Michael VI

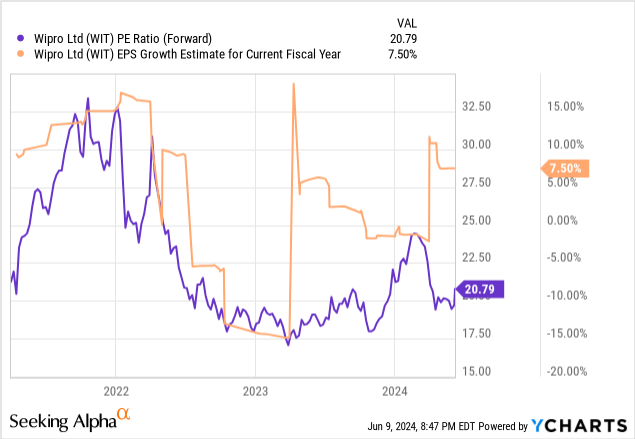

Wipro (New York Stock Exchange: witThe company has dealt investors a double blow in recent months, first with the resignation of CEO Thierry Delaporte and then with disappointing quarterly results. To be fair, many of the headwinds plaguing the industry are beyond management’s control, such as the interest rate Downgrade delays continue to hold down valuations and, in turn, cap technology budgets. But there have been enough signs of improvement in the global economy and IT deals, especially in AI, to make me optimistic about an eventual turnaround (which is the main reason why). My bullishness earlier this year). But what worries me is whether Wipro will be able to capitalize when things improve, especially with the added instability that comes with another reshuffle at the top management. Pending a further downgrade to a still expensive P/E of around 20x, I will sit on the sidelines.

Delaporte exit as CEO reshuffle continues

To some extent, the timing of former CEO Thierry Delaporte’s resignation came as a surprise, given that he had more than a year left on his contract. But given his performance so far, the decision was perhaps a bit less surprising. After all, under Mr. Delaporte’s leadership, Wipro has not caught up with its larger IT services peers in terms of growth or profitability, and the company has made little progress in winning major deals.

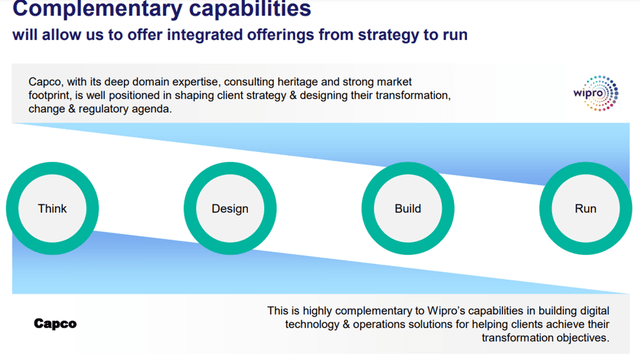

This poor performance comes despite Mr. Delaporte’s push for an inorganic growth strategy that has cost investors nearly $3 billion in recent years. For example, the $1.5 billion acquisition of business/technology consulting firm CAPCO did not yield synergistic results, while integration appears to be more difficult given the volume of post-deal sales (note that CAPCO CEO Lance Levy departed earlier from this year).

Wipro

This instability is not limited to the companies acquired by Wipro; In fact, this has been a constant sore point at Wipro during Mr. Delaporte’s tenure, with the last year alone seeing the departure of two senior executives (Chief Growth Officer Stephanie Trautmann and CFO Jatin Dalal) and several sector/business heads.

To be fair, the issue of management turnover goes straight to the top. After all, since the days of former CEO/Chairman Azim Premji, being CEO of Wipro has essentially been an “on and off” job – both for internal hires and, more recently, for external hires getting High compensation like Mr. Delaporte. Whether this latest CEO shake-up will change things is anyone’s guess, but for the foreseeable future, I wouldn’t rule out a greater management load in the stock price.

|

CEO |

a period |

External/internal |

|

Srini Baliya |

2024 – |

internal |

|

Thierry Delaporte |

2020-2024 |

external |

|

Obaidali Nemushwala |

2016-2020 |

external |

|

TK Corrin |

2011-2016 |

internal |

Source: Wipro Files

The focus shifts to execution under the new CEO

After disappointing results under previous external CEO appointments, it may be good news for Wipro to return to an internal candidate. In context, Srini Palia, a veteran with three decades of experience in the company, most recently as head of the “Americas 1” division (i.e. a mix of sectors in North America excluding Canada, as well as Latin America), will take the reins.

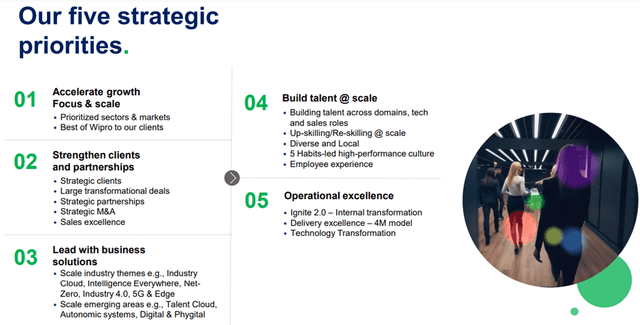

Although it is still early days, early indications from Wipro’s quarterly call (see “Five strategic priorities” below) is that the new CEO will prioritize execution over any new transformational shifts. For example, winning more large deals through a more comprehensive offering – also a key goal of former CEO Delaporte’s acquisition strategy.

Perhaps Mr. Palea’s most important task will be to contain the fallout from Mr. Delaporte’s sudden departure. Since Wipro’s current leadership still includes many employees from the Delaporte era, this will not be an easy task; However, this will be necessary to keep market tensions at bay.

Wipro

Near-term uncertainty looms large as the “kitchen sinking” begins.

The upside of executing on the switch is that Wipro will gain some much needed stability. The flip side is that investors likely won’t see a structural shift towards Wipro’s historical underperformance versus its industry peers either.

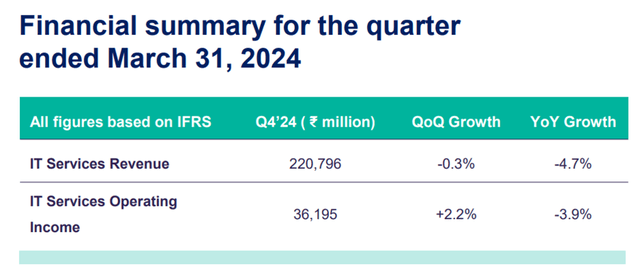

In the meantime, the stock will need to contend with new management reconsidering lowered (i.e., “kitchen sink”) forecasts over the next quarter or two. Remember, the latest earnings report has already seen Wipro disappoint and decline based on the limited vision of operational improvement. Compounding matters, according to management, is the challenging near-term demand backdrop amid “higher for longer” global interest rates.

Wipro

To be clear, I still believe the overall economy will improve, and that technology spending will eventually bottom out. But Wipro’s lagging P&L performance and additional uncertainties stemming from the departure of another CEO have me worried about its ability to capitalize. Therefore, for now, I would be cautious about securing any upside to the consensus forecast of a high earnings growth rate of no more than 10%; And I wouldn’t assign any prospect of Wipro narrowing its gap among its tier-1 IT services peers.

Shift stops

After becoming more bullish on Wipro to start the year, I am moving back to neutral following another reshuffle at the top. The appointment of new CEO Pallia is positive in the sense that it stabilizes the ship. However, it also entails a status quo scenario, meaning the company is unlikely to reverse years of lagging revenue growth/margin performance in the industry anytime soon. With a little stock in the price as well, I’m going away here.