Dekosig

2024 has been a great year for stock picking and sector rotations. While all the hype is still focused on Nvidia (NVDA) and technology (XLK), I’ve managed to get some good deals in lesser-known sectors like Services (XLU) And Consumer Goods (XLP). It may come as a surprise to know that the best-performing sector since the beginning of the year is not technology, but communications (NYSEARCA:XLC). This article discusses the reasons behind this strength and some concerns about XLC configuration.

SPDR sectors

I’ve really grown to love SPDR sector ETFs. They may not always have the best-performing ETFs in a given sector, and they’re less diversified than many other funds, but you know in advance exactly what you’re getting.

All SPDR sector ETFs are passively managed and have the same portfolio composition using a modified “market cap” methodology. Moreover, they are all liquid, and have… Large assets under management and share a very low expense ratio of 0.09%. SPDRs are a reliable and very easy way to move across sectors, or as the fund’s page states, “You can purchase eleven Select Sector SPDRs with a weighting consistent with the S&P 500 or use your own weighting to achieve specific investment objectives.”

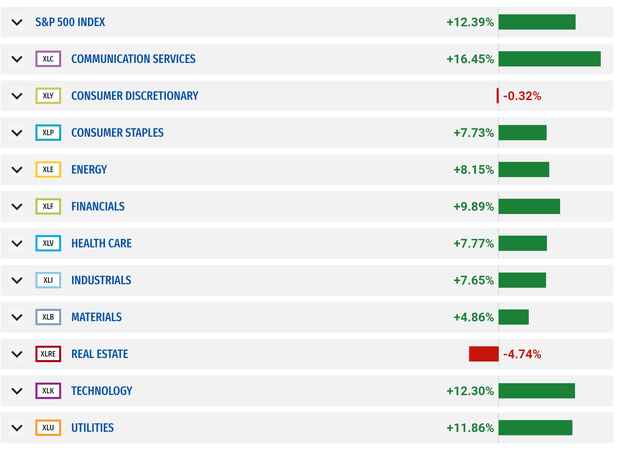

Here’s how all 11 ETFs have performed since the beginning of the year –

SPDR sector performance (Sector SPDRs)

As mentioned earlier, XLC leads the pack, and by a wide margin – trailing second place Technology by more than 4%.

Introducing XLC

XLC is a relatively new ETF that was launched in 2018 when major changes to the Global Industry Classification Standard (GICS®) were implemented.

We detail the largest-ever structural change in the Global Industry Classification Standard (GICS) in terms of market capitalization impact: the telecommunications services sector was significantly expanded and renamed to telecommunications services. This reflects the fact that the way people communicate, exchange and enjoy information – and the way businesses have responded to this new dynamic – is dramatically and fundamentally different as a result of the rapid convergence of technology, media and communications.

What this really means is that the legacy telecom sector has been updated to include the likes of Alphabet (GOOGL), Meta (META), and Netflix (NFLX). This changed the sector dramatically and gave its performance a much-needed boost.

XLC has just 23 stocks, with the top 10 having a heavy weight. META and GOOGL make up a whopping 48% of the fund.

XLC Top 10 Collectibles (Searching for Alpha)

The combination is simply a function of adverse selection and the “adjusted market capitalization” methodology used by the underlying index’s matching company, S&P Dow Jones Indices LLC. META and GOOGL have reached or near the maximum allowed by index rules:

If any firm has an FMC weight greater than 24%, the firm’s weight is capped at 23%, allowing for a 2% buffer. This buffer is intended to dilute any company that exceeds 25% as of the diversification requirement date at the end of the quarter.

This simply means that META and GOOGL cannot have more weight, even if they outperform.

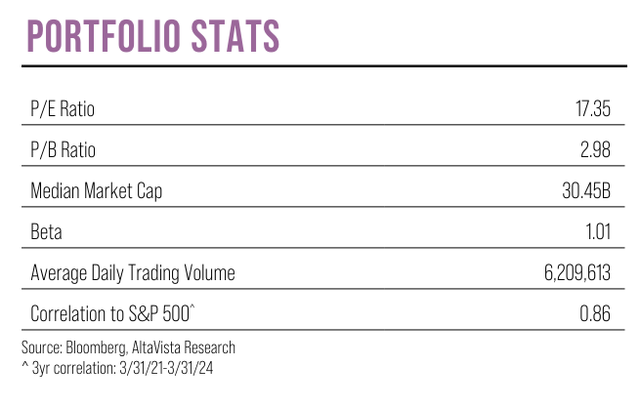

Here are some additional statistics about XLC –

XLC properties (Sector SPDRs)

The P/E ratio is attractive at 17.35, well below many other sectors. This is primarily due to the low valuations seen in legacy telecom stocks. For example, AT&T (T) has a forward PE ratio of 8. Verizon (VZ) has a forward PE ratio of 8.8.

Standard & Poor’s estimates that sector gains should be a healthy 17% this year, but again, this is primarily due to stocks like META, GOOGL and NFLX and not the likes of T and VZ. It seems as if XLC is two sectors stuck together, but it is currently working.

Behind XLC’s superior performance

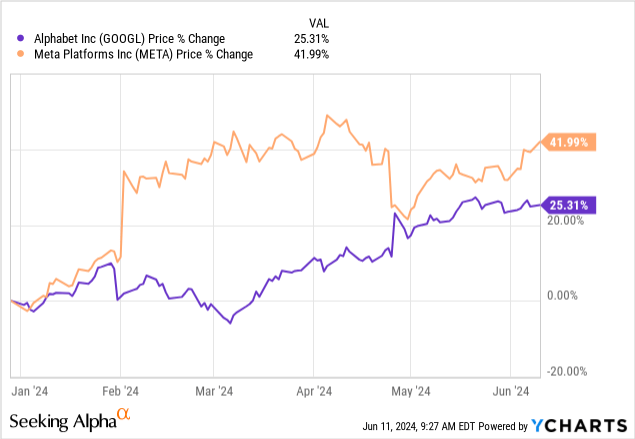

XLC has benefited greatly from the heavyweights in META and GOOGL which have performed very well this year.

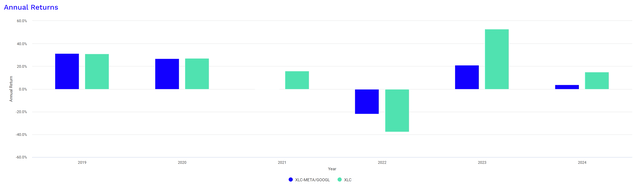

If we exclude META and GOOGL and then normalize all remaining XLC holdings so they total up to 100%, this is how XLC would perform.

Performance comparison (wallet visualizer)

YTD gains would be around 4% without META and GOOGL. Obviously, XLC relies heavily on these two stocks, and it makes me wonder if you might be better off focusing on just them rather than buying a fund that contains many other differentiated stocks. The opposite is also true – if I really liked the telecom sector in its old form; A fund that focuses on stocks like T and VZ and would likely pay a healthy dividend instead of the 0.78% that XLC currently offers, I wouldn’t buy XLC.

At the moment the performance is attractive, but will it continue? To come up with an answer, you’ll need to analyze META, GOOGL and then legacy stocks. They are actually performing very well as yields have fallen and the Fed’s “go higher for longer” expectations have faded. For example, VZ is +35% from the October 23 low. However, I think this overcomplicates things and I look for clarity and simplicity in sector funds. I want to know exactly what drives performance, and in the case of the XLC, there seem to be two or three drivers with very little in common.

Conclusions

XLC is the best-performing sector ETF YTD, but that’s almost entirely due to the performance of META and GOOGL and their huge weightings. Most of the fund’s remaining holdings from the telecom sector appear to be uncorrelated, and XLC is composed like two different sectors rather than one. Although the sector’s performance is attractive, its composition is confusing and the fundamental drivers of the sector as a whole cannot be simply defined. For this reason, I rate XLC as a Hold rather than a Buy.