com. bgwalker

My initial coverage of Walmex — officially, Wal-Mart de México, SAB de CV (OTCQX:WMMVY) (OTCPK:WMMVF) — turned out to be entirely justified. Against the current price of around $42 on January 2, the current price at writing of $35 or so represents a +15% decline since the beginning of the year. My review There was a comment, stating that near-term headwinds may mean this is the wrong time to enter. Upon further analysis, the fundamentals appear to be sound following the announcement of Q2 2012 earnings at the end of April. If you watched my initial article, you’ll notice that I mentioned the $32 to $42 price range that the stock appears to be stuck in. It seems that this phenomenon, which occurred over the past two years, still exists. The stock bounced off support just above $32 after the Q323 report, and has since been rejected twice at just over $42. Verify the validity of this assumption.

Now that Q124 results have been out for a while and Q2 is in full swing, let’s take a look at how the fundamentals are shaping up, and whether or not this is still worth the wait.

Spoiler: I’m upgrading my rating from Hold to Buy, and the reason is because I see a lot of strength in action as we continue to weather persistent headwinds that are largely macro in nature.

Quarterly Performance – Q423 and Q124

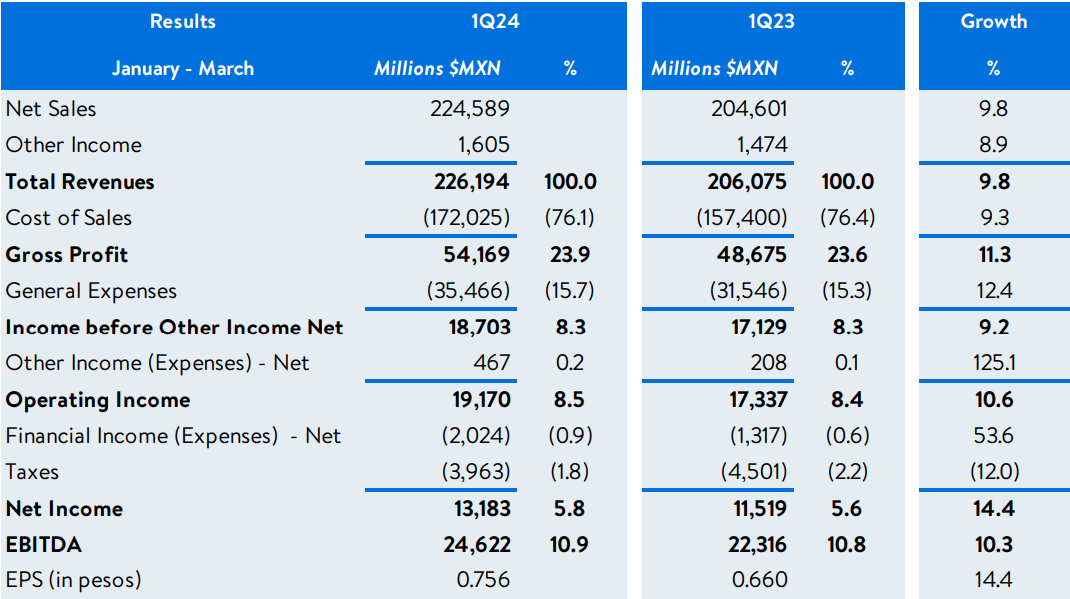

Walmex appears to have come out of the gate with some impressive numbers in 1QFY24. It held back revenue growth of 6.7% coming out of Q4 (revised 7%), but Q1 painted a very different story. To keep things relevant, I’ll just focus on the 124th quarter results and how I see things moving forward over the course of the current fiscal year.

Q1 revenue growth was a strong 9.8% year over year, higher than any single quarter until FY23. To me, this immediately means some tailwinds are emerging; Or at least it tells me that near-term headwinds are not as strong as they were two quarters ago when I last covered Woolmex.

But let’s not get too excited at this point, because it’s still too early to say whether this kind of growth approaching 10% at the top will be sustainable through the year, especially when the entire market is so volatile and consumer sentiment is so volatile. . So. According to a Mastercard Data and Services report released earlier this year, “Latin America will benefit from stabilizing inflation, leading to a smooth deceleration in GDP growth.” However, the same report also shows that “consumers benefit from strong labor markets, but consumer spending growth will moderate in 2024 compared to 2023.” This is a mixed bag, unfortunately.

The good thing is that Walmex seems to be bucking trends with its performance – for now, at least. One of the main factors was the appreciation of the Mexican peso against the dollar until the beginning of April. The problem now is that this trend has taken a sharp reversal, and is currently quite volatile. More on that later.

XE

However, a rally in October 2023 to early April 2024 helped Walmex as a powerhouse through two quarters. This coupled with a 2.5% increase from the calendar effect helped Q1 revenue grow strongly by 9.8%. However, you won’t see much in the way of operating leverage, which is typical in the retail industry where variable costs like SG&A tend to rise along with revenue. Moreover, with the strong pace of store openings in the fourth quarter, operating expenses were bound to increase. However, I did like the fact that cost of sales or cost of goods sold grew just 9.3% on the back of a 9.8% rise in revenue, which indicates some pricing power at the gross margin level.

Woolmix Press Release – S124

The 14.4% net EPS growth was also supported by a half-million-peso tax cut and a 125% increase in the “other income” line item in the profit and loss statement. Overall, it was a very strong quarter supported by favorable currency, pricing strength, calendar effect, lower taxes, and increased other operating income.

Digging deeper into the sector classification in terms of revenue and profitability, we see that the bulk of the growth at the top and bottom came from the core Mexican market, which contributed MXN 190 billion versus MXN 36 billion in Central America, and showed much stronger growth rates in the former at 11.2%. compared to 9.7%, respectively. The EBITDA difference was more pronounced, with Mexico recording growth of 12.2% versus 6.9% in Central America. Moreover, the pricing advantage is even more pronounced in Mexico, where gross profit rose 13.1% on the back of 11.2% revenue growth and an underlying operating leverage spread of 190 basis points, while Central America showed a difference of only 30 basis points plus Revenue of 8.7%. growth rate.

It’s always good news when a larger sector shows healthier growth numbers, and many investors tend to miss the fact that the quality of revenue growth is just as important, if not more important, than the revenue growth itself. The EBITDA growth for these respective sectors reinforces this assumption.

Overall, Walmex is showing clear uptrends at the top and bottom; Unfortunately, the stock price did not follow the same pattern, as we saw above. However, it gives me more confidence in changing my rating to buy, which combines well with the fact that it is trading at the lower end of this range that it has established over the past two years.

However, the second quarter may not come in as strong, and we are already seeing weakness in the $MXN-USD pair. This suggests that the tailwinds of the past two quarters may not continue into the second quarter, so I would be wary of expecting similar growth when the report comes out next month. Let’s also take a look at what’s new as of Q2 so we have a better view of what to expect.

New developments and their repercussions

The obvious new development is the announcement of a new CEO, Ignacio Card. The positive reason is that his predecessor is taking on a bigger role as executive vice president and regional CEO of Walmart Inc’s (WMT) Canada, Chile, Mexico and Central America divisions, and is eventually expected to take the reins as head of Walmex. Council sometime in H224. I usually view this type of smooth succession as a positive development because the company has time to consider the pros and cons of the new employee. In this case, the new CEO is appointed to “further strengthen Walmex’s successful multi-channel strategy and provide continuity to our business.”

One clear negative development in the 124th quarter was the sudden slowdown in store growth. In Q323, Walmex opened 24 new units. In the fourth quarter, it jumped more than threefold, reaching 101 new units; However, in the 124th quarter, that dropped to single digits with an increase of just 11 stores. This extremely volatile rhythm is not something that a lot of investors will be comfortable with, and I can sympathize with that. On the one hand, this could be a sign that management expects growth to slow over the remainder of fiscal 2024; On the other hand, it can be considered a wise move to conserve cash.

My point is that it’s the latter. We need to go to the balance sheet and cash flow statements to get a better perspective on this. Between September 30, 2023 and December 31, 2023, Walmex’s C&CE (cash and cash equivalents) decreased from approximately MXN 50 billion to just over MXN 40 billion. While this would have helped finance some of the new stores’ capital needs, as evidenced by the jump in cash used to invest in long-term assets from MXN17 billion to more than MXN46 billion between the 323rd and 423rd quarters, it would have That also helps raise the need to conserve cash for a period of time. In other words, with its strong cash position at the end of the third quarter, the company had enough cash to support this expansion in the following quarter, but by the end of the fourth quarter, we saw the cash position fall near the MXN 40 billion mark, so it makes sense to prioritize maintaining On the criticism again. As of Q1, C&CE was back at about $44 billion, so this was a very wise move by management to first leverage its cash stock aggressively by funding store growth, and then throttle that aggressive growth until cash flows once again replenish that cash stock. .

I expect the slowdown in store growth to continue during the second quarter, but perhaps not as weak as in the first quarter. These new stores will very likely boost revenue as well as operating cash flows, so once this phase is complete, we should see more aggressive numbers again on the store count front, perhaps as soon as the 324 quarter.

The third positive development is that the nearly four-year investigation by COFECE, or the Federal Economic Competition Commission, is moving closer to resolution. Walmex submitted the necessary supporting documents and defensive evidence at the end of 2023, so we should be able to see some sort of closure for this phase of the battle later this year. Walmex itself expects this to happen in H224, but these investigations are highly unpredictable from a timeline perspective.

Conclusion: Is there value here?

Value should always be preceded by growth, in my opinion. Without growth, value is usually limited to extracting more and more profits from a stagnant revenue base or resorting to financial engineering. In my opinion, neither of these is sustainable, so it’s encouraging to see Walmex’s continued strong high-single-digit and low-double-digit growth at the top and bottom. I believe that the company is growing in a sustainable way, although there are significant fluctuations in its operational activities that make it almost cyclical. But over a longer time horizon, the upward trends in growth and the potential for continued growth are quite clear.

The headwinds I mentioned in my last article persist, but I see them dissipating over the next year. One example is the weak exchange rate of the Mexican dollar against the US dollar which has likely taken a big chunk out of the second quarter revenues that will be reported next month, but forecasters expect a rebound to US$17 per US dollar, with the sudden decline attributed to a A surprising landslide victory in the Mexican elections. There are also other factors that could help the peso strengthen against the dollar further, such as the carry trade or forex carry trade advantage that Mexico still has over the United States with interest rates rising at 5%, at around 11% set by the Bank Federal Reserve. Bank of Mexico in May 2024. Inflation remains high in Mexico, so we could see a prolonged period of rising interest rates and a strong spread over US benchmark interest rates.

In the final analysis, there appears to be some level of stability on the horizon for Walmex, which means continued growth, but perhaps at a slightly subdued level compared to the first quarter. In terms of valuation, the current price suggests a price to forward earnings of less than 18 times, based on an EPS estimate of $1.98 for FY24. That’s not necessarily expensive, but it’s not cheap either. A year later, we see a forward P/E of about 16x based on analyst forecasts for FY25, so I feel quite comfortable upgrading Walmex to Buy versus my previous Hold rating. My reasons? Primarily, despite persistent headwinds such as very high interest rates and inflation, consumer sentiment appears resilient. This evidence comes from the excellent growth recorded at the top and bottom of the first quarter, so even if the rest of the year sees more moderate growth rates, there is still some long-term value in this stock. The second reason is the strong store growth pace from Q4, which will likely help offset any declines in sequential QoQ growth rate we may see.

To be clear, the risks mentioned in my last article are still very much present now, but those risks have been mitigated somewhat by the company’s on-the-ground performance coming out of the gate in FY24. Moreover, with a CEO New specifically tasked with growing our e-commerce and omni-channel offerings, we could see a more stable revenue growth story in the coming quarters.

As always, these are my opinions, and investors are advised to conduct due diligence before investing in any security. For me, there is enough evidence to upgrade WMMVY to buy.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.