com. aluxum

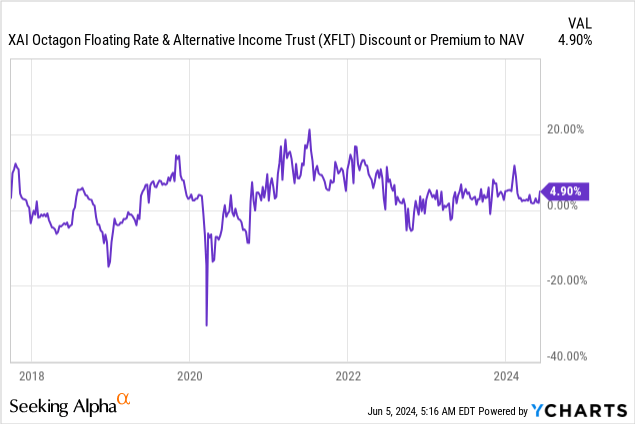

XAI Octagon Floating Rate and Alternative Income Fund (New York Stock Exchange: Exvelt) offers a total return tactic with an emphasis on income generation. This is very common among closed-end funds, or CEFs, where income generation is a very popular topic. The appraiser is trying Achieve this goal by investing in private credit. A category that is growing in popularity. Assets under management add up to $680 million (achieved at a leverage ratio of 38%). The fund trades at a premium of 4.9% to NAV, and offers an attractive distribution ratio of 14.01%.

XFLT has traded mostly at a premium since its inception:

I don’t like buying closed-end funds at a premium to NAV. I rarely do that, if ever. In keeping with my philosophy when investing in these funds, I was skeptical of my coverage of XFLT. However, since my last articleXFLT has managed to keep up with the S&P 500 (spy) which has been an unstoppable force for many years.

I do not want to repeat the points I made in my previous writing, but I will mention them briefly and then introduce some new developments.

- This is a leveraged fund that invests in leveraged loans (leverage is great when it works, but it can work against you)

- The fee on net assets (before interest expenses) is approximately 3.9%.

- Charges on net assets including interest expense are approximately 8.6% (5.13% on total assets)

- Interest is relatively low because it includes leverage obtained at fixed rates prior to the 2022 interest rate hike cycle.

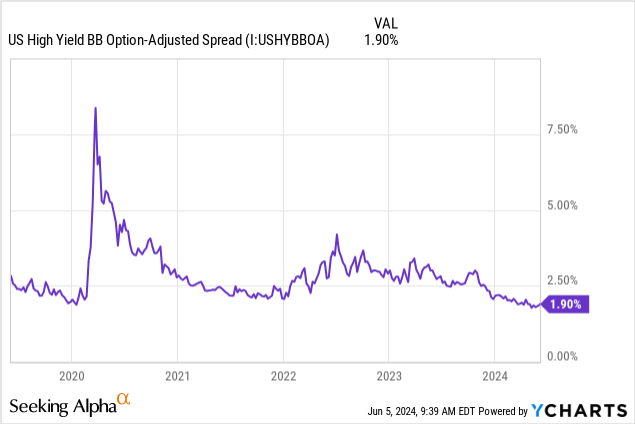

The reason I’m a little conscious of leveraged funds investing in leveraged loans is because we’re in a very complacent environment. Maybe, just like the Fed bailed out high yields in 2020. Maybe it’s okay for high yields to have such a narrow spread over Treasuries. It’s not a unique case, but it’s rare to reach this level.

The fees appear justified due to the work on the special assets and excellent performance. To some extent, they can be. In my humble opinion, this level of fees is very likely to be a drag on long-term performance. It seems a bit unlikely, though not impossible, that the management team can consistently generate enough alpha in leveraged credit to fully offset it.

What I’m particularly concerned about is whether the fund can maintain its leverage ratio as the Fed pushes. The latest news is that it remains “higher for longer”.

One thing that makes a lot of sense to me is reducing the leverage ratio from 41% to 38%. A bigger discount would have made sense to me too.

Another positive development is that the fund has raised additional capital to help replace its 2026 preferred shares over time. I was amazed that they kept a ~6% rate on a small release for 2029. However, these are my favorites for conversion. The coupon is only 6%, but the owner has the option to convert it into shares at market price or net asset value. The latter option means that even if shares trade at a 50% discount to NAV (which currently seems unthinkable), these investors simply get twice the amount of shares to cover their entire investment. Obviously, this would dilute the remaining shareholders. It’s just a small increase in capital, but this option is usually not without value. For example, the average closed-end fund is currently trading at a discount of 6.51%. Most closed-end funds end up trading at a discount at some point.

The fund also raised some capital by issuing shares. It did so at a premium to NAV, and this practice is actually cumulative for investors who bought at NAV. You can also say that it reduces risk for other investors because it improves the leverage ratio. XFLT has issued shares at various times, and so far, that hasn’t completely eroded its premiums. In theory, it dilutes anyone who bought at the higher price (104%+). I think this is a wise move under the circumstances, but I am opposed to paying a premium.

The final thing I don’t like is that the box has lost its expiry date and is now a permanently sealed box. A fund with an expiration date expires (in this case in 2029) and investors are guaranteed to get their capital back at some point without a long and expensive activist campaign. This can support the fund from trading at a very significant discount because over time, the termination date and realization of NAV approach.

In conclusion, over the long term, I remain skeptical of the 14.01% proprietary distribution rate and premium to NAV that the fund trades at. The Fund has begun refinancing its beneficial sources of leverage. However, equity issuance and convertible issues help mitigate the short-term impact of this high rate environment. However, in doing so, the Fund assumes certain risks that will only materialize in the future if this occurs. Juicy distribution rate. However, if there is an explosion in high yield spreads and there is a serious drawdown, the NAV could decline by approximately 50%. In 2020, the fund went from a +15% premium to a nearly 30% discount. If you then have convertible shares that dilute the stock, the erosion of value from here can become staggering. Although the fund has de-risked a bit, I believe this has been negatively offset by the move to its perpetual position. I will adjust my rating to sell.