Peter_Galea

Introduction: What makes a soft landing?

The amount of talk on websites, channels, and financial articles about A Soft landing Really impressive. A soft landing has a kind of immediate alarm effect for the market watcher.

With a purpose To understand whether a soft landing or some other kind is coming, we first need a clear definition:

“A soft landing means the economy is cooling down after a period of rapid expansion occurring smoothly.”

(It is the cooling that occurs smoothly, not the expansion. The expansion itself is likely to be warm and somewhat flammable.)

Investopedia offers its own definition:

“A soft landing is a periodic slowdown in economic growth that ends without a period of complete recession.”

The third definition, this one from former Federal Reserve Vice Chairman Alan Blinder:

“…if GDP declines by less than 1%, or GDP does not decline If a recession is declared at least a year after the Fed’s interest rate hike cycle, it is considered a soft landing.

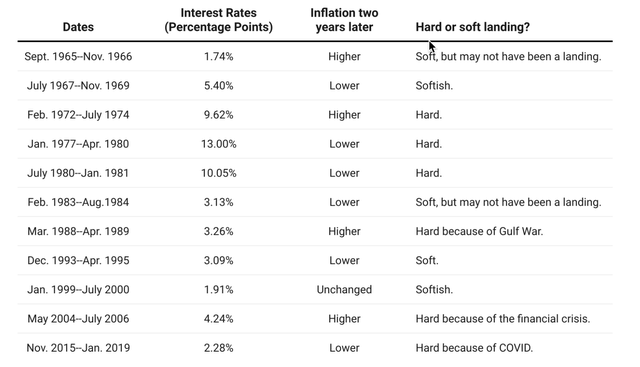

Here’s a historical example of a soft landing, from the same Brookings article that quotes Alan Blinder:

“The classic example of a soft landing is the monetary tightening undertaken under Alan Greenspan in the mid-1990s. In early 1994, the economy was approaching its third year of recovery after the 1990-1991 recession. By February 1994, the unemployment rate was falling rapidly, From 7.8% to 6.6%, the CPI inflation rate remained at 2.8%, and the federal funds rate remained at about 3%… The Fed was concerned about the possibility of rising inflation and decided to raise interest rates preemptively during 1994. The Fed raised interest rates seven times, doubling the federal funds rate from 3% to 6% and then lowering its key interest rate, the federal funds rate, three times in 1995 when it saw the economy contracting more than needed to maintain inflation. . to rise.”

Greenspan miracle Soft Landing suggests a few takeaways:

- A rapid recovery from a recession carries with it downstream risks. Very rapid expansions lead to bouts of inflation that can reach exponential levels;

- It is possible that a rapid decline in unemployment rates is a signal of an expansion that leads to higher inflation rates;

- Fear of inflation can lead to multiple interest rate hikes creating a “cure is worse than disease” syndrome.

Alan Blinder points out that he was there five Soft landing in 58 years.

Brookings Institution

The soft landing record is mixed at best.

The central bank simply does not exercise the same level of control over the economy that a pilot exercises on an airplane flight.

The Fed’s main policy tools – interest rates and asset holdings – are blunt. It does not address phenomena such as supply chain disruptions or pandemic disruptions. The recession followed the last five instances in which inflation peaked above 5% – in 1970, 1974, 1980, 1990 and 2008.

Former Fed Chairman Ben Bernanke described the difficulties of a soft landing with this metaphor:

“If making monetary policy is like driving a car, then a car has an unreliable speedometer, a foggy windshield, and a tendency to respond unpredictably with a delay on the accelerator or brake.”

Federal Reserve Policy and Soft Landing

The assumption behind this article is that the Fed is too focused on engineering a soft landing from the current expansion.

This assumption is supported by Fed Chairman Jerome Powell’s responses to questions at the January meeting of the Federal Open Market Committee (FOMC). As a reminder, the FOMC’s mission is to set the direction of monetary policy in the United States by directing open market operations (OMOs).

Asked whether the Fed had achieved a soft landing, “Jay” Powell replied that he “wouldn’t say we did.”

“We… are not declaring victory at this stage… It is a decision of great importance to start the process of lowering interest rates and we want to do it right.”

However, the Fed remains wary of inflation, and is certainly skeptical about a downward trajectory in the economy Increased inflation rate I will continue.

Second round of inflation?

The risks of renewed inflation pose a major obstacle to the initiation of interest rate cuts by the Federal Reserve. This issue was discussed in a CNBC segment with Jason Trinnert of Strategas Research Partners.

Trinaert pointed to the news that Minneapolis Fed President Neel Kashkari did not want to say in a recent interview that the Fed would start cutting interest rates. Instead, Kashkari “retains ambiguity in the process.”

Trinaert believes Fed governors frequently talk about forward guidance, which confuses markets. The wealth of statements reinforces the idea of this The Fed doesn’t know the future any better than the rest of us.

This is because reading inflation is very difficult, in Trennert’s opinion. More importantly, inflation may have a second wind:

“…upward pressures on inflation continue, which are not going away any time soon…once you have a wave of inflation above 6%, you get a second wave…and the odds are about nine out of 10…”

Despite this confidence in what many may see again Inflation surpriseTrinert believes that Jay Powell and his colleagues are committed to a pessimistic path and will start cutting interest rates in September this year.

Evidence of the slow shift toward dovishness is the easing of tensions Quantitative tightening This was a partner in interest rate increases.

“…The Fed has been allowing up to $95 billion a month in proceeds from Treasury securities and mortgage-backed securities to mature each month. This process has reduced the central bank’s balance sheet to about $7.4 trillion, or $1.5 trillion less.” From its peak around mid-2022.”

“Under the new plan, the Fed would reduce the monthly limit on Treasury securities to $25 billion from $60 billion. This would put the annual reduction in holdings at $300 billion, compared to $720 billion since the program began in June 2022.”

The Fed has stopped aggressively throttling liquidity, and is instead gently reducing it. He has expressed his intention to end quantitative tightening soon.

What do the markets say?

The trajectory of stock markets provides some guidance on the likely path to a soft landing. Markets are where institutional and individual investors place a large share of their assets, so the state of the markets reflects macroeconomic realities, including inputs from central banks.

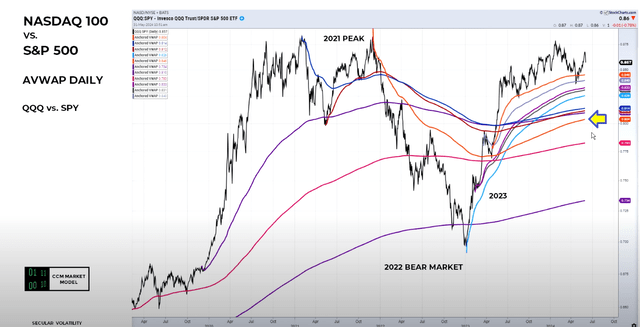

Hedge fund manager and market historian Chris Ciovaco, who prepares weekly technical presentations of market patterns in historical contexts, gave another interesting presentation last weekend. Ciovaco points out that the markets are uncertain, but leaning toward the upside.

One chart-based bull market indicator shows the Nasdaq versus the S&P 500 in a five-year flow, with resistance lines crossed by the path of the moving averages. Evidence points to continued strength in the current bull market.

Chris Ciovaco Show on YouTube

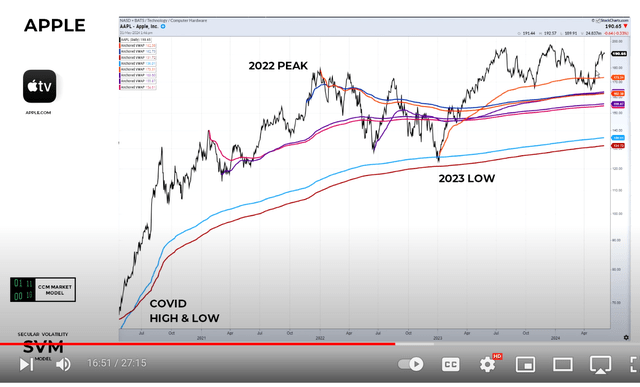

The performance of a leading company like Apple Inc. (AAPL) further confirms the confident nature of this bull market:

Chris Ciovaco Show on YouTube

Apple is a leader and great technology stock, and its performance has been questioned by market watchers. It has just recovered nicely from its recent low. Rather than being a stalled leader that encourages broader market weakness, Apple is a strong, stable company that offers a reason for hope.

BlackRock fixed income investment expert Rick Rieder adds his optimism about the markets to Ciofacco’s. In an interview by CNBC’s Scott Wapner about what a record market high means, Ryder responded positively:

“The technicals in the stock markets are amazing… and the earnings are very good… and you’re still doing 18 or 19% ROE (return on equity) for an average S&P 500 company, which is very impressive.” “

Rick Ryder stresses the importance of techniques and signals like massive stock buybacks, Nine Trillion dollars in cash, and the ongoing wealth creation of individuals and individual investors through vehicles such as 401Ks. He admits what he described as “consumer moderation” But again he points to the big ROE numbers as bullish confirmation.

Ryder then expects another 10% to 15% rally in stock markets by the end of the year — partly due to one or two more expected Fed interest rate cuts that would provide a “boost” to markets.

It also downplays the effects of current “high” interest rates. Reeder points to the huge amounts of cash available at many large and profitable companies; They actually benefit from higher interest rates in the form of interest on short-term fixed instruments.

The sensitivity of companies to interest rates does not ring true when it comes to blue chip companies. In the words of Rick Reeder, they are “more sensitive to interest rates than ever before.”

Famed “Big Short” money manager Steve Eisman, director of private wealth at Neuberger Berman, presented his own market analysis and forecast on Bloomberg TV. Eisman predicted that Donald Trump would win the November elections, and believed that the result would be clear by the time the Democratic Convention was held in August.

Once the election result is clear, investors will invest their money in the business. He does not believe that Trump’s potential tariffs on China will materially affect the US economy, which he describes as “…the most insular economy of any economy in the developed world.”

Eisman is also confident that Trump will not roll back the Biden administration’s large-scale spending, given that half the money currently goes to “red” states. Therefore, economic policies will not change much.

Steve Eisman is not concerned about the impact of the growing federal deficit on markets. Although predictions of a deficit disaster had been coming for “forty years,” the disaster did not happen. Don’t expect one any time soon.

summary

At the beginning of 2024, market watchers expected up to seven interest rate cuts. They believed that a shift to decisive Fed policies was inevitable.

What happened instead is that the Fed slid from its hawkish stance to one that could be called hawkish Neutral waiting to go dove.

This slow drift through neutrality toward a fickle version of dovishness is partly a function of the Fed’s awareness of “steering” limitations (“…the car…has an unreliable speedometer, a foggy windshield, and a tendency” to respond unpredictably and with a delay in accelerator or brake pedal”).

Furthermore, I think the Fed is concerned about the potential for inflation Second round Raised by Jason Trainert. If that happens, the cautious shift will quickly be replaced by renewed militancy that could arise in some very uncertain scenarios.

However, macroeconomic and market factors remain largely positive. Economic and market conditions are better than many realize, as Ciovaco, Ryder, and Eisman express convincingly and clearly.

The Powell-led Fed is aware of Ben Bernanke’s heavy lifting and will steer it carefully. The chances of a soft landing are reasonable, despite the challenges, obstacles, and risks along the way.