DNY59/E+ via Getty Images

Investment thesis

the next (New York Stock Exchange: Yes) Bull’s case is summed up as a very strong balance sheet. Yesterday, management announced that it is seeking to distribute the bulk of its balance sheet funds to make a large, impactful acquisition. So far, the stock is down more than 10% on this news.

In other words, Yext will see some inorganic growth once this acquisition is complete, but beyond that, is there enough here for investors to go bullish on Yext?

I do not think so. Therefore, I rate this stock a sell.

Quick recap

I said last October:

Coming to this point, this stock is currently priced at 21 times this year’s EPS, a multiple that may be too high for a company that may end up with no revenue growth next year. This means that without top line growth, there is Only so far can Yext cut costs before earnings per share also stop growing.

The author worked on YEXT

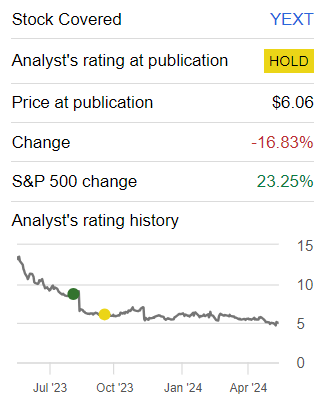

Since I wrote this analysis, the stock has retreated, which, including the pre-market decline, is now down 25% versus the S&P 500 which has risen more than 20% in the same period.

In other words, in hindsight, I was right to downgrade this stock. Now, with another 6 months of results, I rate this stock a Sell. this is the reason.

Yext’s near-term prospects

Yext helps businesses manage their online presence and customer interactions. It provides tools for businesses to ensure their information is accurate and easy to find across various digital platforms, such as search engines and social media. Yext also helps businesses engage with customers through features like review management and local marketing.

In short, Yext specializes in maintaining consistent business information and improving local search visibility.

Furthermore, Yext’s acquisition of Hearsay Systems enables it to significantly enhance its digital presence and customer engagement capabilities, particularly in the financial services sector. By combining Hearsay’s customer engagement solutions with Yext’s digital presence platform, the company aims to offer a comprehensive set of tools for managing the customer journey. This strategic move is expected to provide Yext’s clients, which include some of the world’s largest financial institutions, with the capabilities to communicate and communicate with customers effectively.

However, one of the challenges that Yext faces in the current economic environment is characterized by strict budget constraints among clients. The financial pressure on Yext customers, combined with increased scrutiny of IT and marketing expenses, has led to slow order conversion and challenges in contract renewals at previous levels.

Given this context, let’s now delve into its financials.

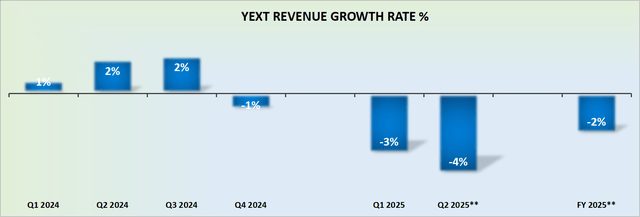

Fiscal revenue growth rates for 2025 have been revised downward

YEXT revenue growth rates

Previously, Yext was guiding for about $400 million in revenue for fiscal 2025. Now, that guidance has been revised downward by a small amount, to ultimately $396 million.

Needless to say, this downward adjustment is not a large amount. But when Yext barely met the low end of its fiscal first-quarter 2025 revenue guidance, plus investors are now facing a downward revision to its full-year guidance, this is quite… This means that its prospects do not appear to be improving any time soon.

Thus, investors are looking at a fiscal year without growth, in the best-case scenario. Or perhaps, if the environment deteriorates further, Yext will see its revenue shrink this year.

In short, this is not a promising setup for new capital to get involved in this stock. Especially since its valuation is not exactly in the basement of the deal, which we will look at next.

YEXT Stock Valuation – 7x EBITDA

Yext has approximately $100 million of cash and cash equivalents on its balance sheet and no debt. This cash amount is after its acquisition of Hearsay is taken into account. Note that I assumed that there would be some additional payment associated with this acquisition to meet the performance targets.

This means that including the 10% pre-market decline, approximately 15% of Yext’s market capitalization consists of cash. It goes without saying that this is a bullish factor that investors will be willing to give some weight to. However, this cash only has some value if management is able to intelligently deploy this capital into something accretive to the company.

Or maybe another way to look at it is that Yext has already made its moves. A very bold move to acquire Hearsay. A company is barely breaking even on its cash flow line. Although management has yet to provide any formal guidance on what kind of growth investors can expect from the combined business, I think we can assume that Yext has bought itself another year of inorganic growth rates. But is that really compelling enough to pay nearly 7x EBITDA for Yext? A business without organic growth rates? I don’t think this makes sense. Therefore, I rate this stock as a Sell.

Bottom line

In conclusion, Yext’s recent announcement regarding its intention to use the majority of its cash balance in a large acquisition surprised me in a negative way.

While the move may lead to some short-term inorganic growth for the company, questions remain regarding the sustainability of its upside prospects.

Moreover, downward revisions in revenue growth forecasts for fiscal 2025 raise concerns about the company’s trajectory. Although Yext has a large cash reserve of about $100 million and remains debt-free, its recent acquisition strategy and uncertain growth outlook lead me to question its valuation.

With the stock trading at nearly 7x EBITDA and facing the prospect of no organic revenue growth in the near term, it makes sense to call it a day at Yext.