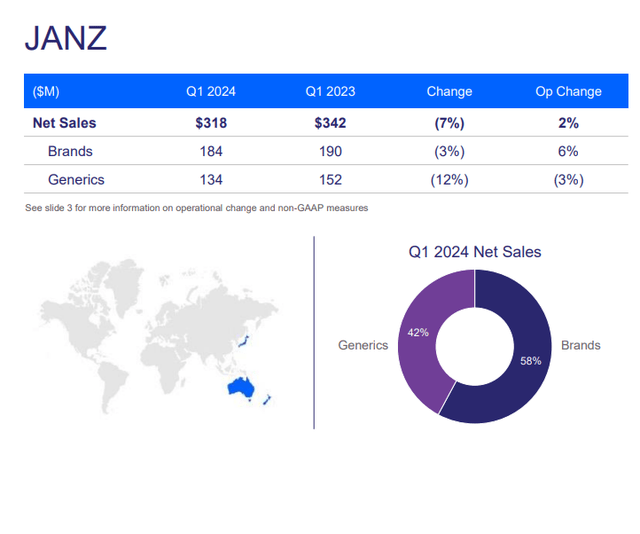

The JANZ region (Japan, Australia and New Zealand) was the worst of all. This was primarily due to the Japanese yen serving as a third world currency. With the exception of forex movements, the results were actually very good.

VTRS presentation for the first quarter of 2024

One of the biggest challenges VTRS has faced is the impact of lower sales on EBITDA. It is almost impossible in any model to stabilize EBITDA when sales are constantly declining. These fixed costs tend to remain stable over time in the best of times. Against a background of moderate to high inflation, as is the case today, they tend to rise. Adjusted EBITDA margins, washed out of all potential sins, fell by 330 basis points. This represents double the adjusted gross margin decline that we saw.

VTRS presentation for the first quarter of 2024

Further down, you can see that free cash flow is down 31%. However, this is a fairly volatile series, and we only measure it annually. Although the results were in line with expectations, they continued to demonstrate the pressures the company is facing.

Prospects

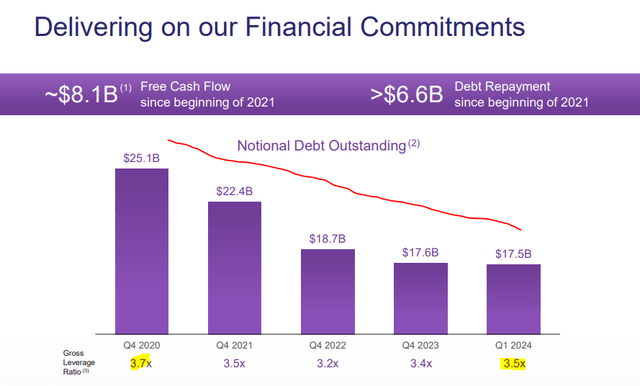

VTRS has this slide below (updated quarterly, of course) in all of its presentations, and it’s our favorite. This red line is our line.

VTRS presentation for the first quarter of 2024

VTRS hilariously shows how ineffective their entire strategy has been up to this point with that one slide. $6.6 billion of debt repayments, which includes the sale of some biosimilars at very high multiples, did not move the debt to EBITDA. Well, technically it’s 0.2 times less, but that’s just thanks to the starting point. 3.5X is also very high for a melting ice cube of revenue. This is also a 12-month plus figure. EBITDA guidance is lower than we see above.

VTRS presentation for the first quarter of 2024

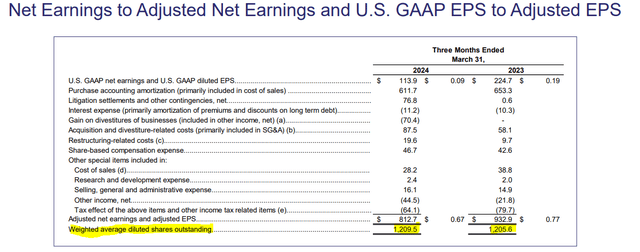

Investors continue to get excited about the low P/E ratio. Adjusted earnings of $2.73 make the stock look cheap. We emphasize the word “see” here. Investors see this as meaning that VTRS could give them returns of 25% at the current price. Well, if you think so, here are the first four quarters of adjusted earnings after the formation of the VTRS. Add those.

Seeking alpha

Next is price performance.

Many people have argued about how cheap this company was at the time (see The Bubble and Its Remnants). However, the returns were MIA. Even the much-talked about stock buybacks are not enough to offset the dilution of stock-based compensation. Shares rose in the first quarter of 2024 compared to the first quarter of 2023.

VTRS presentation for the first quarter of 2024

There’s certainly an outside chance that some of these phase III studies will become a take-home measure. On its last R&D day, VTRS discussed two new drugs, Selatogrel and Cenerimod. Silatogrel is a self-administered medication for the treatment of myocardial infarction, while cinerimod is for the treatment of severe systemic lupus erythematosus (also known as SLE). There are some other potential drugs as well that could move the EBITDA needle meaningfully.

But the problems are fairly severe, too. Debt to EBITDA is stuck one cycle higher than we would like to turn to the upside. In this scenario, we don’t mind paying a higher multiple of Adjusted Earnings for a long position. In other words, VTRS, if you want our money, show that you can actually reduce debt based on ratios and not just absolute debt levels. As it stands, we have increasing generic sales offset by brand sales. Viatris Inc.’s margin pressure could be… In its beginnings. Analysts are finally getting the picture that these adjusted earnings won’t grow even if VTRS starts buying back shares in earnest.

Seeking alpha

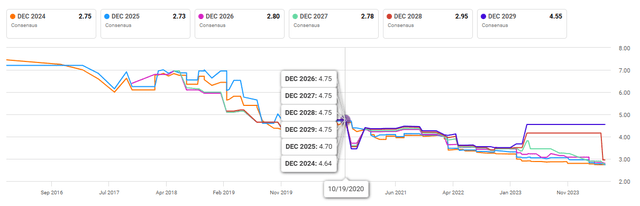

Although the picture has been disappointing over the past six months, the numbers from a few years ago were on another level. Fair warning here: Don’t drink coffee as you see the forecast earnings estimates for these same years, in 2020.

Seeking alpha

So, three years after our first piece, we still feel at peace with not having this. Of course things can change, we will keep an eye on that. Meanwhile, those who want a piece of the action should consider covered calls.

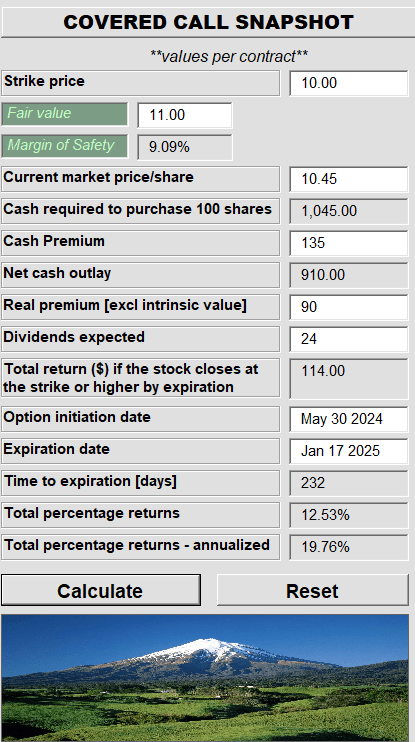

CIP

Deep value investors may scoff at those returns, but anyone who does this dance over the past three years will likely outperform common stocks by at least 50%.

Please note that this is not financial advice. It may seem so, it seems so, but surprisingly it is not. Investors are expected to conduct their due diligence and consult with a professional who knows their objectives and limitations.