Douglas Racing

the iShares 20+ Year Treasuries ETF Buying Strategy (Bat: TLTW) is designed to give investors exposure to 20-year Treasury Bonds (US20Y) with increased income by writing monthly call options on the underlying asset. for me The basic assumption of these more complex products is to keep the simple version. As of May 24, iShares put the distribution yield at 11.58% while the 12-month trailing yield added up to 16.61%. The problem with these income-focused products and their attractive returns is that there are usually risks associated with them.

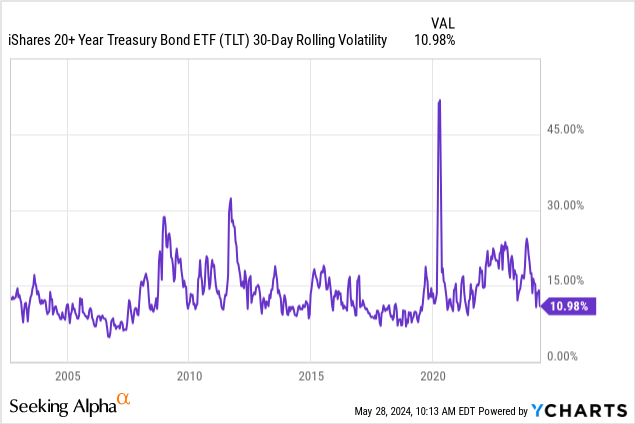

Here lies the volatility in bond markets, which has increased in size over the past few years. Since this is a product where the upside is sold (through calls), the main risk is that the bonds rise tremendously, and you miss out on most of that. Due to low volatility in bond markets, the constant return (derived from… Coupons (but mostly from selling options) go down at the same time.

In my previous article on TLTW, from February 2024, I said it’s not clear to me where bonds are headed. I still don’t have a strong opinion. I lean toward higher bond yields over the long term.

Being a long term bond, with at least some yield, selling calls seems a very reasonable position to me. They make a lot more sense than outright long bonds. Right now, I think TLTW is a better option than TLT. This won’t be the case forever. If implied volatility comes in, most likely as realized volatility dries up, selling the call will yield much lower returns. It also means that returns of 16% will not be achieved, even if the bonds remain stable, because selling futures calls is likely to take place at lower levels of volatility. At lower volatility, I would reconsider whether it is still worth the increased management expense versus a simpler TLT fund.

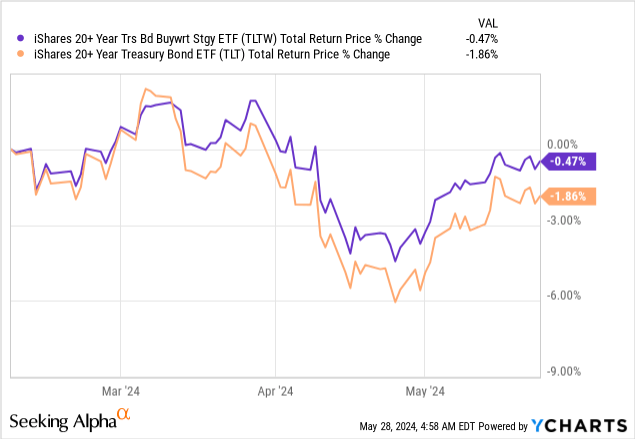

TLTW has outperformed TLT ever since, although neither has performed as well:

The return based on current volatility levels is significantly lower than it was at the time. At the same time, we have made some big moves and the Fed has been clear that they are not about to cut. Meanwhile, we are moving into a generally quiet period (ie summer). Most importantly, the pending banking crises that followed the cycle of rapidly rising interest rates appear to have ended and the region is recovering:

Realized and implied volatilities have decreased:

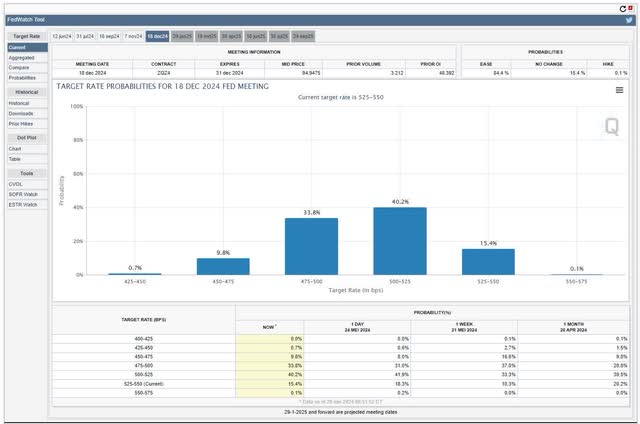

Back in February, CME Fedwatch showed how bond markets were biased towards upcoming cuts. That has changed, and even a rate hike is under consideration:

CME Fedwatch tool (poison)

What I like about this more balanced view is that if things turn out to be the opposite direction, you don’t experience a very volatile move.

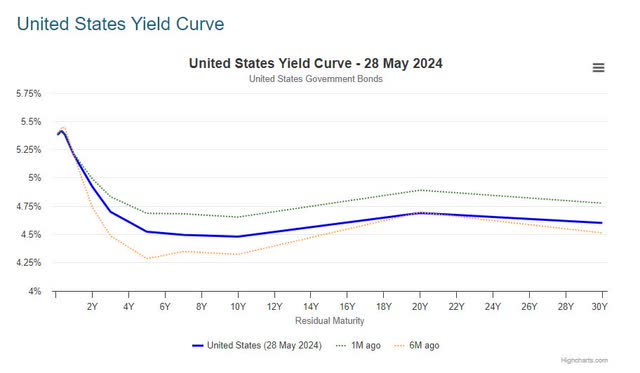

The US yield curve has been inverted since July 2022. We are in for two years now. The yield curve is a signal of recession and has historically been very successful. On average, recessions follow a reversal within 12 months. But in 2006, it took 22 months before a recession hit.

US yield curve (worldgovernmentbonds.com)

This continuous shape of the yield curve is very noticeable. It’s counterintuitive that you’ll be able to get a higher return when you lend your money for a shorter period of time, but here we are. Although I don’t have a strong long-term conviction, bills were one of my favorite investment ideas for 2024 and continue to be. Primarily because of the high return in both an absolute and relative sense.

My conclusion is that TLTW is at best on hold here. I liked this ETF as a relatively easy way to profit from increased bond volatility. In terms of fees, it is 0.35% per annum, which is in line with this category. It is high for a bond fund, but modest for a strategy that involves overlaying options. Right now, there aren’t the same volatility-rich bonuses to support future results.

It seems quite unlikely, although nothing is impossible, that we will see a similar percentage of 16.61% in the future. The realized return will likely drop into the single digits. Otherwise, the risk profile is asymmetric against us. I don’t like the long bond position because of the yield curve, but TLTW will only rise marginally anyway because he’s selling calls. On the other hand, if bond prices decline, the losses are very similar to a long TLT position.