themacx/iStock via Getty Images

Inspired by the ultra-high yields that fund sponsors know investors can’t resist, we’re seeing a mad rush to increase distribution at market highs that wouldn’t normally be a cause for concern. if The funds were seeing their net asset value grow to Support those increases in distribution.

However, unfortunately, this looks more and more like an effort to keep up with the competition from high yield funds that can “offer” amounts as high as 50% Or more annual returns using options on the most popular and volatile stocks, mostly in technology.

ETFs such as… Yieldmax They fill the void of ultra-high-yield funds so that investors feel like they’re not just beating inflation, they’re crushing it. But you have to ask yourself, do… 50% Or are high yields a gimmick or are these real?

Well, that depends on how the markets are Performance of individual securities. Generally this Yieldmax ETFs need a bull market so that long call options and put options written more than compensate for their writing communicate Options.

So far, that has worked well for options plays on technology stocks, although that will largely depend on each individual. Yieldmax The performance of the fund’s underlying stocks. But as we’ll see, just because an underlying stock is doing well, that doesn’t mean it is Yieldmax The box is in good condition as well.

As for mutual funds, I have always used what I consider to be the sweet spot for NAV returns (not necessarily market returns) to be anywhere from 7% to 9%. This is the range you can expect most CEFs to cover in one year and still see their NAV values grow or at least be maintained.

Of course, this depends on each fund’s income strategy, some of which are more aggressive than others. Although, as a general rule, any return to NAV in the CEF has expired 12% I would consider that a red flag that would make it difficult for the fund to cover without losing NAV. It is generally defined as destructive Return of capital.

So that’s the problem for CEFs. When ETFs “Advance” 50% Or more annual returns, how can they compete when 12% Are returns too aggressive in CEFs?

This may be part of the reason why we are seeing many fund sponsors significantly increase their fund distributions, although another part of the reason is due to activist investors looking to pressure CEF fund sponsors to try to reduce discounts and increase funds. Ratings.

Many income investors probably realize that Yieldmax The strategy is not right for them and is more aggressive than they are looking for. But there’s no doubt that these high-yield ETFs, and I’m going to subtract the high-yield ETFs from GlobalX And even boxes like JPMorgan Premium Equity ETF (JEPI) Also, they take investment dollars away from mutual funds.

I don’t want to spend a lot of time on Yieldmax funds, but I would like to point out some of what can go right and what can go wrong in these funds that are considered risky.

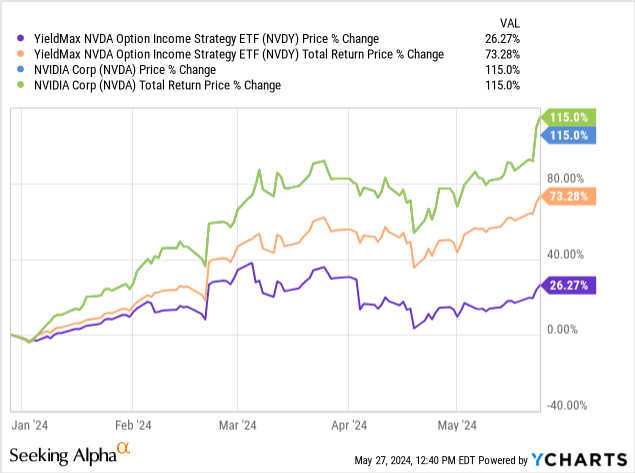

Take for example a success story like YieldMax’s NVDA Option Income Strategy ETF (NVDY), $28.55 market closing pricewhich is up 73.3% YTD.

It may be much less NVDA Total return 115% To date, from $495.22 At the end of last year to Friday’s closing price $1064.69but I want to draw your attention to the increase in the market price of NVDY by +26.3% To date, from $22.61 to $28.55:

That means if you remove the five massive dividends NVDY paid this year by adding up to $8.58 per shareyou’re looking at a much lower rise in pure prices +26.3% Compared to NVDA’s common stock appreciation of +115%. This is a big difference, and it is certain that the majority of NVDY’s gains this year are due to its options strategy and not necessarily to NVDA’s gains.

The current yield of NVDY is +50.3% Based on the most recent NVDY annual distribution for $1.1988 per share in May. But this distribution (and return) can vary widely $0.626 per share In January l $2.6219 per share in March.

In other words, there are a lot of variables that can occur when using options instead of investing in the underlying stock. There are strike prices, there are expiration dates, there are long options and short options (written) that these funds use.

Keep in mind that Yieldmax The Funds do not own any shares of its underlying stock. All gains or losses are due to their options strategy. In fact, most Yieldmax The fund’s assets are actually invested in U.S. Treasuries, securities, and bonds, so I wouldn’t be surprised if many of NVDY’s shareholders or any shareholders Yieldmax The funds believe this is a more conservative way to play NVDA and that it may provide some downside protection, as many discretionary income mutual funds do.

Unfortunately, writing put options is… no Defensive and actually opens the fund up to having to buy the stock at the strike price if the current price is lower at expiration. More on that below.

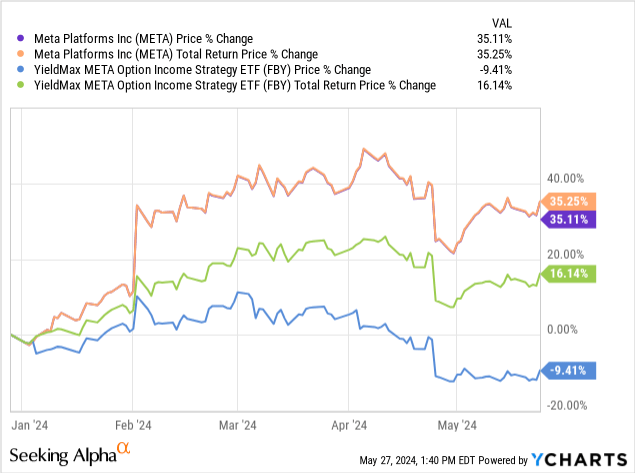

NVDY has certainly been Ben’s success story Yieldmax Money, but what happens when you look at other highly volatile stocks such as… Meta Platforms (META), $478.22 market closing pricewhich didn’t perform nearly as well as NVDA, although it’s still in a good position +35.2% year to date.

Here’s how META performs (both with and without distributions) compared to YieldMax Meta Option Income Strategy ETF (FBY), $19.73 market closing pricethat it Yieldmax peer:

So, from the beginning of the year until now, the META has been raised +35.3% On a total return basis while FBY rises +16.1% On a comparable total return basis when you include the massive FBY distributions. These distributions, based on FBY’s most recent distribution in May, translate to +annual54.6% fruit.

That sounds very attractive. But look at what happens to the FBY market price without those dividends. The price of FBY has actually dropped -9.4% Since the beginning of the year $21.78 At the end of last year l $19.73 Last weekend. One might assume that if the underlying stock’s META is high 35% Since the beginning of the year, the market price of FBY may not have risen as much, but it should not fall.

I cannot determine why FBY is showing such a sharp loss in market price because I cannot see the strike prices and expiration dates in the previous months. But make no mistake. The timing of the expiration of the FBY option has been off and this may happen to any… Yieldmax Money since they all use the same put option, put put, and call option strategy.

In the case of FBY, it’s all about where the META stock price was in relation to the options strike prices at expiration. If the price of a Meta stock is not at the price that optimized the option strategy, the Fund may not cover its distribution.

It’s basically the same as Destroyer Return of capital (ROC) In CEFs. And the matter is more dangerous Yieldmax Funds because they write call options, meaning the fund will have to close the written trade at a loss if the stock price is below the strike price at expiration.

This is something contributors to Yieldmax Funds typically don’t have to worry about a bull market, though, FBY, but if we go into a bear or bear market, you’ll see for yourself how a put option strategy can backfire.

ETFs and mutual funds continue to raise the bar of returns and risks

Fortunately for mutual funds, they generally do not use a selling strategy. But then, discretionary income mutual funds don’t shoot for the moon either.

However, the risk for both ETFs and mutual funds is that they set too high a percentage of the distribution yield and fail to cover it. The result is an erosion of net asset value which means less capital to draw the next distribution.

Note: The market price of an ETF is essentially its net asset value, while the market price of a CEF fund can be higher or lower than its net asset value.

So when you see CEF fund sponsors significantly increasing their fund distributions, you should look at that

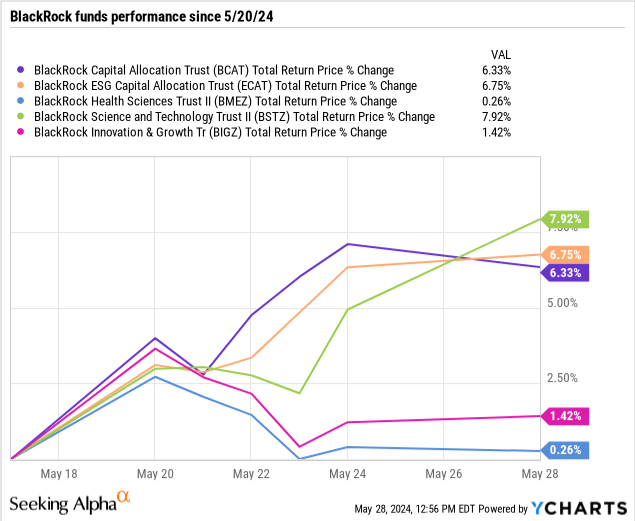

Just last week May 20BlackRock has dramatically raised distributions on several lagging mutual funds in an attempt to stave off this. Saba CapitalActivist investor.

particularly, Black stone Dividends raised BlackRock Capital Allocation Fund (New York Stock Exchange: BCT), $16.91 market closing priceand the BlackRock Environmental, Social and Governance Capital Allocation Fund (ECAT), $17.80 market closing pricemoving from fixed monthly distributions to a 20% To the net asset value distribution policy, which effectively increased the fund’s distributions +124% For BCAT and +98% for ECAT.

In addition, a new BlackRock group 12% Their NAV distribution policies BlackRock Health Sciences Fund (BMEZ), $15.16 market closing pricethe BlackRock Science and Technology Fund (BSTZ), $19.35 market closing priceand the BlackRock Innovation and Growth Fund (BIGZ), $7.50 closing market price, Reflects approx 100% Increases for those three funds as well.

Since that announcement, here’s how funds have reacted from the weekend closing price (before the open on May 20) to today’s price on May 28:

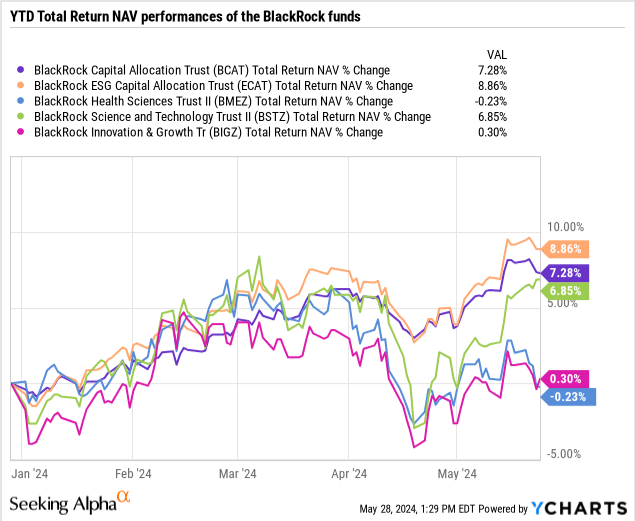

As you can see, there have been mixed reactions so far to the increases. why is that? Perhaps because BSTZ’s NAV is the only fund on pace to cover its increased distribution this year:

Keep in mind that all of these BlackRock funds use options to supplement the income they need to help cover their distributions. BMEZ, BSTZ and BIGZ write communicate Options on their all stock portfolios while BCAT and ECAT write currency options and actually buy long call options on stock positions as well as indices.

BCAT and ECAT also include fixed income in their portfolios. BCAT is 44.6% Fixed income and ECAT is 25.7% Fixed income.

Another fund sponsor recently raised distributions by as much as +60% This year it is Aberdeen. Equity mutual funds such as Aberdeen Healthcare Investor Fund (HQH), $16.69 market closing pricethe Aberdeen Life Sciences Investors Fund (HQL), $13.44 market closing priceand the Aberdeen Healthcare Opportunities Trust (THQ), $20.14 market closing priceit all witnessed drama He increases.

In fact, HQH and HQL have seen their distributions increase twice This year despite a net asset value performance that has since fallen into the low single digits.

Conclusion

Competition for investment dollars creates a race to see who can deliver the highest returns for income investors. This happens at market highs.

Maybe this could all work out if the markets continue their pace through the rest of this year, but I can’t help but think that this will all end very badly for many of these funds, despite the excitement about the raises.

Although I understand the motivation of trying to make their money more attractive in a crowded income market, to me this is an early warning sign that markets are driven by short-term incentives with longer-term costs.