DNY59

I last covered XYLD in January of last year, when I argued that high levels of implied volatility would allow ETFs to generate strong option income, which would likely outweigh the impact of any capital gains in the S&P. 500. Since then, XYLD has returned 16%, with these returns coming almost entirely from option premium income. However, a lot has changed since then. Specifically, implied one-month call option volatility fell by about half, while S&P 500 valuations rose to extreme levels while market breadth collapsed. The income that XYLD is likely to generate is now no longer worth the risk of a significant market decline, and any rise in volatility could actually cause the ETF to underperform the S&P 500 even under a declining market scenario. Therefore, I am shifting my recommendation from commental to strong He sells.

XYLD Price and Total Returns Revised to 2013 (Bloomberg)

XYLD ETF

GlobalNYSEARCA:XYLD) tracks the performance of the CBOE S&P 500 Index BuyWrite, which holds the S&P 500 and writes calls against it in order to capture the option premium. XYLD is similar to the JPMorgan Equity Premium Income ETF (JEPI) with the main difference being that the former sells at-the-money options rather than little-at-the-money options, allowing for greater option income at the expense of lower capital gain potential. . XYLD launched in 2013, and since then, it has significantly underperformed the S&P 500 where capital gains have been particularly strong. The current dividend yield on the ETF is 9.5%, which takes into account an annual expense charge of 0.6%.

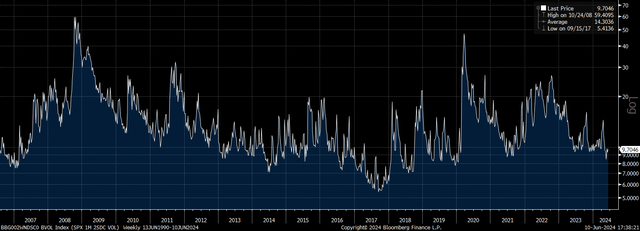

Implied volatility points collapse into weak option income

Covered call strategies like those used by XYLD make sense as an alternative to simply buying the underlying market when implied volatility levels are high. In January 2023, ETFs returned over 13% on a sequential basis due to high levels of implied volatility. However, since then, implied call option volatility has collapsed, with the one-month call option delta falling from 20 to less than 10.

25-Month Delta Call Volatility (Bloomberg)

This is almost a full standard deviation below the long-run average of 12.3%. Likewise, low levels of implied volatility in the past have generated annual income returns of only 5% to 6%.

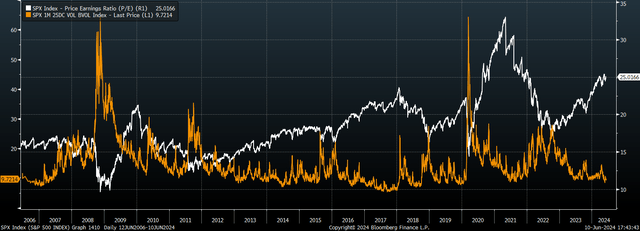

Extreme valuations and low market breadth increase the risk of sharp declines

Not only is low implied volatility likely to undermine income returns, it also increases the risk of a significant market decline if sentiment turns, which could easily wipe out the option’s income impact. Adding to this risk is the fact that S&P 500 valuations have once again risen to extreme levels, with the P/E ratio rising from about 18 times last January to 25 times today.

S&P500 to PE Ratio vs. Call Option Volatility (Bloomberg)

There have been periods where high valuations and low implied volatilities have remained in place for some time. This happened in 2017 and allowed XYLD to achieve amazing returns of 17% for the year. However, not only are valuations more expensive than they were then, but the market is now more favorable to the performance of a small number of stocks. For example, in 2017, the share of S&P 500 stocks that reached new 52-week highs was much higher than the share that reached new 52-week lows. In contrast, the recent all-time highs were driven by a small number of mega-cap stocks, most notably Nvidia and other AI beneficiaries, which increases the risk of a sharp market decline if these stocks start to falter.

XYLD may not even outperform the S&P 500 during a bear market

Being bearish on the US stock market, I still expect XYLD to outperform the S&P 500 over the coming months and years, as is typical during bear markets, where capital losses are at least supported by options income. However, even if the market declines, it is by no means guaranteed that XYLD will outperform. If we see sharp declines in the S&P 500 and strong rises in a bear market, XYLD will suffer capital losses on the way down but will not benefit from the upside from the relief rallies. While this is an unlikely scenario, the current low levels of option income make XYLD particularly unattractive from a risk-reward perspective.

summary

I have switched my view on XYLD from Hold to Strong Sell since my last hold in January of last year, due to a combination of collapsing implied volatility and increased risk of a significant decline in the S&P 500. XYLD now offers insufficient income to offset the potential capital loss Which could happen if sentiment turns bearish and downside volatility rises.