Deepblue4you/E+ via Getty Images

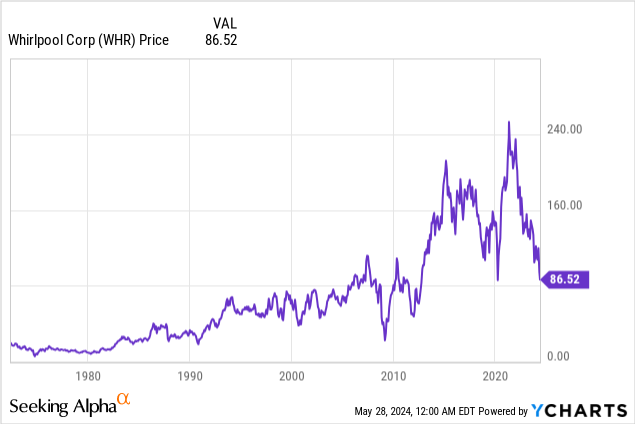

Whirlpool (New York Stock Exchange:WHR) is the most important participant in the flagship devices sector in North America and Latin America. Moreover, the company is witnessing a sharp decline in its share price, firstly due to the heavy cyclical nature of the business and secondly Due to an overleveraged balance sheet resulting from poor capital allocation by management since the second half of 2021. At this point, WHR is valued at the same prices as it was in the last severe crisis, in March 2020, but that does not mean it is a buy. Easy from now on, it’s a worse company. For now, I think Whirlpool is on hold. Due to its cyclical nature and weak balance sheet, the company has become more vulnerable to interest rates. While macroeconomic conditions remain challenging, the stock could continue to decline without an absolute bottom.

Whirlpool, the main participant

As presented at its 2024 Investor Day presentation, Whirlpool is the No. 1 company by market share in the major appliance businesses in both North America and Latin America, with sales of approximately $11 billion in the former and $3.5 billion in the latter, out of a total Revenue is about 20 billion.

This is particularly important because it shows a strong business that, although cyclical, will be almost irreplaceable by new market players or existing competitors. WHR brands like Kitchen Aid, Maytag, or the right Whirlpool won’t lose market share easily since the cyclical nature of the industry gives them a huge advantage when the macroeconomic environment is right, in my view. For example, WHR will sell its products well when money is easy. In contrast, when money is hard to come by, and when interest rates are high, WHR will be able to leverage its mass production and sell its products first compared to its competitors as it can lower its prices easier due to economies of scale of being the largest. Market participant, in my opinion.

This alone would make buying WHR straightforward at low prices, since we might reasonably assume the company will come through the other side of the cycle due to its irreplaceability. Unfortunately for people who want to buy the stock and existing shareholders, Whirlpool’s management has had poor capital allocation since 2021, creating a balance sheet that is difficult to digest, thus adding uncertainty and volatility to the stock.

Some context

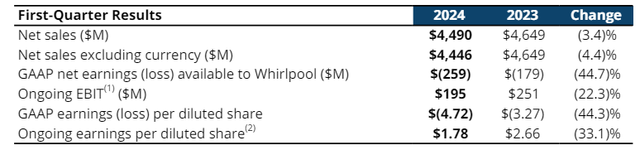

Following its latest earnings release, Whirlpool reported a 4.4% year-over-year sales decline adjusted for currency fluctuations, which translates to a 33% decline in “sustained” earnings per share. This ongoing term refers to some adjustments the company makes to show accurate results without the influence of mergers and acquisitions that the company is currently undertaking in Europe. I’ll cover this in some detail later. The sharp decline in profits compared to net sales is due to the very thin margins in the nature of this industry, where every lost dollar in revenue is felt keenly in the bottom line.

WHR results for the first quarter of 2024 (Whirlpool Q1 2024 earnings release)

The administration is taking some measures

Following its investor day presentation, WHR set about transforming its portfolio. This strategy focuses on reducing global exposure to improve better and more reliable profit margins and overall growth. One of the measures taken is to exit the EMEA markets and bet on India.

This exit from EMEA is being implemented through the creation of a new company called Beko Europe, which should bring $200-300 million in additional cash flows for 2025. Frankly, this sounds great, but in the end it will not be enough to mitigate the damage. that happened. to the balance sheet. However, getting rid of the MDA Europe business is a good decision as it has a terrible EBIT margin.

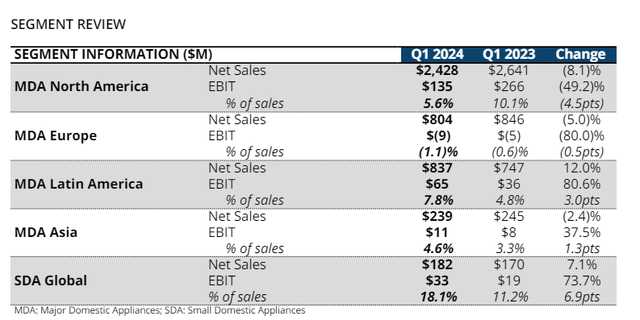

Review the WHR sector by geographical distribution (Whirlpool Q1 2024 earnings release)

Bad decisions made by management in the past affect the balance sheet today

In fact, one of the most dangerous events that can happen to a stock is having a good dividend at risk. Unfortunately, this is the case with the human rights organization. Dividends are expected to reach $400 million for the current year, after the recent earnings announcement, and the company’s dividend payout ratio will reach about 70% of the expected free cash flow of $600 million for this year. While this doesn’t pose much of a risk to the dividend right now, if the market deteriorates quickly enough by next year, the stock could continue to suffer as dividends become less secure.

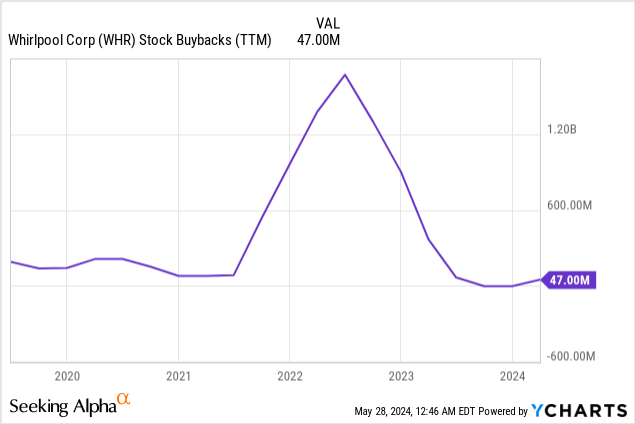

Additionally, management did not capitalize on the good times in 2021. Instead of reducing WHR’s debt, it decided to conduct stock buybacks while the stock was worth between $150-$220 per share, at the highest possible valuations.

To make matters worse, after this massive misallocation, management decided to acquire InSinkErator in an all-cash deal worth 3B for an expensive company valued at 14 times EBITDA in what would become a cyclical business. Do not get me wrong; InSinkErator is a great company, but management has taken on a lot of additional debt, which now represents $350M in interest expense, which is close to 60% of this year’s projected free cash flow.

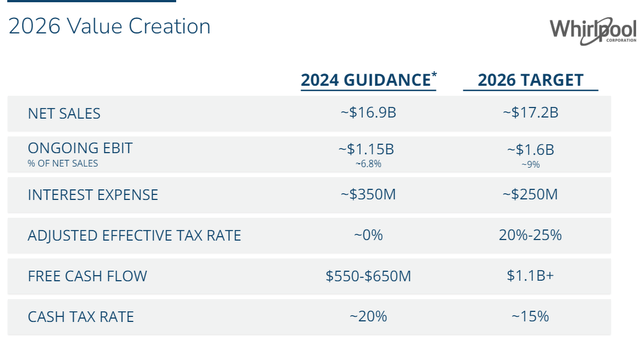

Whirlpool’s expectations about value creation (Whirlpool Investor Day 2024 Presentation)

In addition, the balance sheet is not in good shape, with over 8 billion in long-term liabilities, only 2 billion in tangible long-term assets, and cash flows of 600 million, with a huge interest expense of 350 million; The company is simply too risky and relatively poorly managed. This is undoubtedly why S&P Global rates WHR’s debt at BBB with a negative outlook, the worst possible rating before speculative grade.

Potential upside risks

There is no doubt that Whirlpool is a very special company with many famous brands. I think the stock will eventually rise again from the lows we saw recently, but the question is, from what bottom?

Some of the upside risk I see from the stock comes from potentially large investors coming in to buy at this price, providing support to the valuation, which is a good thing as they can secure high dividends that are not under much threat at the moment. Another upside risk could come in the form of the Fed surprising markets and making comments about cutting interest rates sooner than expected. This information can fuel hope among investors and reduce the risk of a company’s balance sheet, causing the stock to rebound sharply. However, I think the latter scenario will happen, but we don’t know from what price point.

Conclusion

In my opinion, Whirlpool’s management has done a poor job of serving shareholders. Drastically increasing debt levels by purchasing expensive assets while repurchasing shares at the worst possible time only reveals a poor capital allocation strategy. Fortunately, margin improvement, combined with the company’s size and importance in the market, combined with Beko’s European venture and really low valuations, make this company difficult to sell at this stage. However, the company is far from a buy as it is still relying on the Fed to make interest rate cuts to improve demand and ease the resulting pressure on the balance sheet.

Having said that, the stock is an obvious hold if you can hold a bag of this collapsing stock, but if you’re trying to start a new position, this stock is a bet on the Fed cutting interest rates sooner rather than later. However, I prefer to buy other less risky assets such as long-term bonds if I am betting on lower interest rates.