Diverse photography

Zoom Video Communications Company (Nasdaq: ZM) has been one of the most exciting stocks during COVID-19. Zoom helped spark an online revolution as the coronavirus swept the world. Zoom’s extremely easy-to-use platform has made it possible for millions of people to hold meetings online, and The stock rose significantly during this hypergrowth phase. Zoom’s stock price has risen tenfold within a year, achieving an ATH of approximately $575 in 2020.

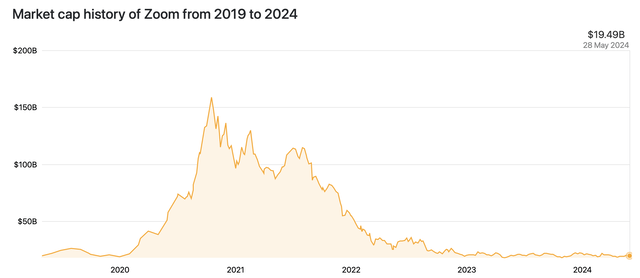

Zoom’s decline, on the other hand, has been epic. Its stock price fell a staggering 90% from peak to trough, bottoming out at around $60 in the fall of last year. The destruction of Zoom’s market cap has been nothing short of astonishing, as its stock has fallen from a high of over $150 billion to only about $20 billion today.

Market Cap Zoom (companiesmarketcap.com)

The good news is that Zoom stock has stopped falling. Zoom’s market cap has been trending sideways ever since Almost two years, a very positive dynamic that indicates that Zoom is going through a long-term bottoming process after an almost two-year downtrend.

Moreover, Zoom has finally developed an obscene rating. When it was trading around its peak, Zoom stock’s price-to-sales ratio was about 260. Now, Zoom stock is trading at about four times sales. Zoom has also become very profitable and very cheap, with a P/E ratio of only about 12.

Zoom is also consistently beating analyst estimates and could significantly increase its sales and profitability as we go forward. Therefore, Zoom stock could rise as the company improves its growth, efficiency, and profitability metrics in future quarters.

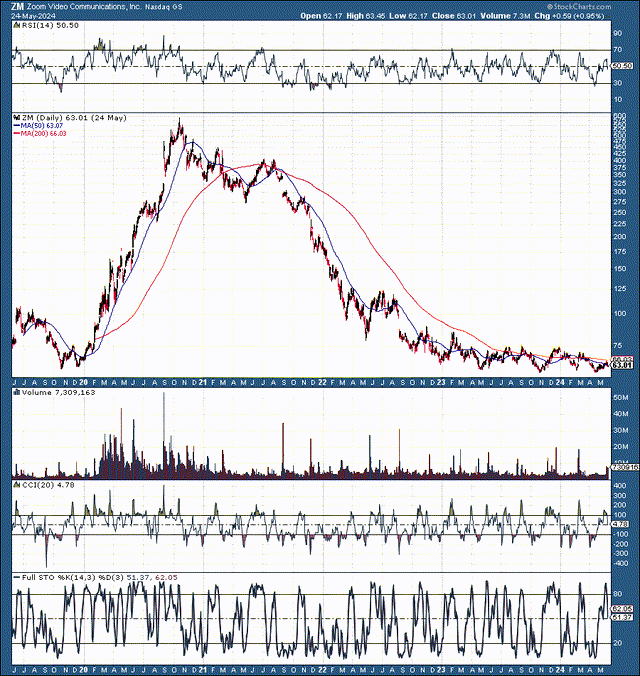

Technically, there is likely to be a long-term bottom

ZM (StockCharts.com)

We see a decline of about 90% after Zoom reached its peak. While this may seem extreme, we have seen a similar dynamic with many stocks. Zoom is recovering more slowly than other companies, which presents us with buying opportunities. However, just as Zoom stock became very expensive during the peak, it is very cheap now. While we may see more volatility in the near term, Zoom stock is likely to rise significantly in the medium to long term. We have seen a sharp expansion, then a peak, followed by a sharp decline and nearly two years of consolidation, and we could see another round of growth and expansion ahead.

Recent earnings have been strong

Zoom recently reported better-than-expected earnings results for the first quarter. Zoom generated $1.35 in earnings per share, beating 16 cents. Revenue reached $1.14 billion ($10 million USD), an increase of 2.7% year over year. Zoom’s revenue increased 3.5% year over year when adjusted for the impact of foreign currencies. Enterprise revenue was $665.7 million, an increase of 5.3% year over year. Our GAAP operating margin was 17.8%, and our non-GAAP operating margin was 40%. Operating cash flow was $588 million, an increase of 40.6% year over year.

Zoom’s cash position has swelled to about $7.5 billion. Zoom also has very little debt and an enterprise value of only about $12 billion (nearly three times sales), which is very cheap. For the second quarter, Zoom expects revenue between $1,145 billion and $1,150 billion, slightly lower than the expected $1.15 billion. Fiscal year (FY2025) revenue guidance is between $4.61 billion and $4.62 billion, marginally lower than the $4.62 billion expected. EPS guidance for the fiscal year is around $5, slightly better than the EPS consensus estimate of $4.89.

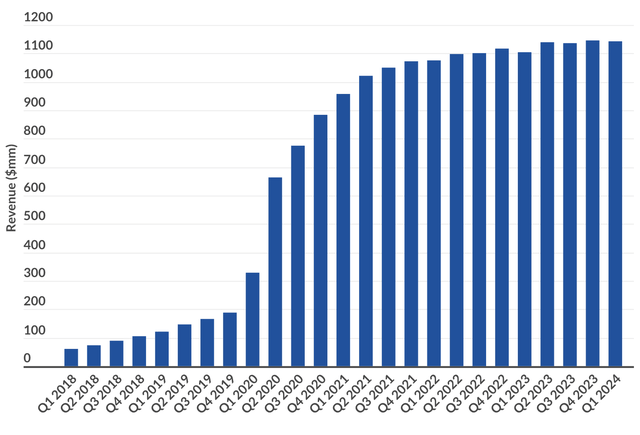

Zoom in on sales by quarter

Zoom sales by quarter (businessofapps.com)

While Zoom’s sales growth has stabilized, we may have an acceleration in sales and earnings. Zoom is the brand name. It’s like the Coca-Cola of the meeting/webinar world. Zoom is like Apple or Tesla in its space. In other words, Zoom is a market leader and can continue to lead innovation in its field. Zoom is similar to Google in its category. When we search for something on the Internet, we Google it. When we want to meet online or share a webinar, we say Zoom, not G Suite or anything else. Furthermore, Zoom will likely continue to beat consensus EPS estimates.

Zoom may not stay cheap for long

Zoom in transition. It has gone from a highly overvalued hypergrowth stock to a record “moderate/modest” growth technology stock. At the same time, Zoom is attractive because of its high level of profitability and its low valuation of just 12 times earnings, or about three times enterprise value. Also, Zoom has consistently outperformed and should continue to outperform consensus estimates.

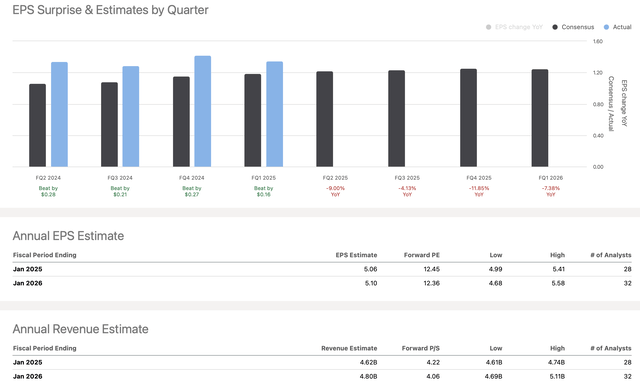

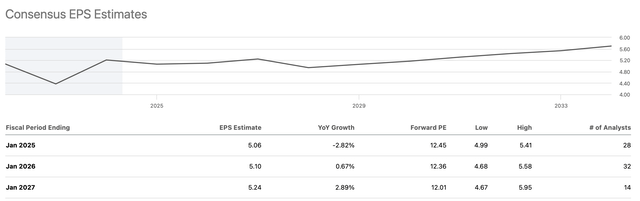

Zoom is likely to exceed estimates

Zoom beats estimates (seekingalpha.com)

Zoom has exceeded EPS expectations in all of the last 20 quarters. While this year’s EPS estimate is about $5.06, and next year’s is only about $5.10, Zoom could do better. The TTM consensus EPS estimate was $4.48, however Zoom reported a much better price of $5.40. So, we see an average outperformance of 20% over the last four quarters, and it looks like Zoom can easily beat the upcoming numbers for 2024 and 2025.

Let’s assume Zoom beats consensus EPS estimates by a modest 15%. This dynamic suggests we could see EPS of around $5.82 this year and around $6 next year (fiscal 2026). If Zoom earns $6 next year, it will trade at about ten times forward earnings estimates now, which is extremely cheap for a company in Zoom’s market-leading position.

Zoom’s great AI capabilities

Zoom AI Companion is your AI-powered digital assistant. Zoom’s AI-powered companion delivers powerful real-time capabilities to help customers increase productivity and work together more efficiently. Zoom users can see AI Companion across the Zoom platform, with features for meetings, group chat, mail, and more.

By leveraging AI, Zoom can revolutionize the user experience, paving the way for increased efficiency and profitability. As a market leader, Zoom’s strategic advantage positions it for greater growth than the market expects. This dynamic could push its stock price to new heights.

Zoom stock likely has more potential than expected

EPS Forecast (seekingalpha.com)

Many analysts have very modest forecasts for EPS and revenue growth for the coming years. The market may be overly pessimistic about Zoom, and the company is consistently beating consensus EPS estimates by a large margin. The market expects a very modest sales growth of 3-5% in the coming years. Furthermore, the consensus estimates have almost no impact on EPS growth as we move forward.

However, Zoom’s EPS could increase more than expected if its growth improves slightly and its productivity and efficiency increase, leading to better-than-expected EPS growth. Also, Zoom has authorized a $1.5 billion buyback program, enabling it to increase earnings per share. Therefore, we should see better-than-expected EPS, leading to multiple expansions and a much higher stock price for Zoom in the coming years.

Where Zoom Stock could be as we move forward

|

Year (non-financial) |

2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue b | $4.7 | $5 | $5.5 | $6 | $6.4 | $6.9 | $7.4 |

| Revenue growth | 4% | 6% | 10% | 8% | 7% | 8% | 7% |

| Earnings per share | $5.47 | $5.85 | $6.32 | $6.88 | $7.45 | $8.20 | $8.91 |

| Earnings per share growth | 5% | 7% | 8% | 9% | 8% | 10% | 9% |

| Forward P/E ratio | 14 | 15 | 16 | 17 | 18 | 17 | 18 |

| Share price | $82 | $95 | $110 | $127 | $148 | $155 | $175 |

Source: The Financial Prophet

Although I’m using relatively modest estimates of mostly single-digit revenue and EPS growth, Zoom’s stock price could triple over the next several years by 2030. Zoom could post slightly better sales and earnings growth soon. This dynamic could lead to multiple expansions, resulting in a much higher price for Zoom stock.

The dangers of zooming

Zoom faces significant risks despite my bullish estimates. There is increasing competition in the meeting and webinar space. Major companies like Microsoft, Google, and others are present in this space and trying to gain an ever-increasing market share at the expense of Zoom. Zoom must continue to expand and needs to improve sales growth. Zoom must also maintain a high level of profitability, and any decrease in price to increase the number of users will reflect poorly on the company’s shares. Macroeconomic factors and other elements could also negatively impact Zoom stock. Investors should consider these and other risks before investing in Zoom.