Slavko Sereda/iStock via Getty Images

Investment summary

Since my last post on YPF Sociedad Anónima (New York Stock Exchange: YBF), and the company’s shares rose more than 95% to the top. The catalysts were: 1) The positive results of the 2023 Argentine presidential elections, where Many of the stocks in this basket received strong demand due to a more positive outlook for the business in the coming years, and 2) improving fundamentals. The new government He put An ambitious target of reducing the budget deficit by five percentage points of GDP saw early promise, as shown in Figure 1. This was underscored by significant spending cuts – in particular, reductions in real primary expenditures By 35% on an annual basis. year.

Aside from this, other efforts that could serve as potential tailwinds for businesses in the region like YPF include the following:

1. Spending adjustments

- Non-discretionary spending

according to Economic ObservatoryThe adjustments were particularly strong in non-discretionary spending, which was constrained to grow below the inflation rate. Pension expenditures also decreased by 36% compared to last year, which represents a large part of the fiscal consolidation, representing 43% of the total fiscal adjustment.

Fiscal tightening extends to discretionary spending as well. Capital expenditures and transfers to the regions were also significantly reduced, contributing 32% to the change. Economic subsidies – especially those directed to energy companies – have also been reduced. To me, this is a positive for the company, because it will provide a more level playing field for economic forces (not government forces) to do their work.

2. Revenue adjustments

On the revenue front, total real revenues saw a 4% decline, primarily due to lower social security contributions. However, tax revenues increased, supported by the tax imposed on certain exchange rate operations, which effectively serves as an import duty. This currently makes up 9% of total revenue, so it’s not a small amount.

Figure 1. Argentine public financial accounts

Economic Observatory

In a recent YPF post, my opinion was that the company was trading at a statistical discount of 0.5x its book value, saving an additional 15 percentage points of ROE to the investor if they paid that price. I also noticed very cheap earnings multiples at 2.8x P/E. The decisive catalyst I saw was financial change in Argentina, which has already happened. In the wake of recent developments, I’ve updated my outlook on the company and will share my findings here today. Net net, review to buy.

Q1 2024 Earnings Insights

It’s been a reasonably flat period of business for the company in the first quarter of 2024. Revenue was $4.3 billion, in line with $4.2 billion last year on earnings of $1.66 per share, up from about $0.90 a year earlier. It pulled this down to adjusted EBITDA of $1.2 billion, up 15% year over year. Growth was driven by favorable market prices and product productivity – with hydrocarbon production up 300 basis points year-on-year, and shale production up 21% year-on-year. The latter’s increased production is a major catalyst going forward as well in my view.

The bulk of revenue was generated from downstream sources, at $3.76 billion, while upstream revenue was $1.98 billion (mostly through inter-segment sales), and gas and power sales rose to $482 million. In my opinion, one of the most notable takeaways from this divisional performance is the fact that the company achieved bottom-line revenue and operating profit growth of 3%. It decreases In the assets used in this part of the work. Since this is the company’s main source of income, it was nice to see this kind of efficiency.

Figure 2.

Source: YPF 6-K, author

Potential drivers of future price changes

One of the most important findings over the past three months is that oil production in Argentina’s Neuquén region reached a record high in April. The reason for this was the inactivity of the restart of the Vaca Meurta formation, of which YPF owns the main developments. As a reminder, the formation is considered the second largest gas reserve in the world and the fourth largest shale oil reserve.

The report showed that crude oil production increased by 19% over the 12 months to April last year and increased by about 19% in the 12 months to April 2024 as well. This is in line with the updated economic policies I outlined earlier, which could be a potential tailwind in this case. Export is likely to become a key tool that the government will use to turn around the fiscal deficit and reduce inflation pressure.

Here, YBF has a potential competitive advantage, given its structure with Argentina. It has begun construction of a new 130-kilometre oil pipeline from the Vaca Muerta site, which could increase production by 135 million barrels of oil per year. The initial investment amounts to $190 million and will allow the transportation of 390,000 barrels per day, i.e. an increase of 70% in the oil transportation capacity in this region.

If all goes according to plan, the company said there is potential to build additional businesses at the site, including an export terminal worth $2 billion in capex.

Investment activity can be a major catalyst in my opinion. Capital investment can raise profits significantly.

For example, one of the most important results I observed from Q1 was the increase in total capital productivity to previous ranges in 2022.

As shown below, the company returned $0.17 in gross profit for every $1 of assets used on the balance sheet in the first quarter (TTM values). This is in line with the 2022 ranges when oil prices commanded a premium. I’m more positive on the company given this reversal in the trend that has been in place over the course of 2023, something I clearly commented on in the last post.

Figure 3.

Company Files, Author

evaluation

In my opinion, the valuation discussion is the most attractive element of the YPF equation. Even after extensive stock repricing, the company still sells for 6x forward earnings, 8.7x EBIT, and a 0.8x discount to book value.

In my opinion, this represents a statistical discount given the company’s profitability. I’m interested in YPF stock and would evaluate it on an all equity basis. In this context, I look to the forward ROE to indicate whether or not this is actually a statistical discount.

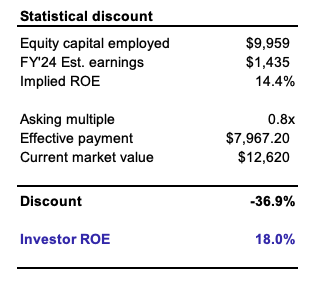

The company left Q1 2024 with net tangible assets (equity capital) of $9.6 billion, having lost capital throughout the period. Consensus estimates call for the company to deliver 46% growth in earnings to $3.65 per share, calling for $1.44 billion in YPF’s bottom line this year. On equity of $9.6 billion, the implied return on forward equity is 14.4% (1,435/9,959 = 14.4%).

This is where the discount appears. The current book value is $9.6 billion, and we are being asked to pay 0.8 times that amount; We’re effectively paying $7.9 billion for a company with a market capitalization of $12.6 billion, as I write (Figure 4). That’s an effective discount of 37%. Furthermore, if this multiple is pushed up, the ROE rises to 18% from 14% due to the higher dividend rate on lower capital.

Figure 4.

author

Furthermore, creating or starting a group of operations the size of YPF or purchasing business assets of similar quality would be impossible, let alone in the realms of reality. It is rare to purchase these assets at a discount from their liquidation value. Here we are buying a high-quality company that produces a trailing return on equity of 14% (it was 15% in the last post) at a discount from the net tangible assets required to operate the company. It would be almost impossible to find this quality for a sale at a discount on the private market. This is one of the main advantages of the stock market in the first place. It enables investors to buy pro-rata positions in great companies, while paying a fraction of the pro-rata cost of the private market.

In this regard, I believe that YPF represents a statistical discount and that there is tremendous value on offer in paying a book multiple of 0.8x today.

With the combination of 1) favorable financial winds, 2) improving productivity, 3) major capital investments, and 4) compressed valuations, my view is that the company should trade closer to the sector multiple, at about 1.3 times book value. I cannot see, other than previous Argentine economic pressures, why this would not happen. This gets me to $15.9 billion in market cap, or $32 per share, with a potential 53% return.

The main risks of the thesis

Investors should recognize these risks before moving forward:

-

There is still no certainty about the long-term future of the Argentine economy; Although there have been promising changes so far, there is still a way to go. This still represents a risk to the overall thesis and must be taken into account.

-

YPF is a company that sets oil prices and does not set the prices it charges for its products – this is done through the market. Commodities like operations have a disadvantage in this regard, and weak oil and gas prices could be a headwind for the company.

-

We cannot ignore broader macroeconomic risks either, as these risks may affect stock markets in general. A breakdown in access to inflation/prices could be negative for stocks, and the geopolitical tensions currently impacting equity markets could spill over into YPF names.

Investors should consider these risks fully before making any investment decisions.

Briefly

YPF offers a statistical discount with multiple tailwinds fueling the company’s afterburners. Argentina’s changing financial system, positive economic development there, and positive outlook for oil exports from the country are two key factors that could impact the company positively moving forward.

But what’s even more attractive in this discussion is the fact that the company is selling at a discount to the net assets used in the business. I find it hard to believe that there would be a similar type of company available to trade for this type of valuation, where we could buy trading assets for less than liquidation value. The implied return on equity rises to 18% for the investor if he pays this multiple. We can thank the stock market for this.

This, combined with the valuation gaps provided by the discount, means that YPF may currently be undervalued by 53% and will be looking at a price target of ~$32 in the following months of trading. In this regard I am revising my rating on YPF to Buy.