DenisTangneyJr/E+ via Getty Images

introduction

On May 28, I wrote an article entitled “My Favorite! 3 Highly Attractive Stocks for the Natural Gas-Powered AI Boom.”

In that article, I focused on what I thought would be very long Strong bullish case for natural gas prices, supported by massive growth in energy demand due to new artificial intelligence applications.

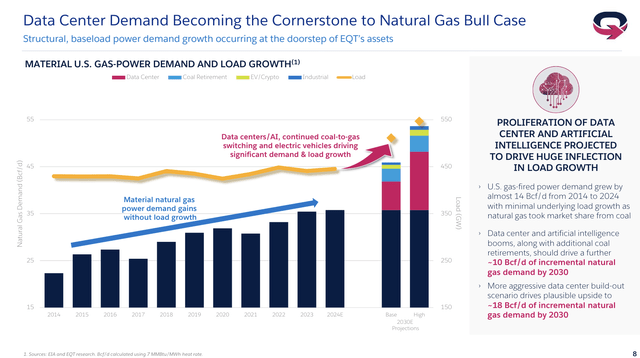

The report added that up to 8.5 billion cubic feet per day of natural gas may be needed to keep up with the rise in demand.

(…) The report appreciates Current power demand from data centers is 11 GWwhich is in the basic state It is expected to grow to 42 GW by 2030.

The report added that in its basic state, about 2.7 billion cubic feet per day of additional natural gas will be needed by 2030. – Reuters (emphasis added)

According to the EQT website institution (IQT), one of the world’s largest natural gas producers, we could see demand increase by 10 billion cubic feet per day from AI alone by 2030!

The most optimistic estimates point to a gradual increase of 18 billion cubic feet per day.

EQT Company

Again, this is from the AI alone!

Excludes:

- Global population growth.

- Middle class growth in emerging markets

- Continuous shift from coal to natural gas.

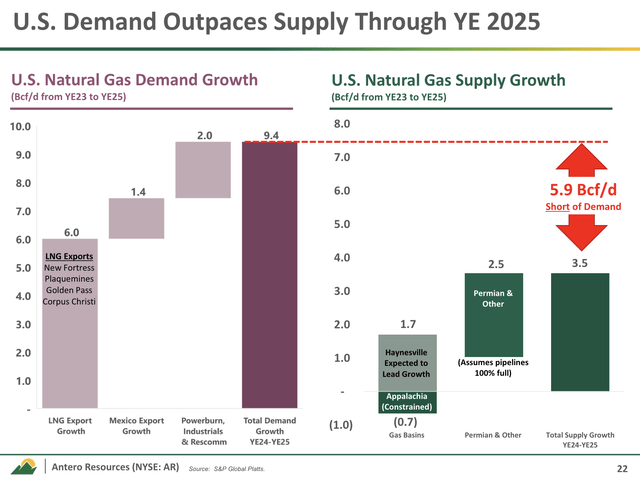

In general, export demand is very bullish.

Antero resources (New York Stock Exchange: R)the star of this article, estimates that growth in LNG (liquefied natural gas) exports will account for 6 billion cubic feet per day of new demand through 2025. When adding higher domestic demand and more exports to Mexico, the company believes there will be a shortage In supply at approximately 6 billion cubic feet/day.

Antero Resources

This is very bullish and is one of the reasons why natural gas prices are starting to recover.

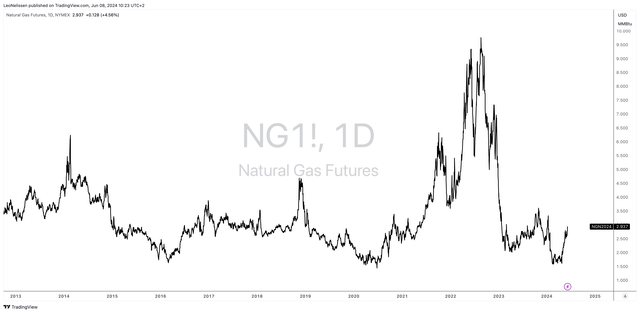

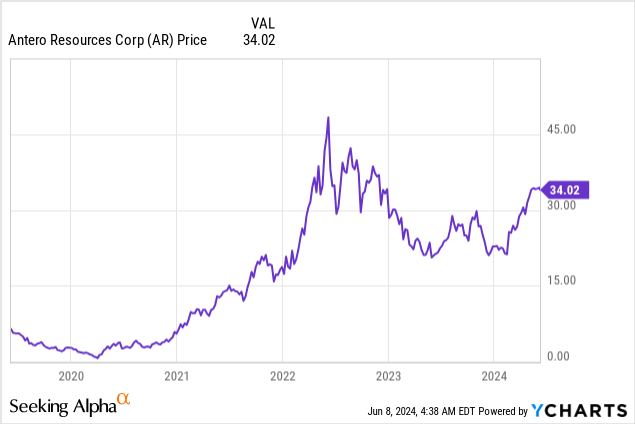

Although prices have not yet returned to normal, the momentum we are seeing is really great.

TradingView (NYMEX Henry Hub)

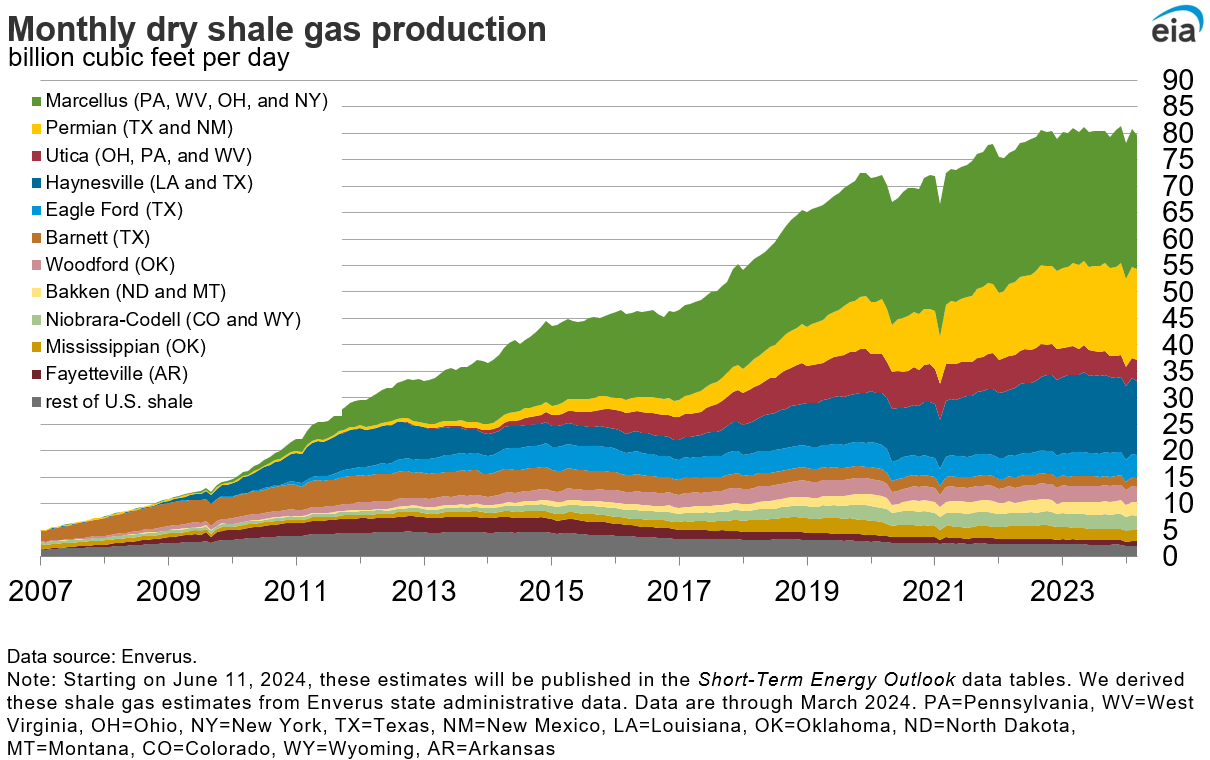

However, the supply side has generally changed, as the shale revolution has provided the United States with unprecedented growth in natural gas production.

Now, that’s over.

Although natural gas is still abundant (especially compared to oil), output growth has slowed significantly.

Energy Information Administration

In light of these changes, Goering and Rosenkoag explain that we are about to see a significant change in inventories, allowing prices in North America to converge with much higher global prices.

The United States is expected to shift from a prolonged period of severe oversupply to a structural deficit of historic proportions. Although stocks are still high, our models predict that they will reach dangerous levels much sooner than anyone thinks. Against this background, it is incomprehensible to us that natural gas in the United States is trading at a record discount compared to the energy equivalent price, even if we take into account two consecutive mild winters. Investors should take note.

Essentially, the end of the shale revolution meets the fastest natural gas demand growth in history.

Back to Goering and Rosenkoag:

Although we are very early, we believe that North American natural gas, with less liquefaction and transportation, will converge to the global price, which is currently $10 per mmcf. Investors are very optimistic after two consecutive mild winters but are ignoring the upward shifts in both supply and demand currently underway. This is the most heterogeneous investment we can remember.

This is where Antero Resources comes into play.

Why I’m so bullish on Antero Resources

I have been bullish on Antero Resources since I began coverage in 2023.

My last article was written on February 19, when I went with A Solid deal evaluation.

Since then, shares have risen 43%, crushing the S&P 500’s 7% return.

I think this is just the beginning, as AR brings some qualities to the table that make it an ideal stock to take advantage of the natural gas bull case.

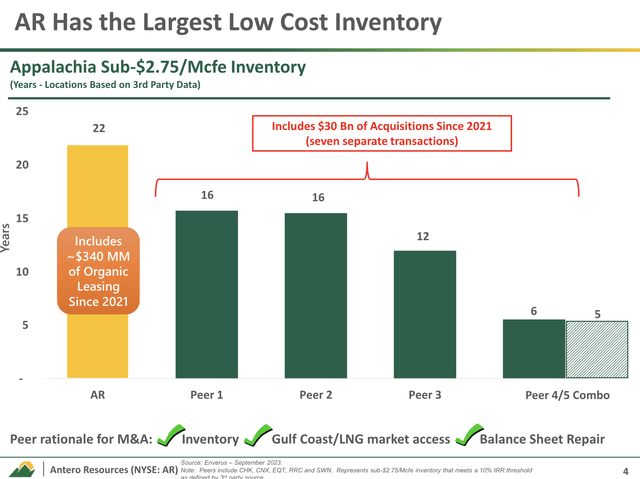

For starters, the company has over 20 years of premium stock in the Marcellus Basin (Appalachia), where it has become one of the most efficient producers.

To be precise, excluding new developments, the company has 22 years of inventories below $2.75 per million cubic feet (2.85 million Btu – Henry Hub unit).

Antero Resources

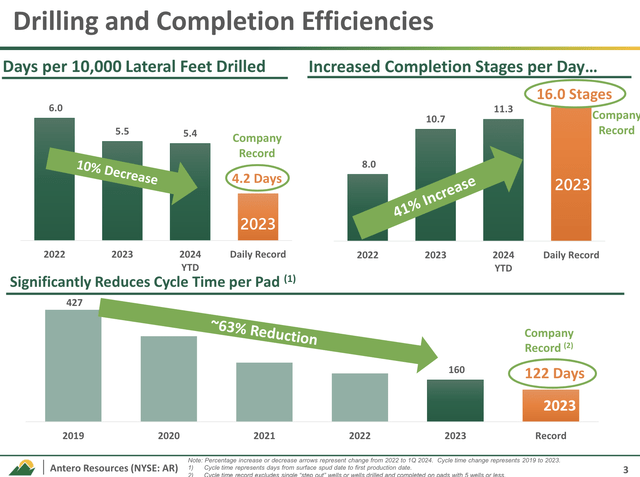

In its basin, the company enjoys high efficiency.

For example, in the first quarter of this year, the company reduced drilling time per 10,000 lateral feet to 5.4 days. This is less than 5.5 days in 2023.

Furthermore, Antero set a record for completion stages, averaging 11.3 stages per day. This compares to just under 11 stages per day the previous year.

Antero Resources

The company has also optimized new completion technology to save more than an hour of pumping time each day, and leverages Antero Midstream’s (AM) advanced water infrastructure to reduce congestion.

This infrastructure also eliminates the need for water trucks.

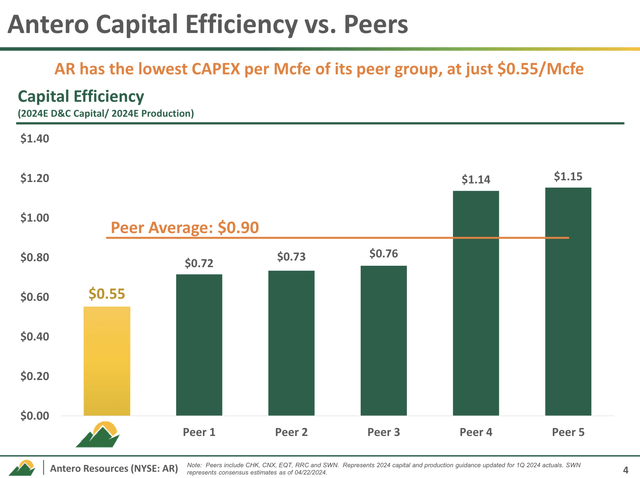

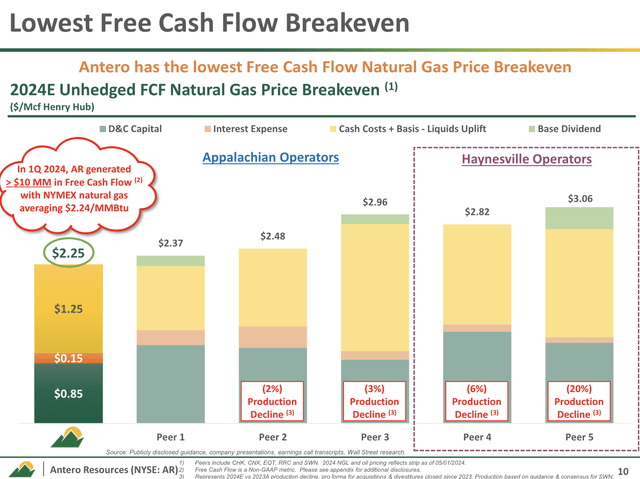

Overall, the company outperforms its peers in capital efficiency, as it requires only $0.55 per Mcfe to maintain production. The peer rate is almost double!

Antero Resources

On an unhedged basis, the company broke even at $2.24, which outperforms its major peers — especially those in higher-cost basins like Hinesville.

Antero Resources

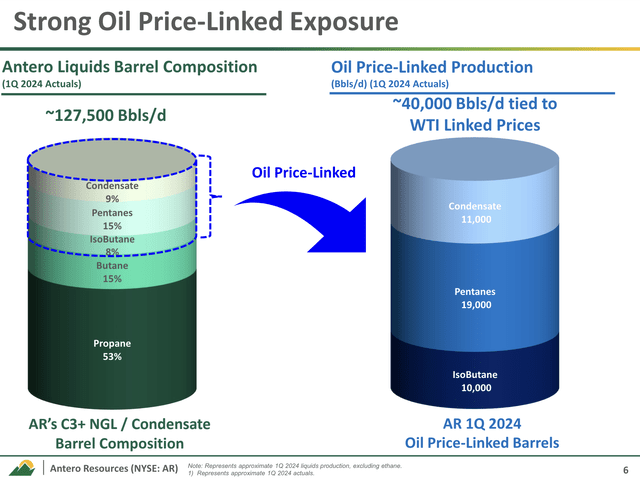

Furthermore, AR has another key advantage: its product mix.

While AR is a natural gas producer, not all of its production is low-margin natural gas.

The company has a large footprint in the liquids and natural gas liquids markets.

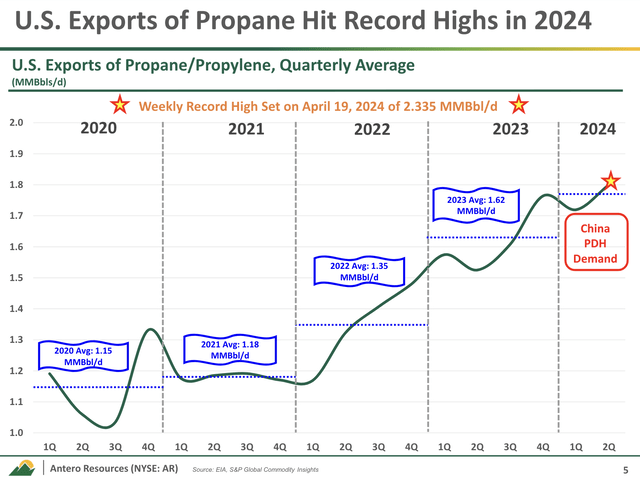

In the first quarter, U.S. propane exports rose to an all-time high of more than 2.3 million barrels per day. This represents a 14% increase compared to the 2023 average.

Antero Resources

This export growth, combined with strategic pricing decisions, has allowed Antero to obtain premium prices for its goods.

For example, propane prices as a percentage of WTI averaged 44% in early 2024. That’s up from 36% in the fourth quarter of 2023.

In addition, Antero’s decision to sell a larger share of its waterborne barrels in international indices rather than long-term domestic deals sees it benefit from better international prices.

Antero Resources

My point here is that AR is not a natural gas producer and relies primarily on Henry Hub prices in its own basin.

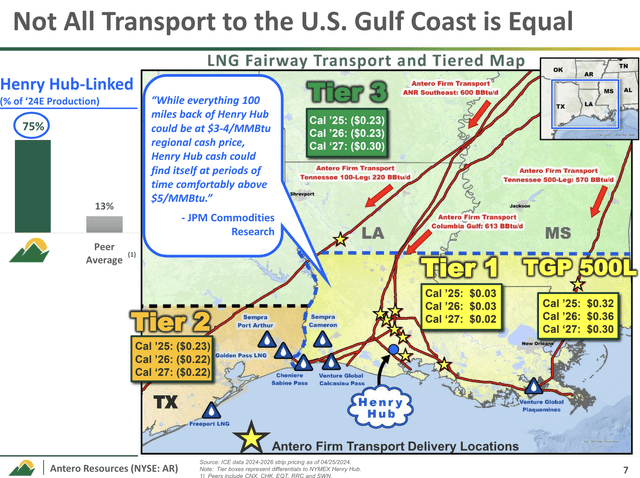

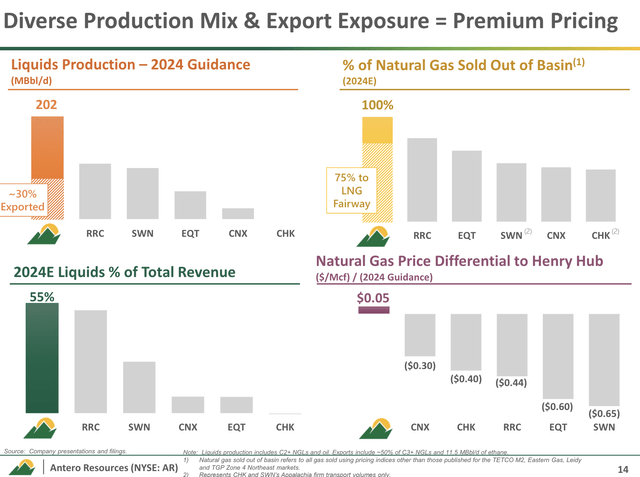

Better yet, the company is a major player in the LNG space, selling nearly 75% of its natural gas from its basin — mainly to the LNG corridor along the Gulf Coast.

As one can imagine, this puts the company in a great position to reach higher prices and capitalize on rapidly growing global demand for LNG.

Using the company’s own data, its peers sell only 13% to the LNG corridor.

Antero Resources

Furthermore, there are three other major benefits.

- More than half of the company’s production consists of liquids.

- It is the only major U.S. natural gas producer that is expected to sell its gas at a higher price than Henry Hub.

- It sells 100% of the natural gas from its basin.

Antero Resources

I believe these qualities distinguish the company as one of the best natural gas stocks on the market.

Shareholder benefits

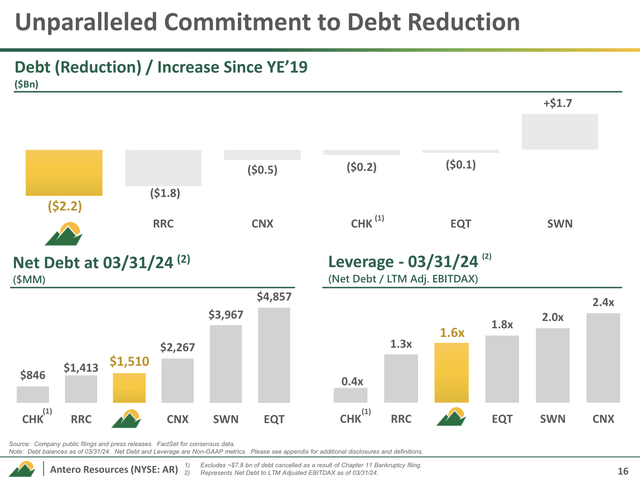

In addition to a great business model, the company has spent the last few years aggressively reducing debt.

Its net debt currently stands at $1.5 billion. That’s less than half of its 2020 debt load. It also has no debt maturities until 2026 and a leverage ratio of less than 2x EBITDA.

Antero Resources

Going forward, the company’s strategy includes reducing total debt and allocating future free cash flow to stock buybacks to further improve shareholder value.

Doesn’t pay dividends.

While AR may not be great for income-focused investors, it has huge free cash flow potential.

This year, based on the current market environment, analysts expect the company to generate $290 million in free cash flow. This is a large number, considering how pessimistic natural gas prices are.

It translates to 3% of the $10.6 billion market cap.

Next year, that number is expected to rise to $1.1 billion, or more than 10% of its market value.

If natural gas prices rise above $5 at Henry Hub over time, the company has the ability to buy back shares at an unprecedented pace, significantly boosting the value of a single share in the company.

Given the company’s free cash flow potential at Henry Hub’s $3, I think we could be looking at a free cash flow yield of 12-16% in an environment where natural gas prices are consistently rising in the $4 to $5 range – depending on growth plans.

This also means that I expect AR to outperform the Energy Index ETF (XLE), as I consider the natural gas bull case to be significantly underappreciated.

So I stick to A Solid deal rating, as I expect the market to discover the appeal of augmented reality and its peers – especially once global economic growth improves.

Personally, I have been holding AR shares since last year – with a good profit. However, I sold because I closed my entire trading portfolio. I decided to move my cash into my long-term investment portfolio — for a wide range of reasons.

Now, I’m looking at the best way to incorporate non-dividend paying stocks into that strategy.

Needless to say, given how much I love AR, I’m looking forward to making it a “permanent” site in my long-term portfolio in the coming weeks and months.

So, please do not confuse me that I am not disclosing a long position in AR at this point.

I invested in Antero Midstream – not Antero Resources.

He stays away

The future of natural gas looks incredibly promising, driven by rising demand associated with artificial intelligence and broader market trends such as LNG exports and the ongoing shift from natural gas to coal.

Here, Antero Resources stands out as a top pick due to its impressive efficiency, strategic location, and strong financial health.

With significant reserves in the Marcellus Basin, low production costs, and significant exposure to attractive LNG markets, AR is well positioned to benefit from growing global demand for natural gas.

Moreover, the company’s focus on reducing debt and the potential for significant free cash flow in the future improves its investment attractiveness.

Pros and Cons

Positives:

- Strong stock and efficiency:AR has more than 20 years of outstanding inventory in the Marcellus Basin and leads its peers in capital efficiency.

- Strategic location: By selling 100% of the natural gas from its basin, AR improves its prices.

- Diverse product mix: Higher exposure to high-margin liquids and LNG also improves prices.

- Physical ability: Significant debt reduction and strong free cash flow potential provide low financial risk.

- Headwinds to growth: Unprecedented demand growth driven by artificial intelligence, the shift from coal to gas, and the rapid growth of liquefied natural gas exports.

cons:

- No profits: AR does not provide income through dividends.

- Market fluctuations: Natural gas prices can be volatile, making AR much more volatile than the “average” stock you may have invested in.

- Industry risks: Regulatory changes and environmental concerns can impact its operations and end markets.